Hello Guest User, You are visiting this website from a computer with an IP address of 172.69.6.233 with the name of '?' since Fri May 10, 2024 at 9:28:54 AM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - July 1, 2020 to July 31, 2020

Kaiser Media Watch Blog enables John Kaiser to share online content from other media he deems interesting or relevant to Kaiser Research Online audiences. He collects links to such content and writes a brief explanation. The KMW Blog gets updated during the evening KRO update. After a week or so the current KMW Blog gets archived and a new one is started. Tweets are sent with a link to the item in the KMW Blog when it is of particular interest. Right clicking the JK header allows one to share or copy a link directly to that specific blog post.

This 33 minute interview by Charlotte McLeod of Investing News Network was done on July 29, 2020 and posted by Investing News Network (INN) on July 30, 2020. (Direct YouTube Link). It was remarkable how much vitriol it attracted from the somewhat less than half of the potential American audience I wasn't expecting would pay any attention to it.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered as Bottom-Fish and Spec Value Hunter picks and will include projects that may be of interest only because they are in the limelight. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. KRO will keep track of projects mentioned through Discovery Watch with HoweStreet.com. Discovery Watch is available via YouTube or Podcast.

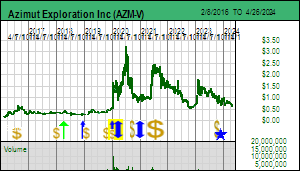

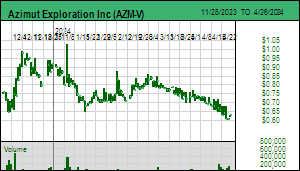

Azimut Exploration In was introduced to Discovery Watch in September 2016 due to its minority stake in the Eleonore South project in the James Bay region of Quebec which covers the southern half of the Cheechoo intrusion where Sirios Resources Inc caught the market's imagination in early 2016 by rethinking a low grade bulk tonnage gold optionality into a potential high grade underground mineable system. Sirios started drilling the intrusion with NE oriented holes instead of SW holes and while initially this seemed to deliver high grade intervals more consistently, after several years it became apparent that the Cheechoo intrusion did not host coherent high grade zones that would lend themselves to underground mining. Sirios has since reverted to a bulk tonnage model and published a resource estimate in late 2019. Azimut's CEO Jean-Marc Lulin became the champion for Eleonore South which it had staked during the early days of the Eleonore discovery by Virginia. Work by Goldcorp and Eastmain failed to deliver a discovery because it was focused on the margins of the Cheechoo intrusion. JML focused on potential high grade zones such as Moni, but that effort grounded out just like that of Sirios. Today it is clear that Eleonore South and Sirios' Cheechoo needs to be consolidated as one property with a large open pit operation which has the support of Newmont (after acquiring Goldcorp), which is also a major shareholder of Sirios. The stick in the mud resisting a win-win proposal has been Azimut, which stopped funding its share of Eleonore South in 2018 when it decided to violate the PGFO strategy by drilling the Chromaska chromite target with its own money. Chromaska died quietly, and it looked like Azimut was a DW bust on two fronts. But in early 2019 when Midland's Mythril copper discovery ignited hopes for a base metals area play in the James Bay region Azimut's Pikwa project to the west became a DW focus after Azimut was able to swing a deal with SOQUEM to earn back a 50% interest. Mythril fizzled in H2 of 2019 when it became apparent that the very high grade copper mineralization was restricted to thin margins of dykes that weren't spaced closely enough to deliver a bulk mineable resource similar to that of the Aitik copper mine in Sweden. During 2019 Azimut focused on mapping and sampling the 20 km Copperfield Trend which projects SWW from the 10 km trend on Midland's Mythril project and established that there were major copper anomalies in the western and eastern ends of the anomaly. The middle seemed to be a dead zone though it did contain 2 prominent EM conductors, the only such anomalies within this trend. The geochemical dead zone may be due to the presence of a giant esker of glacially transported debris that obscures the bedrock. An IP survey in the East Copperfield portion yielded chargeability highs similar to those on the Mythril property to the east, which raised the question of whether Pikwa hosted more of the same marginal copper mineralization. Azimut decided to extend the IP survey west to include the EM conductors, because these could be part of a "center of gravity" for the mineralizing system where bigger zones may have evolved in this Archean setting. We are still awaiting the outcome of this IP survey and what Azimut plans next for Pikwa. Since December 2019, however, the DW focus has been on the Elmer project in the James Bay region where Azimut has demonstrated that the small 200 m by 80 m Patwon outcrop hosts 3 sets of mineralized gold veins: a set of short NW oriented Riedel type dilational veins, a set of sub-horizontal veins, and a set of NE-SW oriented veins, all occurring within what appears to be a 7 km NE trending shear structure. The high grades within the Patwon zone attracted market attention in January 2020 and Elmer was shaping up as a Discovery Watch success story. The association of pyrite with the gold prompted Azimut to conduct an IP survey which generated multiple chargeability highs of the sort associated with sulphide mineralization. Drilling resumed in late May 2020 with the first update occurring in late June after 29 new holes were drilled. Although the market initially responded positively, driving the stock as high as $3.50, the cautious wording by Azimut and the shifts in the drill location sequences of the two rigs suggested that expansion drilling was not playing out as expected. On July 27 Azimut disclosed results for holes close to Patwon which extended the strike 350 m and confirmed mineralization persists to a depth of 200 m. But it is disrupted to the SW and in the NE direction where holes not discussed are pending and where the IP chargeability anomaly is low rather than high. In fact, early holes drilled in ELM-1 where the IP anomaly is strong were not prioritized for assaying. During July Azimut drilled only 7 more holes, most of them in the other ELM IP anomalies. 18 holes were still being logged and assays are unlikely before September. The DW premise was that the Patwon zone would repeat itself along the 7 km shear, most of which is covered by swamp or overburden, with IP anomalies highlighting targets. It now looks like IP is not highlighting gold zones, so until we learn more about the geology and gold controls, the Elmer play is focused on definition drilling of the Patwon zone for a possible open pit scenario and chasing this style of mineralization deeper for an underground scenario. Elmer qualifies as a discovery, but for now it is not a game changing development for the gold potential of the James Bay region. (Jul 29, 2020)

