The gold juniors have so far not responded to the six week uptrend in the price of gold because it is too soon to tell if $2,000 is indeed the new floor for gold rather than its ceiling. Gold producers have responded but their ability to post further gains will require gold to establish $2,500 as a new trading level where the real price gain is 61%, not really a meaningful monetary difference, but it is the optics that count. I have two juniors in my 2024 collection which represent opposite extremes for how to play the non-producing juniors with exposure to gold.

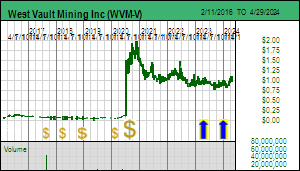

The first is West Vault Mining Inc which owns the Hasbrouck project in Nevada near Tonopah. Hasbrouck consists of two deposits that will be open-pit mined and heap leached at 17,000 tpd over an 8 year mine life during which it would produce 561,000 ounces. This project is shovel ready with all development permits in place, and the PFS was updated in January 2023 so the CapEx and OpEx numbers are reasonably reliable. At the base case price of $1,790 per oz gold the project has an after-tax IRR of 48% and net present value of USD $135.3 million at 10% discount rate and $192.6 million at 5%. Based on 59.5 million shares fully diluted and an exchange rate of 0.74 USD for 1 CAD this translates into an NPV per share range of CAD $3.09 to $4.37. The stock has been stuck in the $0.90-$1.00 range but managed to creep up to $1.03 on Thursday. The biggest shareholder is Sun Valley Gold LLC whose head Peter Palmedo has made a strategic decision to forego any further exploration activity or project diversification and just maintain West Vault as a target for a future buyout. This allows West Vault to serve as a leveraged proxy for the price of gold.

For example, at the current gold price of $2,214 the DCF model using the PFS costs generates a 79.5% after-tax IRR and a NPV per share range of CAD $5.52-$7.41. If you dare to dream of $4,000 gold without serious cost inflation, those numbers blossom to $15.75-$20.22 for 10% and 5% discount rates. The market is ignoring West Vault because it sees annual production potential of only 70,000 ounces gold, and is concerned that no producer will want to acquire and develop Hasbrouck. Given the recent mood about the future of gold and the gold mining sector compared to just gambling on a Bitcoin ETF, this aversion is understandable. But this is what gives West Vault Mining Good Speculative Value. The key development needed to turn West Vault into a $5-$10 buyout is a secular bull market for gold that fosters expectations for a higher real price for gold, and the decision by a producer to consolidate the region surrounding Tonopah and turn West Vault into the initial mine. West Vault is an example of an ounce-in-the-ground story whose feasibility has already been demonstrated and which is waiting for the right market conditions to attract a buyout in the $5-$10 range.

The other extreme is Solitario Resources Corp which is a gold exploration junior waiting for the USFS to approve a drill program for the Golden Crest project in the western part of the Black Hills area of South Dakota. The eastern part is home to the famous Homestake Mine which produced 65 million high grade ounces from basement hosted iron formation rocks, plus another 30 million ounces, some of them hosted in the much younger Deadwood formation sediments. For reasons I have described in prior KW episodes the western half of the Black Hills area received very limited exploration during the past century while the mining action was in the eastern half. One reason is that the cover rock is younger than the Deadwood Formation which hosts the Wharf gold system being mined by Coeur. Another is that the gold Solitario has found at surface is so fine grained it would not have shown up in the pans of early prospectors. So the western half of the Black Hills covered by Solitario's Golden Crest claims was stigmatized as unprospective. This is evident in a LIDAR survey over the entire Black Hills which reveals 150,000 prospect pits on the eastern half, but only 1,500 on the western half.

Solitario is an extraordinary discovery exploration play because since generating Golden Crest in 2020 the company has conducted extensive soil and rock sampling on the property which has yielded multiple areas with high grade gold values in the rocks at surface. The latest news has been on the Ponderosa block to the east of Spearfish Canyon near Hanna where the Geyser and Sleeping Beauty targets have now been recognized as a northeast trending area of interest 3 km by 2 km. The Ponderosa Plan of Operations was applied for in 2023 so these targets will not be permitted for drilling until 2025. For now Solitario is waiting for the final response by the USFS to the comment period objections made about the Golden Crest Plan of Operations. Approval is possible in the second half of April, though in a country haunted by permitting obstacles and anti-mining lifestyle NGOs no discovery is possible until a drill permit is granted.

Solitario has USD $8.3 million working capital and only 87 million shares fully diluted, which means that the implied value of Golden Crest is CAD $71 million at $0.81. If you assume that is fair speculative value for a project still at the target testing stage, the implied outcome is potentially worth CAD $4 billion if there is no further dilution bringing the project to the production stage. In per share terms that translates into a CAD $46.29 price target. Normally it would take 5-10 years to take a project from the discovery delineation stage into production, but resource junior market dynamics include something called an S-curve, also known as the Lassonde curve, which reflects the fact that during the excitement of a new discovery whose limits have not yet been delineated, the market can end up assigning a valuation during discovery delineation that matches what the project eventually ends up being worth when ready to go into production. Add in the fact that Solitario also trades on the NYSE with the symbol XPL, meaning it is eligible for Robinhooders to trade, this stock has the potential for mind-boggling gains. To be ultimately worth $4 billion Solitario will need to demonstrate 10 million plus medium grade ounces which would be quite an accomplishment. What makes Solitario so interesting is that thanks to circumstances created by mother nature Golden Crest could be sitting on a mirror image endowment of what has already been found in the eastern half of the Black Hills. This is what could drive crazy S-curve dynamics, even if the price of gold slumps back below $2,000. For West Vault to turn into a ten-bagger the price of gold needs to keep trending above $2,000; for Solitario to become a ten-bagger it needs to delivery a discovery with grade and size that works at whatever gold price we have. |