Hello Guest User, You are visiting this website from a computer with an IP address of 172.71.254.74 with the name of '?' since Fri May 3, 2024 at 8:04:26 AM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - August 1, 2023 to August 31, 2023

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch August 25, 2023: Go Deep Young Man or I Go Home!

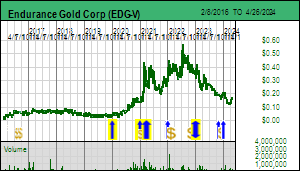

Jim (0:00:00): Why does Endurance Gold's chart look like a lead finger is weighing on it?

Endurance Gold Corp started the 2023 field season at its 100% optioned Reliance gold project in southwestern British Columbia in early May and as of August 3 had reported results for 10 core holes with results pending for 4 holes and hole 23-75 in progress. Earlier in the year the stock came under pressure when a major shareholder who wanted Endurance to mount a very aggressive 2023 drill program decided to bail, perhaps fearing he might not live long enough for Reliance to reach a tipping point confirming it has a major gold discovery. The stock had recovered back above $0.30 when drilling started, but then it really does look like a lead finger weighed in on social media about the not so good looking stock chart. By then the optimism we saw about the resource sector in Q1 had vanished, and nearly every resource junior's chart looked bad, so at least partly it is the market funk linked to gold's failure to turn $2,000 into a base rather than its ceiling that weighs on Endurance's stock price. But that doesn't explain why the shareholder bailed earlier this year when gold was above $2,000 and threatening to turn that into a base for higher prices down the road.

The Reliance gold mineralization is an epizonal orogenic system such as the nearby Bralorne gold system which produced over 4 million high grade ounces from a swarm of veins. Orogenic gold systems, also called "mesothermal", are different from epithermal systems whose vertical zonation is constrained by the interaction of metal bearing hydrothermal fluids with near surface groundwater circulation. This usually limites the vertical extent of mineralization to 200-600 metres. The latest Endurance presentation has a regional map showing the relationship of the Bralorne area orogenic systems associated with the Bendor Batholith and the Spences Bridge epithermal district to the east where Westhaven Gold Corp recently reported a PEA for its Shovelnose project. There is no genetic relationship between the two districts, but their juxtaposition does help illustrate what is special about Endurance Gold's Reliance project.

The Shovelnose PEA indicated a CAD $222 million after tax NPV at 6% and 32.3% IRR using $1,800 gold and $22 silver base case prices for an in situ 768,000 oz gold and 3,998,000 oz silver resource to which the market has reacted unkindly. The Shovelnose PEA envisioned a 1,000 tpd open pit mine with CAD $122 million CapEx which would yield 534,000 oz gold and 2,715,000 oz silver over 9.5 years. The PEA clears development hurdles, but the market prefers bigger scale. To be fair, the PEA is only based on the South Zone, so there is room for a bigger scale scenario if additional zones along strike or parallel end up being included. But this illustrates the difference between epithermal and orogenic systems. Westhaven cannot go much deeper and it has done sufficient nearby exploration to limit the immediate upside potential from parallel and on strike zones; although additional mineralized zones are not included in the PEA, the market has perhaps prematurely concluded that Shovelnose is as good as it is going to get.

Endurance's results so far suggest potential for a similar scale open-pittable resource between the Imperial and Eagle Zones and some shareholders have suggested maybe Endurance should focus on delivering a maiden resource estimate so that the number crunchers can assign outcome visualization based valuations to the project. However, that is not what our grumpy shareholder who bailed earlier this year wanted. He was focused on the geological fact that Reliance is an orogenic system, and given evidence the mineralization is very high in such a system, should have substantial vertical extent within which gold mineralization could blossom in grade, width and continuity so that it can become a high grade underground mining play such as Bralorne became a century ago. This shareholder declared to CEO Robert Boyd, "Go Deep Young Man or I go Home!" Robert Boyd's nature is one of cautious exploration that builds on incremental new information, and without an over-flowing treasury in place, was not going to drill deep speculative 1,000 m holes, at least not quite yet. So our grumpy shareholder called it quits and went home.

Robert Boyd believes he has a big one on the line at Reliance, and does not want to risk losing this fish because he runs out of money in a bad market. This week Barrick's former exploration VP, Alex Davidson, came on board as an advisor. While conceptual geological plays like NuLegacy's Red Hill Carlin-type project in Nevada do intrigue him, what attracted him to Reliance was the "strength" of the mineralizing system and its geological context. Orogenic gold systems form well below the surface and deposit high grade mineralization over a great vertical extent that can run into thousands of metres such as is the case in the world's greenstone belts. These structurally controlled deposits end up exposed at surface thanks to extensive erosion. The difference between Bralorne and Reliance is that at Reliance the gold system associated with the Royal Treasure Shear is near the top of the system, based on the presence of other elements such as antimony which are not present at the bottom of an orogenic system.

The source of the orogenic fluids is linked to the Bendor Batholith on whose southwestern flank sit Bralorne's veins and whose chemistry implies the mineralization is more than 1,000 m deeper than the mineralization at Reliance which has associated antimony and arsenic. The tantalizing story about Reliance is that the mineralizing system at surface is very powerful with lots of high grade gold zones and chemistry indicating the top of an orogenic system. And so the question arises, how much gold was left behind at depth in rich zones? The northwestern end of the Royal Treasure Shear trend disappears under the Carpenter Lake hydro reservoir and it seems to fizzle out at the southeastern end for a total 1.5 km strike length (though this may be a function of physical access up the mountain and the fact that the gold zones appear to be like shoots interspersed with lower grade mineralization).

There remain untested near surface gaps such as between the Imperial and Eagle zones, but after 3 years of RC and core drilling Endurance could hunker down and crank out an open-pittable resource similar to what Westhaven has done, followed by a PEA. The sizzle, however, lies with going deeper, substantially deeper to the depth where Bralorne style veins might start to show up. And the Bralorne veins were much thicker, richer and continuous than what we have so far seen at Reliance.

The reason delineation of the Reliance gold system has taken so painfully long is partly due to Robert Boyd's cautious use of staged multi-data set collection to develop a geological understanding of what makes the mineralization within the Royal-Treasure Shear Corridor tick. Keep in mind that the Imperial zone was discovered in the 1980s by the late Charlie Boitard, a maverick who used dowsing methods to spot drill hole locations. Although Imperial yielded some spectacular intervals, subsequent drilling did not reveal the geometry of mineralization. When Endurance took on Reliance in late 2019 it explored the Royal-Treasure Shear by building a road along it up the mountain and surface sampling the road cuts. This became the basis for a shallow RC drill program in 2021 which confirmed that the gold mineralization was a shallow dipping gold zone within the foot wall of the Royal-Treasure Shear corridor separated by some sort of thrust fault from the southwest that had placed younger sediments as the hanging wall above the mineralized corridor. Due to the limitations of road access most of the core holes drilled in 2022 were spotted on the foot wall side, which, because these holes were drilled westward, chased a mineralized zone that was dipping southwest. This becomes a problem when you try to delineate the zone down dip.

The latest corporate presentation contains a longitudinal section which shows where mineralization has been encountered relative to an elevation scale on the right side of the section. The dots present ranges for the equation gold grade times metres. Hole 23-70, drilled from the footwall side and the last one reported this season, which yielded 3.7 m at 7.91 g/t gold, is represented as an orange dot for the 25-50 range at an elevation of 1,000 m, which is about 250 m beneath the surface. The section includes 3 deeper black dots representing grade x metres of less than 10. That makes it look like the mineralization is fading at depth, but Boyd explained that those holes were drilled from the foot wall side and never reached the mineralized structure hole 23-70 encountered. The longitudinal section is a two-dimensional plane onto which every mineralized pierce point is projected, so can be misleading. When the company tags the Eagle zone as open at depth that is actually the case. With the next update we will likely get a drill plan and sections for the Eagle Zone that allows us to better track what is unfolding.

