| |

Tracker - November 29, 2019: Tri Origin takes a big step to avoid a Zombie Spec Value Rating

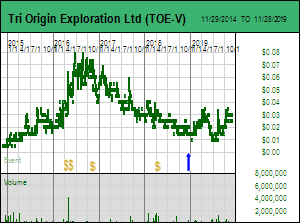

Tri Origin Exploration Ltd was assigned a Bottom-Fish Spec Value rating at the start of 2019 which is in jeopardy of turning into a Zombie Spec Value rating based on a deteriorating balance sheet which at the end of September 30, 2019 shows the junior with $406,000 negative working capital. $195,000 of that amount is owed to CEO Bob Valliant and is convertible at $0.05 into 3,900,000 shares. It shows up as a current liability because it is classified as a promissory note due on demand; it has a one year term which would require resetting the convertibility price if the stock was higher each year it is rolled over for another term. The other $255,000 in current liabilities consists mainly of unpaid salaries due the CEO which accrued during the past 5 years. During this period Valliant has run Tri Origin as a one man show, with moral support from JP Janson, head of wealth management at Richardson GMP. While there is little danger that Valliant, the largest shareholder, would bankrupt Tri Origin, a Zombie spec value rating gets assigned when a negative balance sheet makes it impossible for the junior to undertake any work on its projects that could create new value. Tri Origin ended up in this condition when Sumitomo dropped its option in late 2018 on the South Abitibi project after spending $2 million. De Beers is doing some diamond exploration ground on this property without having done a deal, but the rationale for its interest is not clear and the likelihood that anything interesting will come of this drilling is for the moment low. Despite a portfolio of interesting exploration projects, as the current situation stands Tri Origin does not qualify for a Bottom-Fish Spec Value rating. And the $0.02-$0.03 stock price, periodically dumped on by long term shareholders grown impatient or funds with a manager change and a liquidation mandate, reflects that reality. Tri Origin Exploration Ltd was assigned a Bottom-Fish Spec Value rating at the start of 2019 which is in jeopardy of turning into a Zombie Spec Value rating based on a deteriorating balance sheet which at the end of September 30, 2019 shows the junior with $406,000 negative working capital. $195,000 of that amount is owed to CEO Bob Valliant and is convertible at $0.05 into 3,900,000 shares. It shows up as a current liability because it is classified as a promissory note due on demand; it has a one year term which would require resetting the convertibility price if the stock was higher each year it is rolled over for another term. The other $255,000 in current liabilities consists mainly of unpaid salaries due the CEO which accrued during the past 5 years. During this period Valliant has run Tri Origin as a one man show, with moral support from JP Janson, head of wealth management at Richardson GMP. While there is little danger that Valliant, the largest shareholder, would bankrupt Tri Origin, a Zombie spec value rating gets assigned when a negative balance sheet makes it impossible for the junior to undertake any work on its projects that could create new value. Tri Origin ended up in this condition when Sumitomo dropped its option in late 2018 on the South Abitibi project after spending $2 million. De Beers is doing some diamond exploration ground on this property without having done a deal, but the rationale for its interest is not clear and the likelihood that anything interesting will come of this drilling is for the moment low. Despite a portfolio of interesting exploration projects, as the current situation stands Tri Origin does not qualify for a Bottom-Fish Spec Value rating. And the $0.02-$0.03 stock price, periodically dumped on by long term shareholders grown impatient or funds with a manager change and a liquidation mandate, reflects that reality.

Bob Valliant has decided enough is enough, he cannot wait any longer for this 8 year bear market to turn around and create a natural audience for his exploration ideas, and is biting the bullet in terms of dilution. On November 13, 2019 Tri Origin announced a private placement which could raise up to $650,000 based on 15 million units at $0.03 and 5 million flow-through units at $0.04. Each unit includes a full warrant exercisable at $0.05 for 18 months, with no acceleration clause. Tri Origin has obtained a discretionary waiver from the TSXV allowing it to do this financing below the $0.05 minimum, and while there is a risk Tri Origin may undertake a rollback, it is not a requirement of this waiver as it is in some cases. As part of the TSXV waiver Bob Valliant had to agree that none of the private placement proceeds will be used to repay debt owed to him. So that ugly part of the balance sheet is not going to disappear, but it also won't swallow up new funding.

