Hello Guest User, You are visiting this website from a computer with an IP address of 172.71.254.69 with the name of '?' since Fri May 10, 2024 at 1:53:56 AM PT for approx. 0 minutes now.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

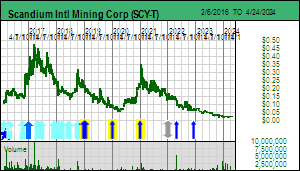

The big news for Scandium International Mining Corp is that Barrick in its Q1 2021 results presentation on slide 20 declared that with regard to its gold-copper Phoenix mine in Nevada (61.5% Barrick, 38.5% Newmont) it stated that it has "Initiated a study on the potential recovery of selected critical metals from the SXEW raffinate, in partnership with a local third party". The slide in the Q4 2020 results presentation dealing with Phoenx and Long Canyon made no such statement. The fact that Barrick would include the reference to the CMR study in a corporate presentation that will be reviewed by its huge institutional shareholder base suggests that this study is well advanced and is showing a lot of promise. Who could that local third party be? Scandium International held its AGM on the morning of June 3, 2021. Maybe 5 shareholders were on the Zoom call and asked questions. One brought up the Barrick slide comment with the suggestion that the partner is unlikely to be anybody but SCY. The CEO's response, rather than just plead "no comment, all our CMR dealings are under non-disclosure agreements", insisted that it is possible Barrick is dealing with another party. That would truly be amazing if somebody else based in Nevada has managed to get Barrick to participate in a study about recovering certain critical metals from a copper SXEW raffinate. I feel so sorry for SCY's CTO Willem Duyvesteyn who is the driving force behind SCY's CMR strategy if Barrick is indeed referring to another group. But the CEO is only correct in a logical sense; in probability terms his response is an arrogant dismissal of the shareholder question. In response to another question about better disclosures, the CEO pronounced that "shareholders can follow the bread crumbs by reading the 10K and 10Q filings". Well I have been doing that, but the need to do that presents a strong case for a change in corporate culture at SCY.

For whatever reason the SCY management is doing its best to discourage the market about the company's future. It still has not updated its March 2020 corporate presentation to reflect the shift to the CMR strategy and the pursuit of HPA production. Neither has the company said anything about Rio Tinto's breakthrough at Sorel-Tracy in recovering scandium while upgrading its 80% titanium slag to the 95% rutile equivalent TiO2 grade now required by pigment makers. No discussion that Rio Tinto now has an incremental scandium supply growth strategy that can spawn scandium demand gradually, overcoming the chicken-egg problem without a huge risky upfront CapEx investment. SCY's CMR strategy, for whose scandium recovery it already has a patent, can deliver the same incremental growth. Once SCY gets a CMR hosting deal, it and Rio Tinto can build out the offtake market for scandium which has a long term potential to grow to 1,000 tpa Sc2O3. If either is successful, building global supply into the 50-100 tpa range with offsetting demand, that will be the tipping point for rapid demand growth which can only be served by developing larger scale primary supply, for which role SCY's Nyngan project is ready. In late 2019 the scandium chicken-egg problem looked hopeless and Nyngan had become worthless because there was no plausible timeline for its development. But copper SXEW CMR and Sorel-Tracy changes everything. The Nyngan asset now has a future, maybe being developed 3-5 years from now when scandium demand takes off.

It has an optionality value that should be reflected in the SCY stock price ahead of any progress on the CMR or HPA fronts. Not just as a 35 tpa output project as defined by the 2016 DFS, which exploits only a fraction of the resource, but one that expands operating capacity in cash flow funded stages to 4 times the initial capacity. To see what this expansion might be worth to Rio Tinto if it has success with its Sorel-Tracy plan, I have done a discounted cash flow model of this expansion scenario. Assuming the $2,000/kg price for Sc2O3, the expansion scenario has an after tax NPV value of USD $762 million at 5% discount rate and $414 million at 10% which translates into a stock price range of CAD $1.43-$2.64 at current exchange rates and 349 million fully diluted. That is the range one might expect Rio Tinto to pay down the road when it needs to expand its scandium supply beyond the 50 tpa limit from Lac Tio ore at Sorel-Tracy. But we don't know how far down the road that will be, and with a project stuck at the completed feasibility study stage with no funding to move on to construction, the fair speculative value range for this future outcome is 50%-75%. Thus at the 10% discount range SCY should have an optionality value range of $0.72-$1.07, and if you push it to a 5% discount rate, the range is $1.32-$1.98. SCY should be trading between $0.50-$1.00 just on the optionality value of Nyngan alone, before any value is added for the CMR and HPA plans. In fact when you consider the future development potential for Keviniemi and Honeybugle, the value should be even higher. When you consider that SCY has mastered downstream master-alloy capability, and can branch into recovering critical metals other than scandium from various waste streams in premium commanding high purity forms, the company is a candidate for a bubble stock. The corporate culture should include promoting all this potential, not demoting it.

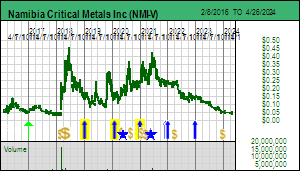

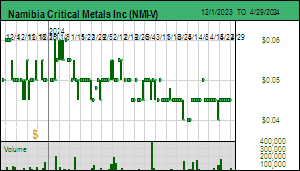

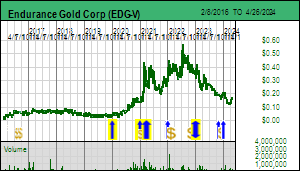

Disclosure: JK owns Endurance Gold, Namibia Critical Metals and Scandium Intl; Endurance is a Good Spec Value rated Favorite, Namibia Critical Metals and Scandium Intl are Bottom-Fish Spec Value rated Favorites