By the end of 2022 it was clear that to test the Eagle and Imperial zones properly at depth the holes had to be spotted on the hanging wall side of the Royal-Treasure Shear corridor and drilled toward the northeast. But that first required permitting and building roads up the mountain, which Endurance has accomplished this year.

So far Endurance has drilled 10 core holes, 4 of them testing the Imperial Zone at depth though 2 had to be abandoned. The second pair, 23-65 and 23-66, revealed that the Imperial zone is alive and well at depth, and the 2 holes into the Diplomat Zone along strike to the northwest also show the mineralization persists toward Carpenter Lake. Road building has focused on the higher elevation Eagle Zone where holes 67-74 have been drilled from the hanging wall side, with results reported through hole 70. Drilling earlier in the season was done at the lower elevation Imperial and Diplomat zones while the roads traversing the hanging wall side of the Royal-Treasure Shear were built. Holes 71-73 were shipped for assays in late July, but hole 74 is still in the box awaiting sampling, and hole 75 is partly done, with no holes drilled since then. On August 3 Endurance Gold reported that it had to suspend exploration work because Goldbridge had been ordered to evacuate due to forest fire in the vicinity of Gun Lake.

The Reliance project is not threatened by fire which is limited to the north side of Carpenter Lake. But Endurance had rented a building near Gun Lake to house its exploration crew, and once the evacuation order came, there was no place to stay. The fire torched a number of houses, including the residence of the landlord, but only came within 500 m of the rental house. Fire also caused the evacuation of the Shalaith First Nations community from which Endurance sources a number of workers, though apparently that evacuation order has been lifted. Currently there is no road access to Goldbridge except for emergency and fire support vehicles, both from the Pemberton Meadows and Lillooet access routes.

The authorities have given no guidance when they will lift the evacuation order and restore general access. Robert Boyd is hopeful Endurance can resume drilling in September but is frustrated that the entire month of August has been lost. Drilling without a winterized camp can continue into early December and resume in April. He figures with the current budget he could get 15-25 more holes done with one rig, but would like to increase the drilling rate by adding a second rig. However, given his cautious nature, he only wants to add a second rig if he can raise additional funds, and that he does not want to do at the current price level unless it involves a premium priced charity flow-thru financing. Most of the remaining holes will test the down plunge extent of the Eagle Zone, while others will attempt to fill the 400 m gap between the Imperial and Eagle zones. This gap exists because there is limited outcrop due to topography which has allowed a thicker blanket of ash from the Mt Meager eruption to settle, so was not part of the initial surface sampling work.

The immediate goal is to extend the Eagle zone into the 900-1,000 m elevation depth (23-70 is at about 1,000 m - deeper means lower elevation). Boyd is reluctant to drill big deep stepouts because the team thinks the mineralization's plunge has a rake to the southwest which they want to confirm in order to spot productive holes. He much prefers to follow the zone with incremental stepouts before becoming more aggressive. That means it will be a while before Endurance reaches the depth where Bralorne style veins will be present. On the other hand, with each incrementally deeper hole, the potential exists for the mineralized zone to blossom, and once that happens, Endurance's drill rig will have something to chase which can revive anticipatory speculation. Except in the James Bay Lithium Great Canadian Area play positive outcome speculation is pretty much absent from the Canadian junior resource sector, which creates an early "bottom-fishing" season for stocks like Endurance Gold which have the capacity to generate game changing news.

The importance difference between last year and this year is that the new hanging wall access roads allow chasing the Royal-Treasure Shear structure down plunge from the hanging wall side and intersect the structure at an angle closer to a perpendicular. If the Royal-Treasure Shear zones start to blossom at depth, and the plunge-dip remains generally toward the southwest, Endurance will be able to add a second rig and become more aggressive with deeper stepouts. Should this tipping point happen the disgruntled shareholder might even come back into the market, and the breakout chart pattern could prompt lead finger's impact on the market to undergo an alchemical transformation in the social media world where it wags.

Given the shortened summer exploration season a key question is what Endurance will have gotten done on the Olympic and Sanchez properties it optioned 100% last year from Avino and a private party. These properties cover the western and northwestern flank of the Bendor Batholith. One concern I initially had was that the Reliance project was a relatively small property which carried the risk that the discovery could turn into a Shovelnose outcome if grades fizzle at depth or the zone disappears thanks to a blind low angle fault. That concern heightened in 2021 when it became apparent that the gold mineralization had a shallow southwest dip that raised the risk that it would stop when it ran into the thrust fault that separates the unmineralized sediments and the Royal-Treasure Shear mineralized corridor. But in 2022 drilling established that dyke like sub-vertical structures were present within the corridor on whose flanks gold mineralization was present, so that concern ameliorated somewhat.

In the case of Westhaven's Shovelnose project and the other properties it owns within the Spences Bridge epithermal belt, the junior can continue to explore on a district scale even if the South Zone and its nearby zones fall short of development critical mass. Endurance went after the Olympic and Sanchez properties on the premise that similar orogenic zones could be present on the other flanks of the Bendor Batholith. One would think that intensive prospecting a century ago in the wake of the Bralorne discovery would have found anything if it were to be found. But the Bendor Batholith is steep, has a lot of forest cover, and is burdened by thick ashfall from the Meager Creek eruption. A century ago prospectors did not deploy soil sampling and definitely not biogenic sampling methods which Endurance used to identify elevated arsenic levels that fir trees are absorbing from soils above mineralized bedrock (arsenic is a pathfinder at Reliance). Fortunately Endurance started early with its Olympic-Sanchez sampling program and completed it before the fire evacuation notice. Results expected later this year will tell us if the Olympic-Sanchez claims do indeed offer district scale potential for additional orogenic gold systems. There is reason to be optimistic; Robert Boyd grumbled about how the sampling medium is thick and difficult in this area, which gives hope that prospectors did not find anything because nothing was there, but because it was pretty much hidden "under cover".

Orogenic and Epithermal Districts in southwestern British Columbia

Google Earth Map showing Fire Locations

Longitudinal Section of Royal-Treasure Shear Corridor

Illustration of how net roadwrok will facilitate deep drilling

District Scale Potential created by Olympic-Sanchez Property Options

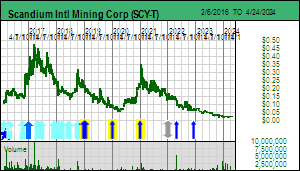

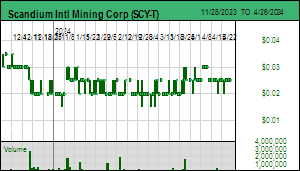

Jim (0:17:50): What you think of Scandium International's Nyngan results?

Scandium International Mining Corp reported on August 8, 2023 the results for a small drill program conducted on the Nyngan property. Earlier in the year the company announced that it planned two small drill programs, one to test additional targets on the Honeybugle property, and the other to assess the limis of the western zone at Nyngan. The Honeybugle results were announced June 20, 2023 in a press release with a detailed assay table and drill plan which allowed me to undertake a speculative back-of-the-napkin resource estimate for the Woodlong anomaly. Back in 2014 when SCY was in danger of losing the Nyngan property to creditors it drilled the Seaford magnetic anomaly on the Honeybugle property it had staked about 20 km from Nyngan. The results were better than reported for Nyngan and Honeybugle could have become a replacement project for Nyngan. But SCY managed to stave off foreclosure when the Evensen family extended a USD $2.5 million loan that was convertible into a direct 20% project equity stake. So SCY stuck with Nyngan which was more advanced and delivered a DFS in 2016 for which a mining lease was granted in 2017. The CEO George Putnam decided to embark on an offtake deal development strategy as a pre-condition for trying to develop Nyngan, a rejection of the notion "if you build the supply the demand will come".