In addition to being available for hard dollars to both US and Canadian accredited investors, the private placement unit is also available to non-accredited Canadian investors under the existing shareholder exemption. To be accredited you need to have a net worth of at least $1 million not including the equity in your primary residence. The restriction with the existing shareholder exemption is that you can only do up to CAD $15,000 per company per 12 month period. But you can do that with any number of different companies. You must also establish that you are an existing shareholder. Apparently you do this by filling out the Schedule D form in this subscription package. There is no mechanism by which the company or regulators can verify that you were not confused when you filled out that form. Nor are there any consequences if it is later discovered that in fact you were confused about already being a Tri Origin shareholder.

Given that, you might ask, why does this exemption require one to be an existing shareholder? Why can't I just discover a great resource junior story doing a private placement and give my money directly to the company rather than having it be intercepted by some capital stripping day-trading account operated by a brokerage firm employee? Sadly, I suspect the regulators want to be seen as trying to help out the resource juniors raise capital from a broader population pool without actually doing so. If you do not qualify as "accredited" and wish to do more than $15,000, you must get a registered representative to sign off on a statement declaring that such an investment is "suitable" for you. If you are a Boomer, meaning aged 55 or older, that will not happen, not just because the broker's firm won't allow it, but also because the broker gets no commission through completing that pain-in-the-ass declaration, which also applies to Post Boomers. But even if you are a Post Boomer, it wouldn't be wise to do more than 500,000 units at $0.03, which would give control over 1 million shares over the next 18 months.

Will Tri Origin emerge from its decade long drift below $0.10? On November 20 three highly experienced individuals who had joined the advisory board in early 2019 agreed to become full directors. This financing is an attempt to relaunch Tri Origin which has never undergone a rollback since going public in late 1991 with Valliant at the helm. The "tight structure" pump and dump crowd will sneer at Tri Origin's 167 million fully diluted if this financing is completely done, but the cheap financings in their rig jobs aren't available to the masses. During this long period Tri Origin has maintained a dual focus on Ontario and Australia which ended in 2009 when the Australian assets were spun out as a separate entity that listed on the ASX. Valliant is a geoscientist who did his PhD on the Bousquet-Laronde deposits within the Abitibi greenstone belt, which has driven his ongoing interest in VMS and gold deposits since leaving Lac Minerals in 1988 when his role as Exploration VP became redundant. He was also involved with the exploration of the Hemlo discovery on behalf of Lac which lost the Williams Mine in 1988 to the Corona successors in a court battle which ruled that Lac violated a confidentiality agreement when it acquired the property. Since the Australian asset spinout in 2009, however, Tri Origin has been trapped below $0.10 while Valliant kept the company alive as a one-man show. The $650,000 alone likely will not change the company's fundamentals, but it sets the stage for a higher profile that may enable the junior to raise more substantial financing. Maximum completion of the financing would push fully diluted to 167.6 million shares, and there will be a risk that in four months 20 million shares get clipped from the warrant and flipped into the market as a free lunch for the holders. But that may not be a problem if Bob Valliant switches his marketing strategy from the cannabis fried brokers on Bay Street to a Post Boomer audience just starting to discover the junior resource sector. In a certain sense I see Tri Origin as an experiment to test the idea that Post Boomers can come to embrace resource juniors.

The exploration focus for Tri Origin in 2020 will be the 27 km long 12,800 ha Sky Lake project in western Ontario located between the Red Lake and Pickle Lake districts. The Red Lake district and the surrounding region made headlines the past week when Evolution Mining Ltd (EVN-ASX), an ASX listed mid tier gold producer, purchased from Newmont the Red Lake assets owned and operated by Goldcorp prior to its acquisition by Newmont in 2019. The price for the 7 million ounce gold resource at 11 g/t gold and associated infrastructure was surprisingly low at USD $375 million plus $20 million for each additional million ounces discovered by Evolution up to 5 million ounces. Evolution has signaled its intent to give the surrounding region within a 150 km radius a fresh look, creating new hope for exploration juniors that if they find something, there will be a possible exit strategy. Tri Origin's Sky Lake project sits beyond Evolution's circle of interest, but for all practical purposes it and the Pickle Lake district are within Evolution's new stomping grounds.

