The James Bay Lithium Index, which now has 70 members, had a good week, managing to close up modestly every day, but it is still down 23.3% from August 1, 2023 when I created it. Lithium Mania 2.0 has by no means caught on with general audiences. The lithium carbonate price weakened this week again as more bad economic news emanated from China which retaliated against western moves to limit export dumping of state subsidized electric vehicles by declaring export restrictions for natural and synthetic graphite. This is really a warning shot about potential measures that would be much more drastic for car makers outside China. While China dominates in graphite production from natural sources, and making synthetic graphite from hydrocarbon sources, the rest of the world could easily ramp up synthetic production from hydrocarbons, especially the United States. But because China is the lowest cost jurisdiction (don't mention the downstream victims of lousy emission and worker safety standards), everybody is happy to import cheap Chinese graphite. The same applies to gallium and germanium whose export China has also restricted; the way to strip gallium from bauxite conversion to alumina and germanium from zinc smelters is present outside China when the will to do so develops.

Rare earths are another matter, but apart from Japan, what non-Chinese nation makes the rare earth based magnets required for electric vehicles? China exports magnets made from its super-abundance of rare earths, and it is unlikely China will curtail the export of a value added down stream product. However, if supply curtailment turns out to be not China's explicit choice, but rather a functional by-product of western reaction to Chinese aggression such as trying to annex Taiwan or becoming more overt in supporting Iran's proxy war against Israel and Russia's invasion of Ukraine, then Global West car makers will have a problem. And everybody has their heads in the sand about the future rare earth supply problem. Not so, however, about the future lithium supply problem. Although Goldman Sachs thinks China will become a limitless supply of cheap lithium, nobody else does. The corporate takeover actions of major lithium suppliers like Albemarle and SQM in Australia signal that nobody believes China will own global supply for lithium as it does for rare earths, antimony, graphite, and tungsten. China's stranglehold on lithium today involves downstream refining of spodumene concentrates into battery grade lithium hydroxide and carbonate. This vulnerability, however, is well understood, and so it only takes an abundance of will to harness the existing way into conversion capacity outside China.

The scramble afoot now is to secure the future lithium supply needed for an EV sector on an unstoppable track to displace ICE cars. Nothing highlights this more than SQM's decision to try to buy out Azure Minerals Ltd for the astronomical implied amount of AUD $2.4 billion before Azure even has a maiden resource estimate for its Andover pegmatite field which nobody knew about until just over a year ago. Meanwhile, Patriot Battery Metals Corp, which had a similar implied value for its CV5 maiden resource and on trend expansion potential when Albemarle invested CAD $109 million to acquire a 4.9% equity stake in August, is bumbling along at a value of about CAD $1.6 billion. Is this a Prime Minister NoCanDo discount being applied to Canadian resource projects? Gina Rinehart has injected complexity into SQM's straight forward bid for Azure's 60% stake because Mark Creasy, owner of 40%, represents a wild card. However that plays out, what matters is that Gina is no longer just looking at near term production assets, but is also looking at emerging pegmatite lithium discovery plays with world class footprints, discoveries that will not come into production before 2030. Gina Rinehart now personifies the vision of lithium supply becoming a $100-$200 billion market in the 2030's, not as big as iron, but rivaling copper and aluminum, and gold if you want to include useless metals. The iron lady is brushing aside the iron men as if they were mere tin men from the land of Oz.

Next week is important for the James Bay juniors because the AEMQ will hold its annual mining and exploration XPLOR 2023 conference in Montreal from October 30 through November 2. Only 8 James Bay Lithium Index members are exhibiting, but I am sure representatives of all the serious juniors will be present to network and sponge up information. Hopefully government officials will be plugged into what is happening in the James Bay region. The Abitibi greenstone belt activity at this stage is largely a mechanical process which cynics might even dismiss as lifestyle activity. There is zero buzz about Quebec's gold potential. Nor does anybody care about base metal projects. The buzz is all about Quebec's lithium potential, with anxiety focusing on what stance Quebec's First Nations will ultimately take about the development boom in their backyard, and to what Canada's Prime Reconciliation Minister will do to stymie mine exploration and development.