No offtake deals emerged, but what did emerge was an extortion attempt Owen Carter had launched during the mining lease application period in 2016. He had sold the surface rights to the western half of the Nyngan claim to Jervois, then the owner of the project before SCY acquired it 100%, but retained the eastern half's surface rights which he then claimed qualified for protection as "agricultural land" which would have shielded it from eminent domain acquisition by SCY at fair market value. Unfortunately Carter's complaint letter disappeared into a wrong file and was never reviewed by the NSW permitting department which granted the mining lease. It resurfaced in late 2018 and NSW was forced to cancel the mining lease while it conducted a review of the agricultural claim's validity. The problem would have disappeared if SCY purchased the surface rights from Carter, but by then Carter, perhaps borrowing from the "sacred territory" handbook of Canada's First Nations, wanted a lot more money than the land was worth as marginal farmland. Eventually NSW ruled that it was not "agricultural land" and undertook steps to reinstate the mining lease for the eastern half (the mining lease for the western half, where all the infrastructure was to be located and which hosts the West Pit to be mined in the first decade of the mine's life at the initial planned operating scale, remained intact). News about the mining lease uncertainty no doubt was heard by SCY's various LOI "study" partners and likely helped derail whatever deal was close to happening.

SCY was vague about why it was necessary to conduct additional drilling at Nyngan, but I surmise it was based on a hope that the size of the West Pit could be expanded, pushing further into the future the date when it would become necessary to purchase the surface rights from Carter or his heirs. Since John Thompson who knows his mining stuff was on top of the resource data, and the resource targeted for mining was the higher grade near surface limonite horizon, I wondered what room there was to find additional tonnage. In contrast to the Honeybugle results, all that SCY reported was that "the drilling results have better defined the western boundary of the existing resource and reserve that are the foundation of the 2016 feasibility study and are therefore adding to our knowledge of how to optimize development of the project when it goes into production". There was no table of results nor a drill plan, but SCY did include two graphics, one a contour map of the limonite horizon with average grades for drill holes labeled, and the other a limonite thickness contour map. I'd never seen such graphics, so it was hard to tell to what extent the drilling changed anything. So I decided to look up the DFS technical report, couldn't find it saved on my PC, groaned at having to navigate the fabulously crappy new SEDAR Plus ClickaLot system created by the Canadian regulators in their tireless campaign to discourage investors from independently researching companies, but fortunately found it in Stockwatch's SEDAR archive. The grade contour map overlaps nicely with the existing West Pit design, so I guess what SCY learned was that West Pit limonite reserve was properly delineated. The company did not say how much meterage was drilled or how many holes. So it is fair to conclude that nothing new and positive was learned from the Nyngan drilling.

What is discouraging from the press release is that the company effectively declared that owning SCY will be dead money until their ongoing efforts to "engage with partners and customers to secure arrangements that will allow the Nyngan project to move into production" bear fruit. The Honeybugle results, which I described in KW Episode June 23, 2023, were very good, and coupled with the older Honeybugle results for the Seaford anomaly whose implications I described in Tracker June 7, 2021, should become the focus for a maiden resource estimate. Former CEO George Putnam was always reluctant to do that because supposedly it would increase the holding costs for Honeybugle, which sort of hints at the near eternal timeline he had in mind in terms of when the world would embrace aluminum-scandium alloy.

So what did I think of the results? The press release is a downer for SCY shareholders because it signals that nothing will change for a long time. A year ago the hope was that Rio Tinto would end up buying SCY or becoming the funding partner for Nyngan's development if Rio Tinto's efforts to develop the scandium offtake market bore fruit. The reason Rio Tinto is the best hope for this happening is because scandium offtake is stuck in a chicken-egg trap. No end-user wants to commit to an offtake agreement that has a risk that in the three years it takes to develop a scandium mine the result will not match cost and recovery expectations. And then all the tooling up and pre-marketing would be a writeoff. And no financier wants to provide CapEx to build a mine for whose output there is no guaranteed market.

Rio Tinto has the potential to crack this problem thanks to a solution it developed for the threatened evaporation of the market for the titanium slag by-product from its Sorel-Tracy facility in Quebec that smelts iron-titanium ore from its Lac Tio Mine. Pigment makers, especially those located outside China, are switching to a process that requires a higher purity feedstock, rutile equivalent that is about 95% TiO2. In developing a way to upgrade its 80% TiO2 slag to a purity demanded by pigment makers, Rio Tinto noted that the 50 ppm Sc naturally present in the Lac Tio ore was reporting to the titanium slag when the iron ore was first smelted to recover the iron. Rio Tinto figured out a way to recover the scandium as part of the titanium slag upgrading process. Although Rio Tinto has not published any details, it looks like Sorel-Tracy could produce up to 50 tonnes of scandium oxide annually based on the smelting scale at Sorel-Tracy.

Current global scandium supply estimates, which are very sketchy, are in the 15-25 tpa range and supply comes from a hodge-podge of by-product sources that are not scalable. The lack of supply scalability to match rising demand is part of the chicken-egg problem that deters aluminum-scandium alloy adoption. But if Rio Tinto could gradually double or triple global supply with its Sorel-Tracy by-product, it could push scandium to a tipping point as more end-users become comfortable deploying it in what are initially elite product lines but could be deployed on a broader scale if scandium has a scalable supply with a stable price. When Rio Tinto senses it is approaching that tipping point the best way to increase supply would be to develop the shovel-ready Nyngan project.

Hopes that Rio Tinto might be getting close to such a tipping point were dashed on April 28, 2023 when Platina announced that it had sold its Owendale deposit in New South Wales to Rio Tinto for USD $14 million. Owendale is part of the complex that hosts the similarly rich and large Syerston scandium project that sits on the flank of Sunrise Energy Metal's low grade nickel-cobalt resource which Robert Friedland is pitching as a clean alternative to the dirty nickel Indonesia is supplying to China and anybody else who doesn't care about the environmental footprint (NYT: Chinas Nickel Plants in Indonesia Created Needed Jobs, and Pollution). Owendale, although it completed a DFS, is nowhere near shovel-ready. Sunrise has a lock on water rights in the region, so Owendale's scandium ore has to be trucked offsite to location where water is available and the tailings dumped somewhere. Owendale also sits on farmland that is much more fertile than in the Nyngan area and Platina does not own the surface rights. A mining lease has not been granted and no doubt the "agricultural land" claim will be invoked once the permitting cycle is initiated. Platina has repackaged itself as a gold exploration junior so it was happy to sell a dead asset for USD $14 million. In KW Episode May 5, 2023 I floated some complex scenarios about how this Owendale purchase might not be a death signal for SCY's buyout hopes, but the simplest scenario is that Rio Tinto bought Owendale cheaply because it has realized it will be a very, very long time before its Sorel-Tracy supply builds offtake demand to a tipping point where it will need to secure scalable supply elsewhere. The acceptance of this glum timeline is implicit in SCY management's failure to signal that it will do anything with the Honeybugle results.

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch August 22, 2023: Will NPK survive the 2023 sales slump?

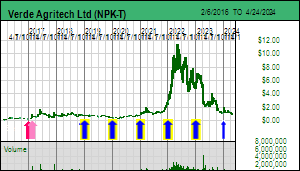

Jim (0:00:00): How did Verde Agritech's alternative potash sales do during the first half of 2023?