The heart of the Sky Lake project is a 200 hectare parcel of patented claims optioned 96% in November 2016 from Barrick for $500,000 exploration over 4 years and a 0.5% NSR. At the time Tri Origin owned 84.3% of 20 "boundary" claims and 100% of 11 surrounding staked claims for a total of 4,400 ha. The deal allows Barrick to back in for 51% of this claim package upon Tri Origin completing a positive feasibility study. The back-in purchase terms have not been disclosed. Bob Valliant believes that this area has the potential to host Bousquet-Laronde type gold deposits, essentially VMS systems that have undergone a major gold overprint. He has since tripled the land position to cover 27 km of prospective geology, most of which is not subject to the Barrick back-in right. The Barrick back-in is a funding obstacle which Tri Origin will eventually have to negotiate away. The Barrick claims host a gold system discovered during the 1950's when first Pickle Crow Gold Mines Ltd and then Hasaga Gold Mining Ltd explored the property. Eventually Lac Minerals inherited the property and conducted several drill programs including the last one in 1986-87. Valliant was in charge of Lac's exploration team and was given the job of firing everybody which he rejected by declaring that he could not continue if this was Lac's strategy; the board meditated on this ultimatum briefly and told him, yes, when you are done you are also fired. Following a definitive court decision in 1989 that Lac had to forfeit the Williams Mine to Corona the producer lost its way and was acquired by Barrick in 1994. Barrick had no interest in eastern Canada and sold key gold assets such as Laronde. Sky Lake was so insignificant it stayed lost inside Barrick until Valliant who has a long memory came knocking.

From 1950-1990 the core Sky Lake claims had 133 holes drilled into them to a maximum vertical depth of 150 metres with most drilled 50-100 m deep. This resulted in a small non-43-101 compliant historic gold resource. Tri Origin has spent $1.7 million on the overall Sky Lake project but is only half way through the $500,000 obligation to Barrick, which means that it must spend another $250,000 in 2020 to vest. In 2019 Tri Origin completed a deep penetrating IP survey which revealed potential at depth that will require 500 m holes to test. All the historic data is being compiled to form the basis for a 3D model expected to be ready by early January. Part of the $650,000 financing will be used to establish the geology at depth and provide a case for an expanded program; a side effect will be to vest Tri Origin for 96% at which point it becomes feasible to approach Barrick about the back-in right. The 2020 work will also set the stage for exploration along the 27 km trend covered by the Sky Lake property.

A group of inlier patented claims in the eastern half called Kasagiminnis hosts a similar gold system owned by Ardiden Ltd (ADV-ASX) for which it published a JORC resource estimate of 790,000 tonnes at 4.3 g/t in September 2019. It is only 110,000 oz but Ardiden is planning a major winter drill program to expand the deposit along strike and at depth. Ardiden acquired the project from a moribund Canadian junior, and until recently was focused on Ontario's graphite and lithium potential. But in the past year there was a management change and the focus is now on gold in western Ontario, a smaller version of the wave of Australian interest washing ashore in Canada. Another landowner in the region is Exiro Minerals which is headed by Shastri Ramnath and Josh Bailey. Exiro's strategy is to conduct regional data compilations to which it applies "big data" analysis to highlight under-explored areas with potential. Haywood's David Elliott is a disclosed backer while Rick Rule is rumored to be a hidden backer. When you consider that Great Bear Resources Ltd has achieved a $250 million valuation based on its ownership of a 23 km structural trend south of the Red Lake camp, the $5 million value at $0.03 implied by Tri Origin's 167 million shares fully diluted after the financing looks pretty cheap. Ardiden with 1.7 billion shares fully diluted and a $0.003 stock price is also carrying a AUD $5 million value for the 4 far flung projects that make up its Pickle Lake play, but with 10 times the amount of stock out, Ardiden makes Tri Origin look like a tight deal.