This conference I wish I were attending so that I could take the pulse about the will to turn Quebec into a critical supplier of the lithium needs of the energy transition. The ones I attended during the past decade were fun while held in Quebec City, because they had the cozy feel from when PDAC took place in the Royal York and Roundup in Hotel Vancouver. But the later ones in Montreal were held in this dreary Soviet style concrete dungeon attended by very few delegates, though the low attendance was because the resource junior bear market had extended well beyond the usual 2-3 years of gloom. Attendance was so sparse in 2015 I got to hang out with the Osisko gang (and discover why all these new Osisko juniors were named after scotch brands) which enabled me to have a chat with Bob Wares. I had noted unusual zinc-lead-silver assays coming out of the Hermosa-Taylor project of Arizona Mining, and because Bob was a director we started chatting about it. Based on that happenstance conversation I took a closer look at it, tagged it as a $0.35 bottom-fish for the 2016 collection, and, after I met Don Taylor at the VRIC conference in January 2016 who walked me through the geological story, I turned it into a major recommendation whose $2.2 billion South32 buyout outcome at $6.25 I accurately projected with the help of my rational speculation model, outcome visualization method, and IPV charts. That was so long ago.

Lithium Mania 2.0 was premised on the idea that after the Canadian awakening in 2022 about the world's future lithium supply needs the summer of 2023 would be the most intense "boots on the ground" prospecting season in the history of Canadian exploration. Alas, nobody foresaw that in 2023 Canada would go up in smoke. The most depressing moment for me this year was that weekend in early June when word got out that most of Quebec had been closed to exploration due to unprecedented forest fires. Not only were vast regions closed for safety reasons, but all air transport equipment such as helicopters were requisitioned to support fighting fires in the vicinity of threatened communities. This was not something on could complain about. It was a shot from left field that had to be absorbed. The James Bay region lost two critical prospecting months, and in many areas even August was not accessible. Most juniors got boots on the ground in early September, but many of them had to cease work on September 15, the beginning of the Cree moose hunting season which runs until October 15.

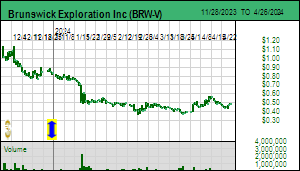

As a result only a handful of juniors are currently drilling pegmatite targets, and only a handful have done enough target development work to justify mobilizing a drill program in Q1 of 2023. Not much gets done during Q2 in the James Bay region other than wrapping up drill programs because spring thaw is a nasty, foggy time of the year, and May is the Cree goose hunting season. Work does not resume until late May when the fog has dissipated and the ground is exposed for prospecting. But within several days of prospecting kickoff in 2023 all field crews were called home to sit out most of the summer. The only consolation emerging from the lost 2023 exploration season is that so much forest burned that 1) not much is left to catch fire in 2024 if we get the same intense conditions, and, 2) a lot of otherwise hidden outcrop will be exposed after the spring rains have washed away the soot. In rugged terrains like northern British Columbia the retreating glaciers give prospectors fresh hope to discover newly exposed goodies, but the glacial retreat is of an incremental upslope nature. The vegetation "retreat" caused by the 2023 forest fires will be laterally monumental. I might add that a third consolation is that all those people who felt they missed the boat will have in fact missed only a very few boats. One I think they will have missed which I introduced in Q2 of 2022 is Brunswick Exploration Inc which has done sufficient work to shortly be in a position to lift off in the manner Azure Minerals did in June 2023.

On September 7, 2023 Brunswick Exploration Inc announced that it had started a 5,000 m drill program at its Mirage project. On October 3 Brunswick reported that it had drilled 1,000 m representing 15 holes of which 12 had intersected spodumene bearing pegmatites up to 52 m in width. A big question with pegmatite outcrops is the orientation and extent of the bodies beneath the surface. "True width" talk is not allowed until drilling has sorted out the geometry. Brunswick indicated assays would be available in the second half of October. Brunswick, unlike Azure, has not been overly helpful with providing graphics to help shareholders understand what is unfolding. KW Episode October 6, 2023 is the most recent discussion about what might be going on at Mirage. An update early next week ahead of the XPLOR conference in Montreal is reasonable to expect. Mirage has the scale to be comparable to Azure's Andover pegmatite field. If Gina Rinehart knows about Canada, and Brunswick delivers evidence that Mirage is a major emerging lithium discovery, be prepared to hold onto your hat. We already know Albemarle knows about Canada. The real question is whether or not SQM also knows about Canada. SQM so far is missing in action as far as Canada is concerned, but SQM did have a booth at PDAC this year along with Albemarle. In light of what happened with Azure Minerals the past week, do not be surprised if positive news from Brunswick about Mirage lights a fire under the James Bay Great Canadian Area Play. |