Verde Agritech Inc announced its Q2 results on August 14, 2023 and the market justifiably had a negative reaction. Revenues of $10.3 million in Q2 compared poorly to $24.9 million last year ($21.43 million H1 2023 compared to $36.165 million H1 2022), which was not surprising since potash prices declined 40% in H1 of 2023 after dropping 50% during H2 of 2022 from the 2022 peak. More disappointing is that physical volume in Q2 of 107,000 tonnes was just over half of the 202,000 tonnes sold in the same quarter last year. In total NPK sold 215,000 tonnes in H1 of 2023 compared to 314,000 tonnes in H1 of 2022. This is very disappointing because during H1 of last year NPK's capacity was only 600,000 tpa; today it is 3,000,000 tpa and NPK is not even achieving last year's first half capacity limit.

The company managed to squeak out a $133,000 net profit and EBITDA of $4.1 million (CAD) but that is not what caused the stock to fall below $3 on August 14 when the results were released. It is about concern that NPK's push to eventually sell 50 million tonnes of K Forte annually is failing. If Q2 sales volume during a key potash application period does not improve significantly in Q3, Brazil's second key fertilizer application quarter, Verde Agritech will fall well short of its 800,000-1,200,000 tonne 2023 target. It could end up achieving the same sales volume as in 2021. So an obvious question is, was the sales spurt in 2022 a temporary panic response to soaring KCl prices caused first by Lithuania's sanction related decision to stop letting Belarus ship its potash through the country, and then by Russia's Belarus backed invasion of Ukraine which raised fears potash supply from both countries would be disrupted? Or is there another reason why the demand slump this year may prove temporary, keeping alive NPK's dream of eventually supplying more than half of Brazil's potash demand?

According to the company the slump has been caused by a farm credit crisis that has prevented Verde Agritech from competing with the major potash importing fertilizer companies. Despite all the anxiety during 2022 about soaring food prices, an anticipatory global supply response reversed the crop price trend in H2 of 2022, and Brazilian farmers, hoping for a turnaround in Q2 of 2023 before financing their fertilizer input needs with crop forward sales, instead saw crop prices slump further in Q2 of 2023. A key driver for subdued food demand has been the high interest rate policy pursued by Global West central banks to bring inflation down to their 2% target. In 2022 Brazil increased its benchmark Selic rate to 13.75%, which halted the decline in the BRL against the USD. It also helped bring Brazilian inflation down to 3.99% which has prompted a modest decrease to 13.25% with a gradual decline to 8.25% projected for 2025. If the current inflation rate is stable, this implies a real interest rate of 9.26% which, of course, makes the real rate attractive relative to real rates elsewhere. For the farmers, however, all this is bad news because their crop prices have deflated. It is also bad news for NPK because the average rate for its lines of credit is 16.6%, which results in its lending rate to K Forte purchasing farmers to average 18.6%. The major fertilizer companies like Cargill, Nutrien and Mosaic, however, have access to credit in the 5%-6% range, which allows them to extend cheaper credit for the farmers' fertilizer purchases. They can also sweeten the deal by throwing in extra products the farmer might otherwise choose to do without. This credit crisis effectively froze out Verde Agritech as a supplier of alternative potash.

After the initial shock the stock has recovered but only because last month NPK disclosed that K Forte permanently converts about 120 kg of CO2 per tonne of K Forte into an inert mineral, or about 100 kg/t after accounting for CO2 emissions related to producing, grinding, shipping and applying K Forte to fields. The company is now focused on creating a carbon credit product it can sell to international groups such as Microsoft with voluntary goals seeking to offset their carbon footprints by purchasing carbon credits. Depending how much NPK gets for its carbon credits, it could use these proceeds to discount the price of K Forte relative to KCl and achieve market penetration in this manner. This potential to use carbon credit sales to escape the parity pricing strategy could attract a deep-pocketed buyer of the company.

Initially I was quite enthusiastic about this development, but only because I assumed that David Manning's study involved empirical measurements of glauconite grains combining with CO2 to form a carbonate mineral as they weathered, similar to what FPX Nickel Corp proposes to do with ultramafic rocks dominated by a magnesium mineral called brucite. While the European government regulated carbon credit market currently commands a price around $100/tonne CO2, according to an Aug 23, 2023 NYT article by Peter Coy, To Fight Climate Change, We Need a Better Carbon Market, the carbon credits peddled in the voluntary carbon credit market trade at $2/tonne or less because they have a, pardon the pun, a credibility problem. NPK's two press releases have referred to carbon credit prices ranging from $100 to $500, but has not indicated what price it hopes to get for K Forte linked carbon credits. When I stumbled upon a page within its web site on How it Works, I realized that Manning's study is about the theoretical concept where ground up rock undergoes chemical weathering which causes a reaction with atmospheric CO2 that results in bicarbonate ions dissolved in water. The bicarbonate ions do not permanently sequester the carbon until they flow into the ocean where they combine with calcium and magnesium ions to form mineral carbonates that settle onto the sea floor. NPK has not disclosed any details about Manning's study, but I now suspect it is just a computer simulation model rather than a physical measurement. My optimism has consequently shifted to skepticism until we learn how K Forte's carbon capture can be verified and what price the carbon credits could capture on a large scale approaching the 50 million tpa output goal.

That, however, does not affect the original reasons why I think the Brazilian agricultural sector could undergo large scale adoption of K Forte as an alternative fertilizer to imported potassium chloride (KCl). One key reason is that applying K Forte to soil does not punish it by killing beneficial micro-organisms that keep soil fertile as does the dissolved chloride ions that are left behind when plants take up the potassium. The other reason is that two nasty members of the Global East, Russia and Belarus, could soon undergo a major supply disruption again.

According to the USGS Belarus produced 8 million tonnes of K2O equivalent potash in 2021, which dropped 50% to 4 million tonnes in 2022. Russian production dropped from 9.1 million tonnes in 2021 to 6.8 million tonnes. Total world production in 2021 was 47 million tonnes of which Belarus and Russia represented 17% and 19.4% respectively or 36.4%. Global potash production in K2O eq terms) dropped to 40.9 million tonnes in 2022, which drops the Russia-Belarus share to 31.3%; most of the drop is attributable to the slump in Belarus and Russia output. Vancouver KCl prices soared over $1,200/t in early 2022 when Russia invaded Ukraine, though the price had already risen from its $200/t holding pattern to $800/t in 2021 as the world rebounded from the covid pandemic. During H2 of 2022 the price came down sharply as the supply disruption from Belarus and Russia ended (no sanctions were imposed on potash exports), a vigorous policy of interest rate hikes to combat not so transitory inflation got underway at the halfway mark, and farmers decided to cut back on potash usage in light of abnormally high prices. Potassium, which plays a role in plant resilience to disease and thus boosts overall yield in a negative sort of way, is the only one of the 3 key fertilizers (nitrogen, phosphorous and potassium) that a farmer can omit for a couple years before crop yields decline.

The recovery of potash supply from Belarus and Russia may, however, only be temporary. Russia's invasion of Ukraine has now settled into a war of attrition between Russia and Ukraine which Russia will win the instant the United States withdraws its support for Ukraine, a goal for some of the Republican 2024 presidential candidates, including Donald Trump, who admire much about Putin and his autocracy. Putin's invasion of Ukraine has been such a disaster on all fronts that Yevgeny Prigozhin, head of the Wagner mercenary group which had been called into Ukraine to help out, mounted a strange coup attempt in late June. Instead of using aircraft to wipe out the convoy on its way to Moscow, Putin let the march plod onwards until magically Lukashenko brokered a deal that caused Prigozhin to call off the coup attempt which supposedly was aimed at Putin's military commanders rather than Putin himself. Putin offered a deal for the Wagner mercenaries to join the regular Russian army, and those who declined were allowed to relocate to Belarus, supposedly to train Belarusian troops how to fight. Since then the world has witnessed a strange charade where Prigozhin seemed to be flitting about Russia while his mercenaries seem to have returned to the Sahel where they were possibly helping Niger's military overthrow its democratically elected leader, Mohamed Bazoum, on July 26.