During 2019 Tri Origin gave up on its Detour West project covering the western extension of the Sunday Lake Deformation Zone that hosts the Detour Lake gold mine which Kirkland Lake is acquiring. But Tri Origin continues to maintain the 5,000 ha North Abitibi project which is located on the Ontario side of the Casa Berardi Break and is adjoined by Detour Gold to the east and to the west by a private company called LaSalle Exploration Corp headed by Ian Campbell. This area has extensive overburden cover and has seen little exploration beyond drilling Tri Origin has conducted along its 8 km segment of the trend. North Abitibi could end up being a farmout to LaSalle if it ever gets public, something that may be in the works given that its web site has been stripped of all content.

Tri Origin still holds 100% of the 2 blocks that made up the South Abitibi JV it had with Sumitomo; the northern one is called Nipissing Cobalt and the southern one Southern Abitibi. Most of this area was off limits to exploration for decades after the Bear Island Caution was issued in response to unresolved First Nations territorial claims. The surface rock is the Proterozoic aged Cobalt Embayment, a sedimentary sequence which became host to high grade silver-cobalt veins that became the basis for the Cobalt mining district. The Cobalt Embayment sits on top of Archean rocks and thickens toward Sudbury. When the staking moratorium ended Valliant staked these claim groups in the eastern part with the hypothesis that the sedimentary cover would be only a couple hundred metres thick above the Archean aged Abitibi Greenstone belt whose deposits are geochemically "under cover" and only visible to geophysical surveys. The exploration strategy was to use geophysical surveys to identify potential VMS targets as well as structures with gold potential. Drilling funded by Sumitomo did confirm the general hypothesis but failed to deliver a discovery hole and the Japanese company lost interest in late 2018. During the 2016-2018 period cobalt spiked to $40/lb and the Cobalt Plate received new exploration interest, in particular from small juniors milking the latest metal price bubble. Sumitomo was not interested in cobalt so all things related to cobalt unearthed by field work was ignored. Now once more nobody cares about the cobalt potential, but in 2019 De Beers approached Tri Origin with an unusual proposal.

In September and October of 2019 Tri Origin announced that it had given permission to De Beers to drill kimberlite targets the diamond producer had identified on the two claim blocks. Although Tri Origin had the data from the airborne magnetic-EM survey generated by the Sumitomo JV, De Beers seems to be relying on its own geophysical data, meaning that it must have flown this region to the southwest of Cobalt. The Tri Origin "permission" granted De Beers one year to spend its own money drilling these targets, provided it would share all information with Tri Origin. If De Beers wished to do so, the two parties would negotiate a "standard" industry agreement. I pressed Bob Valliant about the structure of the "standard" deal, but he would only say that it would conform to his goal that Tri Origin would not be required to contribute any exploration cash until at least a production decision, and still be left with a meaningful net interest in the project. His reasoning was that Tri Origin's mandate was to be a base and precious metals explorer where he possesses a core competency, and he was also aware of the Peregrine Factor where $100 million was spent on quality exploration at Chidliak on Baffin Island to deliver a new field of kimberlites that included several high grade pipes with high value diamonds but only garnered $124 million from De Beers, a mere $14 million premium for all that success! The junior diamond exploration sector is in worse shape than before Fipke found Ekati, though there is now a public knowledge base which could ramp up interest very quickly if something new and special emerged.