On July 26 the US State Department issued a Level 4 Travel Advisory not just advising people not to travel to Belarus, but also stating that "US Citizens in Belarus should depart immediately". Since then there has been a build of Polish, Lithuanian and Latvian troops on their side of the Belarus border, supposedly to stop an influx of refugees, not Belarusians, but rather refugees from the Middle East that Lukashenko has imported with the goal of exporting them to NATO Europe as a destabilization tactic. This advisory was not reported on by the media until this week. It made me wonder if the Wagner group was going launch a suicide mission from Belarus into Ukraine as part of an escalation by Russia of the conflict. The Russian ruble was tanking against the USD and this time around even a major interest rate hike was not working to stop the decline. Since the Wagner group has now been disowned by Putin, any military action by Prigozhin's mercenaries would be fair game for US intervention. The resulting mess could turn Belarus into a hot conflict zone and take its potash supply offline.

So were my thoughts when I recorded the KW episode on August 22. But on August 23 while preparing the written comments and graphics we learned that a private airplane with 10 passengers on board had crashed about 30 minutes from Moscow on its way to St Petersburg where Prigozhin has his headquarters. Prigozhin's name and that of his Wagner lieutenant Dmitri Utkin were on the passenger list. All 10 bodies have reportedly been found though identities have not yet been revealed. The NYT reported: "Russias Investigative Committee, a top law enforcement body, announced the opening of a case on the plane crash, on suspicion of a violation of air transport safety rules." If Prigozhin is among the dead, this probably spells the end of the Wagner group. It also simplifies Putin's war on Ukraine and ramps up the likelihood that a major escalation will happen before the end of the year. Given how hopelessly deep a hole Putin has dug for himself, anything could happen, though that might also include a safety issue with one of his airplanes, which really would require all of us to rethink the future.

How Brazil's high real interest rates push NPK to the sidelines

Verde Agritech's 2023 volume sales guidance looks hopelessly high

Global Potash Supply in 2022

Potash Supply of Belarus & Russia relative to Global Supply

Potash price and USD:RUB exchange rate charts

Jim (0:12:20): Anything new with the James Bay Lithium Great Canadian Area Play?

The fire access restrictions for much of the James Bay region of Quebec have been lifted. The SOPFEU fire map shows red outlined burned areas as no longer opaque, meaning the fires are subsiding, and much of the James Bay area is rated low (blue) or moderate (green) fire danger. The exception is the area on the southeastern side of James Bay which is still rated high fire danger (yellow) and is the reason the Billy Diamond Highway is still closed, making it impossible to access the east-west Trans Taiga Highway that passes through the heart of the northern part of the James Bay region where Patriot Battery Metals recently reported a world class lithium resource. Rain is now drenching much of the region and it looks like the fire season is over.

Many juniors have announced that boots are being mobilized onto the ground. The bad news is that barely more than 2 months of the regular 5 month summer exploration season remains for juniors to prospect key areas of the James Bay region where a variety of exploration strategies have identified pegmatite targets to be assessed as being of the LCT type. I haven't seen the confirming document, but apparently Quebec has extended claims assessment deadlines by one year, which is bad news for serious juniors but good news for armchair speculators who have map staked in prior years without doing any actual exploration work but are now enjoying an influx of Australian juniors willing to do outlandish option deals.

There is no reason to complain, because these ASX-listed juniors come with an army of Australian investors who not only understand the big picture energy transition story and its need for a 600% expansion of global lithium supply by 2030 to keep on track the EV contribution to net zero emission goals for 2050, but they also understand that Canada has an extraordinary geological potential to rival Western Australia in terms of hardrock sourced lithium supply. In fact, some may even be wondering if Canada hosts a pegmatite deposit to rival Greenbushes, which is comparable in scale to Brazil's Araxa niobium deposit, but, in contrast, woefully insufficient to supply the world's future lithium needs. Serbia's Jadar lithium deposit isn't quite a Greenbushes, but Rio Tinto claims the world needs 60 Jadars to meet 2035 demand, though Rio Tinto does assume claystone, Lithium Triangle salars, and oilfield brines will prove to be non-events.

It will be at least 2-3 years before we know if these other sources will be a reliable supply source, so the EV sector is looking hard at Lithium Mania 2.0, namely the hunt for LCT type pegmatites whose size and grade can be quickly quantified, and whose conversion into battery grade lithium carbonate or hydroxide does not hinge on new process technologies that will take another 2-3 years to demonstrate commercial scale viability. It is possible that in 3 years process technologies aimed at these alternative sources of lithium will show that a nearly unlimited supply of lithium can be mobilized at a cost well below what is needed for pegmatite supply, which currently is about $5/lb lithium carbonate. That would be the preference of the car makers. But time is of the essence and they cannot afford to gamble on innovative process technology stories when demonstrated process technologies can be taken to the bank. It is the reason why Albemarle, which produces lithium ion battery precursor materials, stepped up and handed PMET $109 million for a 4.9% equity stake at an implied value approaching $2 billion for a project that has only just delivered a maiden resource estimate. The Canadian exploration scene has a 2-3 year window to show what it has, the Australians get it, and Canadians are slouching on the sideline like a bunch of sad sacks. No wonder some KRO members who are mainly based in North America and Europe are trying to figure out how to trade ASX listed stocks and why Brunswick Exploration Inc has resigned itself to seeking a dual listing on the ASX.

I initially planned to create a Lithium Index representing all serious Canadian, US and Australian listed lithium companies, but given how successful ASX-listed companies were as they embraced the Lithium Mania 1.0 cycle between 2015-2018, after which their success tanked the lithium carbonate price during the 2019-2020 period now called the "Lithium Winter", I'm not sure what an all lithium types index trend would tell us today, especially if I apply an equal weighting for all index members on the starting date. Once I saw PMET deliver a world class maiden resource estimate for its Corvette project in the James Bay region, I decided to create an index consisting of juniors with land in this part of Quebec.

The criteria for membership is that the company must have a land position in the James Bay region. The index is based on $1,000 worth of stock based on the closing price of August 1, 2023, and it has been backdated to December 30, 2022. Initially I wanted the company to have a stated intent to explore for lithium to qualify for membership, but as I surveyed the field I realized that a lot of horrible juniors had claims in the James Bay region covering ground with questionable LCT-type pegmatite potential, and yet there were a number of pig-headed anti-lithium gold or base metals focused companies sitting on very lithium prospective ground. So I shanghaied those juniors and included them in the KRO James Bay Lithium Index along with the flaky juniors, because the nature of Lithium Mania 2.0 is such that any patch of ground could turn out to host low hanging fruit in the form of a major lithium pegmatite deposit.

Currently there are 54 members which are presented in the snapshot table below. I am sure there are some ASX juniors that are missing, and perhaps even some Canadian juniors, so this index will be retroactively adjusted over the next month. Please email me at [email protected] with the name of any company you think belongs in this index.

I have created the index as a tool to measure market response to the Great Canadian James Bay Lithium Area Play that is emerging in the James Bay region of Quebec and as an analytical framework. Most weekly Kaiser Watch episodes will include updates on developments within the James Bay region. But the Index link above will be behind the KRO paywall, and, through a combination of posts within the KRO Slack forum and Trackers posted to KRO itself, KRO members will get real time commentary on James Bay Lithium Index developments. The overall junior resource sector is in bad shape, and there are too many forks in the road to the future for me to predict which region or metal will become the next hot trend. But I am confident the lithium story which is linked to the energy transition goal is only going to get bigger. Prime Minister Justin Trudeau through his foolish dance with Canada's First Nation wolves could scuttle Canada's role as a major supplier of critical minerals needed for the energy transition, but for now I am betting Canadians will say no way to second class citizenship subordinated to a race based aristocracy.

KRO James Bay Lithium Index - Market Activity for August 22, 2023

MI% = change in member's index value, RS% = difference in change between overall index and member index values, W% = value weight of member

The big development this week in the James Bay region was news on August 21, 2023 that Brunswick Exploration Inc has identified the source of the 1,700 m by 200 m spodumene bearing boulder field it reported in June following one day it had boots on the ground on the Mirage project before being forced to evacuate by Quebec's forest fire closure. The news was very positive because it indicated that the boulder field had been extended to 3 km, but, more importantly, that up ice a cluster of spodumene bearing outcrops resembling the boulders had been prospected along a 2.7 km trend that was still open to the northeast.

When I first read the June news release I assumed the boulder field was parallel with the ice direction which in this part of James Bay is generally from northeast to southwest. Brunswick had not published any maps of its Mirage land position or anything showing the location and orientation of the boulder field. But when Brunswick first announced the Mirage project, which included a 100% option of the Lac Elsace claims owned by Jack Stoch's Globex Enterprises Inc, I tracked down an old claim map on Globex's web site and had a rough idea of what the geology looked like. The claims in the area were tracking greenstone belt trends prospective for gold and base metals system which Andre Gaumond's Virginia companies had chased in prior decades when Remi Charbonneau noticed pegmatite boulders he had the skill to recognize as containing spodumene, the preferred lithium mineral. He had pitched the idea to various people, including Bob Wares, but decades ago (2005) lithium was a $200 million market supplied by Chilean salar brines, Australia's Greenbushes pegmatite monster, and Albemarle's puny Silver Peak brine mine in Nevada, so nobody cared.

In early 2022 Bob's encyclopedic memory resurfaced the spodumene boulder story and he tracked down the source (Remi Charbonneau now works for Brunswick). Much to his annoyance Jack Stoch's Globex, which benefited handsomely from Bob's conversion of the depleted Malartic underground vein play into a major bulk tonnage gold mine, owned claims covering the approximate location of the boulders. So he did a reasonable deal which Jack was happy to do because he knew James Bay was a monstrously disappointing precious and base metals also ran. But Globex did manage to keep a net 2% NSR. The area, however, was a dog's breakfast of fragmented claim ownership, and while Brunswick staked open ground covering what was the obvious geological trend that would also be prospective for LCT type pegmatites, there were holes owned by others.

Having obtained only a one day visual snapshot of the boulder area before being forced to evacuate, Brunswick became concerned about tying up additional ground. It mentioned that it already controlled 13 km of the up-ice direction of the boulder field, so people like myself concluded that it would only be a matter of time before the up-ice source would be found. Although no diagrams were provided by Brunswick, the news release led one to conclude the 1,700 m by 200 m boulder field was parallel to the ice direction. After 3 decades of diamond exploration everybody is quite familiar with the idea that an indicator mineral train identified through till sampling will lead back to a circular pipe-like kimberlite source. But while kimberlites are created by sub-vertical magmas starting from a depth of more than 150 km, below the diamond stability field, pegmatite bodies are lateral magmatic flows that exploit linear zones of weakness.

Since the Globex map showed the northeast trend of the prospective rocks, I assumed the source would be an elongated pegmatite parallel to the ice direction. That left plenty of size potential open, but also the negative scenario of a pinpoint source with limited tonnage potential - for example, a 200 m wide kimberlite pipe equivalent. When I explained this to Brunswick CEO Killian Charles he reacted quite adamantly that the boulder field was perpendicular to the ice direction, emphasizing that if this were not the case, the source could be an inconsequential pinpoint. To me that was a very significant revelation, because there was no way such a configuration could exist in glaciated terrain unless the pegmatite source was very local, with the boulders possibly frost-heaved. So in KW Episode June 23, 2023 I declared that, based on the spodumene crystal composition of the Mirage boulders and the distribution of the boulder field relative to the ice direction, Brunswick was sitting on a major lithium discovery.

Monday's news release revealed that my conclusion was based on nonsense. The diagram published by Brunswick showed that the boulder field, which had grown from 1,700 m to 3,000 m, was parallel to the ice direction. The good news was that up ice as the frequency of boulders decreased, Brunswick had prospected outcropping pegmatite with similar spodumene crystal composition along a 2.7 km trend that was still open to the northeast. This suggests an elongated pegmatite zone similar to the CV5 PMET has at Corvette. Based on spacing Brunswick has reported that there appear to be 5 pegmatite dykes with apparent widths of 25-80 meters and a maximum exposed length of 100 m. The importance of the width depends on the dip of the dykes, which we will not know until they are drilled. If they are shallow dipping the width is not significant, but if sub-vertical the widths represent substantial tonnage potential. The observed strike length is a function of bush, over-burden, swamp and water. What matters is the distribution of outcrops along 2.7 km up ice from a 3,000 m long 200 m wide train of boulders most likely barfed up from this minimum 2.7 km outcrop trend. The market reacted positively to the news because it saw a setting similar to what has delivered a $2 billion valuation to PMET for its Corvette project.

So why did the CEO blow misleading nonsense into my ear? It is impossible that field workers like Francois Goulet were confused about ice direction and its relationship to the boulder field's orientation. The best explanations are that the CEO was very confused because he is so busy interfacing with the market rather than the field, or he fed me misinformation in order to assist with an underlying task of tying up additional ground in this area of fragmented claim ownership. Neither of these explanations pleases me.

On the plus side, thanks to maps being published by others with claims they hope to option to other juniors, and no thanks to Brunswick which has not published any useful claim maps, it is clear that Brunswick has struggled to consolidate its ownership of what appears to be a major new lithium sub-district within the James Bay region. Monday's news release included comments on two option agreements. The more important one was about 8 claims that have been folded into Brunswick's bigger 90% option from the Osisko group which includes Plex, Anatacau West and Anatacau Main. There are no extra payments or spending requirements, but Brunswick nets only 75% in these claims while Osisko is carried to a production decision. If the claim map submitted into the KRO Slack forum by a member is valid, these claims sit inside the Globex option, and while they do not cover the area identified by Brunswick as having pegmatite outcrops, some appear to be immediately up ice.

Brunswick also announced an expensive staged earn-in option on ground owned by IMinerals, which appears to be the successor to a company called 1Lifestyle Holdings which managed to secure extremely onerous terms for pasture proximal to PMET's Corvette project from the Keith Schaefer pump job called Tearlach Resources. My googling efforts to find out who is behind this entity failed, so anybody who does know, feel free to shoot me an email whose source will remain confidential. Tearlach, whose treasury Schaefer helped load has been depleted in such a monstrous manner I may eventually turn the financials into an educational case study of bad management, has almost zero chance of vesting in any of its properties.

I was thus appalled to see the deal Brunswick did. I'm not sure where those 1Minerals claims are located, but it looks like this vendor has lifted at least $500,000 from Brunswick's treasury just to prevent those claims from ending up elsewhere, possibly in Aussie land. I suspect there is a temporary strategic reason for this option, which may allow Brunswick to drop the option before its onerous terms kick in, but I have to admit I am not impressed. In any case, there is clearly a lot of intrigue, and that is one key aspect of a Great Canadian Area Play. Eventually I may learn why it was important to make me look like a fool by feeding me the false perpendicular story, which could prove beneficial to my ownership of Brunswick and the fact that Brunswick is a KRO Fair Spec Value rated Favorite that KRO members loaded up on last year when I tagged it as a Lithium Mania 2.0 linked bottom-fish. But based on basic disclosures it looks like Brunswick has harvested some low hanging fruit which it has threatened to drill in September. I think this story will repeat itself over and over again within the 54 company collection that currently makes up the KRO James Bay Lithium Index.