De Beers has not explained why it is interested in this area south of Cobalt where there are no known kimberlites, in contrast to a 130 km by 75 km block from the Destor-Porcupine Break down to Cobalt where dozens of kimberlites have been discovered, none which have yielded a macro grade above 10 cpht. Perhaps this new area is of interest because its closure to staking prevented any exploration, even after Dia Met kicked off the Canadian diamond boom with the discovery of Ekati in 1992. Recently another junior called RJK Explorations Ltd has revived interest in diamond exploration immediately south of Cobalt where the 800 carat Nipissing yellow diamond was found around 1903 when the silver veins were discovered. This diamond was sold and cut into smaller diamonds whose whereabouts are unknown so it is impossible to determine what type of diamond it might have been. The understanding about very large diamonds is fairly recent, though giants like the 3,000 carat Cullinan diamond were found a very long time ago. Interest in Type IIa diamonds emerged after De Beers gave away the smallish, low grade AK6 pipe in Botswana which dazzled the world after Lucara put it into production as the Karowe Pipe. It seems that Type IIa diamonds form "super deep", between 400-600 km depth in an environment created by underplating the craton with subducted oceanic crust. Type IIA diamonds are thus younger and different from the peridotitic and eclogitic populations that form at shallower depths and constitute the vast majority of all diamond production. A kimberlite magma starts its ascent even deeper and entrains different diamond populations from the "growing fields" encountered along the way, ultimately blending them into what appears to be a single diamond population. But what if the shallower populations got wiped out in this part of Ontario by some sort of thermal event that was gone after the oceanic slab underplating began? What if later kimberlites only sampled these Type IIa populations which may not exhibit the lognormal size distributions of the other diamond types? Their presence would not be detectable with micro diamond analysis, nor would pyrope and eclogitic garnet chemistry be diagnostic about their presence. Maybe De Beers has figured out the magic bullet chemistry for Type IIa diamonds just as was the case many decades ago with G10 pyrope chemistry? It could dump a file of factual chemistry on Bob Valliant's desk that might as well be hieroglyphics before the Rosetta Stone was found. The message would be, "we have nothing yet in terms of diamond content to get excited about, but we need to spend lots of money, and if you think you are lucky, give us an easy deal so that we give it a shot". The risk De Beers is otherwise taking would be that really good micro diamond size distribution curves would enable Tri Origin to tackle the "pipes" on a 100% basis and thus evade any right of first refusal conditions likely attached to the "permission to drill".

The future for natural diamonds in the smaller size categories has grown cloudy with the arrival of synthetic gem diamonds and an unwillingness by Post Boomers to differentiate between natural and synthetic diamonds, or worse, prefer synthetic diamonds because they supposedly have a smaller greenhouse gas footprint. However, I suspect that large, gem quality natural diamonds will have a collectible value that will never be matched by the synthetic equivalent which will be dismissed as crass "bling". Canada has not shown the presence of Type IIa diamonds except in the Fort a la Corne kimberlites which may explain why Rio Tinto has earned a majority stake in these low grade deposits. Why would De Beers spend time, money and effort in this region south of Cobalt if the best one could hope for is higher grade versions of the kimberlites in the New Liskeard and Kirkland Lake clusters? The interest of De Beers in this area is a mystery, and it may simply be the banal case that De Beers is on auto-pilot mechanically exploring the final frontiers with no expectations beyond "more of the same". Or maybe my speculations about the Hunt for Type IIa diamonds are valid and some sort of recent deep seismic work by the academics has revealed something about the Super Deep part of the Superior craton in this area that is different from the area to the north. The Lake Temiskaming Structural Zone is said to sit on top of s deep-seated subduction zone. Since Tri Origin has a large land exposure to this area, land that would attract exploration dollars if we ever again get a bull market for base and precious metals, getting a free diamond lunch from De Beers strikes me as a pretty good extra reason to place a bet on Bob Valliant's efforts to relaunch Tri Origin as a serious Ontario focused exploration junior. I am thus continuing the Bottom-Fish Spec Value Rating for Tri Origin Exploration Ltd on the assumption the financing will get done, and recommend that instead of buying the stock in the open market, Spec Value Hunters participate in the private placement which gives a full 18 month warrant and substantial upside for a small investment if the relaunch is successful and we get a resource sector bull cycle going that attracts bigger scale capital from the more usual accredited suspects for Bob Valliant's big picture discovery dreams.

*JK owns shares in Tri Origin Exploration Ltd

|