SOPFEU Map of Fire Situation in James Bay as of Aug 23, 2023

Tentative Map of Brunswick's Mirage Arera

Globex Property Map : Before lithium and after lithium

Brunswick Mirage Boulder-Outcrop Distribution

KRO James Bay Index featuring Brunswick Exploration Inc

Disclosure: JK owns shares of Brunswick and Verde Agritech; Brunswick is a Fair Spec Value rated Favorite, Verde Agritech is a Good Spec Value rated Favorite

Kaiser Watch is a weekly 15-30 minute audio show produced by KaiserResearch.com with Jim Goddard and John Kaiser discussing the junior resource sector. The show has three parts: the first is a general topic, the second discusses developments involving the KRO Favorites which as of January 1, 2022 are no longer exclusive to KRO members, and the third is a peek inside the members only KRO Bottom-Fish Workshop. KRO is transitioning into a Do-It-Yourself research platform that covers all Canadian and Australian resource listings and which also features a Bottom-Fish Workshop where John Kaiser highlights juniors with solvable "missing pieces". Companies that graduate from the Workshop may become part of the Annual Favorites collection whose profiles and related commentary are unrestricted for non-members. Visit the KRO Favorites Dashboard for quick access to all the unrestricted Favorites related content. KRO is not sponsored or compensated directly or indirectly by public companies. The business model is based solely on membership fees in the form of a USD $450 Annual Individual Membership that at some point will increase substantially to reflect KRO's shift to a research platform. However, when the change happens active members will be grandfathered to renew indefinitely at the current rate provided they maintain a continuous paid membership. Kaiser Watch is available at Kaiser Research YouTube and as a Podcast downloadable from KaiserResearch.com. Each episode will be made available through the publication of a Kaiser Media Watch blog report which will provide links to specific questions and include supplementary graphics. All episodes will be archived at Kaiser Watch.

Kaiser Watch August 11, 2023: Time for Canada to fix its First Nations Problem

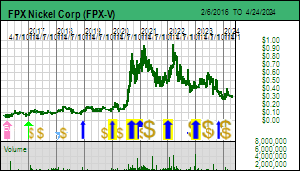

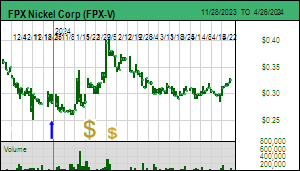

Jim (0:00:00): Why did FPX Nickel drop sharply on Wednesday?

FPX Nickel Corp released a vague Aug 9, 2023 Update on its 2012 MOU with Tl'azt'en Nation which the market didn't really understand until it tracked down the publication referred to by FPX, Dust'Lus Talo 'Ooza' August 2023, a monthly newsletter of the Tl'azt'en Nation. Page 4 contained a declaration by Chief Leslie Aslin, elected in June 2022, that after more than a decade of collecting from FPX Nickel whatever benefits accrued from the 2012 Memorandum of Understanding, the Tl'azt'en Nation has decided it is unequivocally against development of Baptiste, which would become the world's first awaruite based nickel mine in a secure jurisdiction, possibly with a zero carbon footprint, producing more than 4 decades of "clean" nickel relative to the dirty nickel Indonesia and Russia supplies (double that if Van is developed).

This is the same First Nation with a population of 1,802 on and off reserve members (Carrier Sekani Tribal Council which through its Tanizul Timber Ltd division has benefited from clearcut logging within its vast "traditional territory". Some FPX shareholders, in particular Europeans who do not understand Canada's ridiculous First Nations problem, hit the panic button, assuming that this project into which Cliffs and FPX have sunk over $40 million, and for which a mystery strategic investor and the Finnish stainless steelmaker Outukumpu during the past year have invested almost $30 million is dead. If this turns out to be the case, it signals the death of Canada as a nation, because it would confirm that 1 million full status indigenous people who claim 400% of Canada as traditional territory thanks to their overlapping inter-tribal claims, represent a race based aristocracy with rights that over-ride those of the 37 million Canadians who are not descendants of an indigenous nation. It would not actually come to that, for a more likely outcome is that First Nations aspirations will end up on the scrap heap as 95% of Canada's 38 million people declare, "enough is enough", and force the federal government to pull out of the United Nations Declaration on the Rights of Indigenous Peoples.

When you read through the UN declaration it all makes perfect sense until you realize that Canada is the second largest country by area, and all of it technically is traditional territory of various peoples who managed to be the survivors still standing when the Europeans arrived. Unlike the United States which became independent from Great Britain in 1776 and waged physical genocide against its indigenous people and used shotgun diplomacy to strip groups of any legal rights, the British pretty much dealt with Canada's indigenous people by ignoring and marginalizing them. This is now decried as "colonial conquest" and the way generations of Canadians waged cultural genocide against indigenous people is indeed deplorable. But subordinating the interests of 37 million non-indigenous Canadians, most of whom are on their own to secure the means of survival in a modern economy, to those of a 5% minority whose membership is race based and which lineage can easily be established with DNA, just will not happen.

The problem is that Canada's failure to confront its complicity has engendered a guilt complex that encourages pussy-footing around First Nations land claims. Canada has a mineral title system which asserts that the crown owns the sub-surface mineral rights, and where crown land has not been set aside as a park or preserve encourages exploration and development activity by private parties. Canada has erected a massive environmental permitting regime to minimize negative downstream harm, but has not evolved the pragmatic wisdom to accept that when it comes to resource development, you cannot avoid a distribution of costs and benefits that makes some parties winners and others losers. The Canadian mentality is one of seeking ethical purity, which just isn't possible in a world of physical scarcity. There is a latent cowardice in the Canadian unwillingness to accept that whatever decision is made will involve a dirty compromise. Canadians want to be "clean" which has allowed the First Nations problem to escalate to a point where it threatens Canada's viability as a thriving sovereign nation, especially in its emerging role as a producer of raw materials that are critical to energy transition goals and which will also become a secure alternative to metal supply that is destined to become geopolitically compromised as the Global East axis of China-Russia escalates into a hot conflict with the Global West while the Global South aligns itself on the basis of expedience.

One reason Canada has failed to establish a relationship with its indigenous people that balances their interests with those of the 95% non-indigenous Canadians is that the various First Nations groups have these overlapping traditional territory claims. Chief Leslie Aslin's decision to assert a veto right over the future of FPX Nickel's Baptiste Mine, which hasn't yet been validated as economically viable - the PFS due in September will tell us a lot about how vulnerable the economics are to dirty Indonesian and Russian nickel supply - could engender a massive backlash of resentment towards First Nations goals. FPX management has followed best practices in its engagement with local stakeholders, Decar has attracted international investment because of its potential to supply clean nickel for both stainless steel and lithium ion batteries, and the mining plan will be benign relative to bulk tonnage sulphide based mines. This story has the potential to become a publicity nightmare for Canada.

The government withholds drill permits on exploration projects until a company has struck "benefit" agreements with First Nation groups within whose traditional territory the project sits. If there are overlapping traditional territory claims the company has to do a deal with all of them. None of these agreements have a binding nature because the First Nations groups do not have legal rights to the land covered by mineral claims. They are also competing against each other, and not necessarily in a friendly manner. I heard one bizarre story going back to the 1980s when a junior with a copper project on Vancouver Island did a benefits agreement with the local indigenous group. This junior, which was ahead of the times, got a letter from an indigenous group to the south complaining that the junior has no right to do an agreement with that group, that the southern group had kicked this group's ass centuries ago, and has since allowed them to occupy that land at their discretion.

Because a project's potential to deliver a discovery requires a drill permit, the investors in a junior will lose if there is a holdout among these overlapping transitional territory claims. This is comparable to a shopkeeper having to pay protection to multiple street gangs competing for the shopkeeper's neighborhood, none of which agreements are binding and promise no long term protection. These benefit agreements are one-sided because if the junior breaks the terms of the agreement it gets cremated in the court of public opinion with the help of a mindless mainstream media, but if a First Nation scraps the agreement, as the Tl'azt'en Nation has done with FPX Nickel Corp, the junior has no enforcement recourse. Canada needs a good dose of bad publicity for running a mineral claims system that is effectively fraud because the rights a company thinks it has are at the mercy of groups whose decisions have no accountability.

The FPX situation, however, will not result in massive bad publicity for Canada, though if it did the whole world would find out about the Decar nickel project and perhaps start buying the stock. FPX Nickel has been vague in its response to the Tl'azt'en Nation's "Unequivocal No" because it is engaged in confidential discussions with multiple stakeholders. FPX last year announced a June 21, 2022 MOA with Binche Keyoh Bu Society, which is a business organization created after the Binche Whut'en Nation split off from the Tl'azt'en Nation in 2019.

I am not privy to what is going on behind the scenes, but when you scroll to the Appendix you find a map showing the Binche Whut'en Consultative Boundary. The southern portion overlaps the traditional territory map of the Tl'azt'en Nation. When you go to the Tl'azt'en Nation web site you will find a link to the Tanizul Timber web site which has lots of maps and information about the timber harvesting of the past decades, though the financials have not been updated since 2019 when Bince Whut'en Nation split off. The Binche Whut'en web site doesn't have any links to business divisions but its home page currently sports an announcement for a recent fishing derby surrounded by logos of corporate sponsors such as FPX Nickel, Canfor (a forestry company) and Centerra Gold, operator of the Mt Milligan copper-gold mine which is to the east of the Tl'azt'en Nation traditional territory.

The footprint that the Baptiste open pit mine would represent is smaller than most of the logging clear cut patches within the overlapping territories of these two First Nation groups which were once part of the same First Nation group. Given the willingness of the Tl'azt'en Nation to benefit via Tanizul Timber from commercial logging within its traditional territory, it really looks like Chief Leslie Aslin's sudden need "to say an unequivocal No to the proposed mine at Mt Sidney Williams within our sacred territory" is the opportunism of a hypocrite. This really seems to be a territorial conflict between distinct First Nations groups with different agenda. Given that the FPX story has potential to become an international scandal, doing plenty of damage to the interests of both Canada's mining sector and First Nation goals, I do not think this uncertainty about the future of FPX Nickel's Decar project will last long. But in buying at the current distressed prices you do have make a bet that Canada is not as spineless as it seems, and that is hard to do given the current leader and his handlers.

Tl' Azt' en Nation historical desecration of its "sacred" territory

Decar Property and Baptiste Footprint within Tl'azt'en traditional territory

Map of clearcut logging activity from which Tanizul Timber benefits

After the split into 2 First Nations groups, who benefits from logging?

Overlapping traditional territories of Binche Whut'en and Tl'azt'en Nations

Guess which First Nation wants FPX Nickels Baptiste Mine if it is viable?

Jim (0:11:35): Any new developments in the James Bay region?

The main new development everybody is looking for, namely a lifting of the forest access closures, has not happened yet. The main problem is that the western part of James Bay still has an extreme fire danger according to SOPFEU, as a result of which the Billy Diamond Highway remains closed. Although the Trans Taiga Highway which runs east-west in the north James Bay area to service the hydroelectric infrastructure is open, that is of no help because access via Billy Diamond remains closed. The Quebec government's SOPFEU fire map is not well endowed with explanatory legends, but I had somebody explain the legend system. The eastern part of the James Bay region now has a low fire danger though the western part along the eastern side of James Bay has high to extreme fire danger. The irregular red outlined areas are fires that are being "observed", meaning they are being let to burn out on their own because they do not threaten infrastructure. Those that are solid red are still burning actively while those with just a red outline are fading.

There is talk that the Billy Diamond Highway will soon open which will allow road transport to the greenstone belts along the Corvette "trend", which is critical because it will allow boots on the ground which do not need helicopter support to begin prospecting. Companies such as Dios Exploration Inc which were set to do helicopter supported prospecting on their eastern claims by mid August have been notified that there will be a delay of at least another week due to a shortage of helicopters. The Canada wide Interactive Fire Map shows that British Columbia, Yukon and Northwest Territories are now forest fire hotspots. The Yukon, already constrained by a very short exploration season, is now seeing drill programs curtailed because helicopters are being requisitioned to fight its fires. Between First Nation aggression and forest fires the resource juniors operating in Canada are having a tough time, hampered by a market that has become very subdued. Juniors in the James Bay region are consoling themselves with silver lining jokes about how next summer when the winter-spring rains have washed away all the soot there will be a bounty of visible pegmatites previously obscured by brush and moss. Some are already making arrangements for commercial satellite photos next May-June.

At the moment the main hope for major discovery news resides with Brunswick Exploration Inc which has had boots on the ground at its Mirage spodumene boulder field for two weeks now. The stock price has started to sag after a burst of market interest over a week ago when theJuniorExplorer published an hour long interview with Brunswick's CEO Killian Charles. Killian doesn't reveal any secrets about Mirage but the interview does a very good job explaining why what I call Lithium Mania 2.0, the search for lithium pegmatites in places like Canada which don't make anybody's list of where the 600% supply expansion required for 2030 EV deployment goals is supposed to come from, has barely started. It is especially valuable for individuals who feel they missed the lithium boat because they didn't own Patriot Battery Metals Corp. Although investors have been reluctant to act, juniors have scrambled to acquire land in the James Bay region during the past year. I have identified 54 public companies with land in Quebec's James Bay region and created the KRO James Bay Lithium Index with August 1, 2023 as the effective date ($1,000 worth of stock was bought for each company and the index was set at 1,000). The index has been back-dated to December 30, 2022. The index members begin with equal weighting because the point of the index is to identify and track emerging lithium discoveries. I see the James Bay Great Canadian Area Play as the ultimate and final mineral exploration boom ideally suited for the resource junior eco-system which is on its deathbed.

Some of the companies are truly awful pukeworthy juniors which you can tell from the nature of the property deals they have done and the IR contracts in management's history that a pump and dump is the primary objective of exposure to the James Bay Great Canadian Area Play. I decided to include all of them because the nature of the lithium pegmatite hunt is such where the most horrible junior could actually make a world class discovery, so long as they go to the trouble to put boots on the ground. And even that may not be necessary because a serious junior next door might find a CV5 equivalent pegmatite projecting onto the lifestyle junior's property. I've even included gold or base metals focused juniors not (yet) interested in lithium because the kind of geology prospective for those metals in many cases is also prospective for LCT type pegmatites. In fact what makes Lithium Mania 2.0 such a compelling story is that countless pegmatites were noted through the course of past exploration but ignored because as recently as 2005 the annual lithium market was worth only $200 million compared to $20 billion in 2022, and amply supplied by Australia's Greenbushes pegmatite monster and the brines in the Chilean part of South America's Lithium Triangle.

I will be regularly sharing the KRO James Bay Lithium Index chart on Kaiser Watch and talking about important developments, but the KRO James Bay Lithium Index web page and associated comments will be available only to KRO members, which costs USD $450 annually for an individual membership and $1,000 for a corporate multi-user membership.