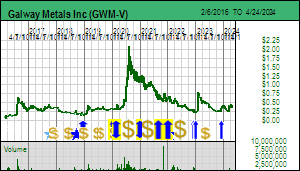

Galway Metals Inc was introduced to Discovery Watch in February 2020 based on its effort to demonstrate that the Clarence Stream gold project in New Brunswick is a multi-million ounce gold district with both open-pittable and high grade underground mining potential. It was a grassroots discovery in 1999 by Mac Watson's Freewest which along with successors never went much beyond the North and South zones for which a resource of 432,000 tonnes of 6.56 g/t gold was generated (about 100,000 ounces). Galway acquired Clarence Stream in 2016 and for the past 3 years has struggled to gain market respect for Mike Sutton's idea that it hosts a district of multiple intrusion related gold systems on both sides of the regional George Sawyer Fault which separates two ages of meta-sediments that have been intruded by younger granites which created the structural setting for gold deposition within veins along their flanks. Key to the optimism are widespread gold in till and soil anomalies north and south of the fault (the North and South zones are on opposite sides of the fault). In late 2017 Galway discovered the trend 7 km southwest of the original North-South Zones defined by the sequence of the George Murphy, Richard and Jublilee zones within a 4 km trend. Due to the complex nature of the vein sets the market has had a tough time connecting drill hole dots to visualize emerging ounce footprints, which was not helped by tight budgets during the past few years. But in 2020 a rising gold price prompted Galway to adopt a more aggressive strategy which now involves 5 drill rigs, 3 of them infill stitching together the Jubilee-Richard-GM segment with infill drilling which will become the basis for a resource estimate in Q1 of 2021, and 2 rigs "wildcatting" at the northern and southern limits of the infill focus. The open-endedness of this district play whose destiny Galway was controlling through geology smarts and drilling appealed to the market against the backdrop of a rising gold price, enabling Galway to raise $17 million in June 2020 at $0.44-$0.64 for common and flow-thru which boosted its treasury to $22 million, more than enough to carry its strategy well into 2021. On June 24 Galway reported 0.5 m of 186.5 g/t gold (6 opt) for hole #38 at the southern end where there seems to be a cross structure associated with a high gold in soil anomaly. On July 29 Galway reported that hole #65 drilled as an expansion hole to the NE of the George Murphy Zone unexpectedly intersected repeated visible gold over 14 m d=near the bottom of the hole. When you look at the geological context, #65 appears to have intersected a new zone parallel to the Jubilee-George Murphy trend which itself flanks the southeastern margin of a granite intrusive which is 400-500 m wide where it outcrops and about 2,000 m long. No holes have been drilled on the northern flank. So for the moment the market is wondering if hole 65's VG interval is evidence of a mirror trend on the other side of the granite intrusive. Although Galway describes its 2 rigs as "wildcatting", this is not the same as testing isolated targets elsewhere on the property, if which there are plenty with geochemical support. These wildcat rigs are groping beyond the known mineralization, which makes it unlikely that Galway will pull a job dropping discovery hole signaling a major new zone. That suits the current market fine, because despite the awakening bull, it remains fearful that all will soon enough end, so a district play undergoing a major rethink that incrementally keeps getting better suits the market just fine. (Jul 29, 2020)

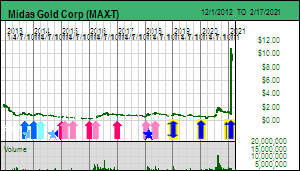

Midas Gold Corp has been a regular Discovery Watch feature since January 2017, not because there was any new mineralization to be discovered at the Stibnite gold-antimony project in Idaho, but rather because we were curious to discover if CEO Stephen Quin with John Paulson's financial backing in early 2016 could overcome the market's glum view that Idaho would never permit an open pit mine in an area that was turned into an environmental disaster zone by mining for antimony to support the World War II effort, and later by gold miners who were no longer around when Nixon invented the EPA in the 1970's to put an end to cost dumping by proponents of unfettered free market capitalists whose bible was "fuck the losers" Ayn Rand rather than "we are all in this together" Adam Smith. And boy oh boy, has it ever been a journey of discovery with regard to regulatory incompetence led by the Forest Service as the timeline for a draft Environmental Impact Statement kept slipping into the future like that Steve Miller song. Midas as of the end of 2019 has spent USD $53 million on permitting out of $210 million overall, and CEO Stephen Quin has suggested to me the total will be $70 million when a mining permit is finally granted. The last economic study was a PFS in December 2014 which was lousier than the 2012 PEA because certain parts of the deposits lacked the drill density needed to support a PFS calibre ore schedule, so half the antimony output disappeared, as did a good part of the high grade front loading of the ore mining schedule. The outcome of the PFS was not impressive because it used a $1,350 gold price as a base case to support an after tax NPV of US $832 million and 23.4% IRR using a 5% discount rate. The IRR was fine, but the NPV not so good because CapEX was $970 million thanks to a pressure oxidation unit needed to deal with the refractory sulphide ore. But even worse, gold was below $1,300 most of the time until mid 2019 when it finally began to rise as the world became uncertain about America's leadership role in a world where China under emperor for life Xi Jinping had since 2012 embarked on a course that clearly dashed any hope that China's prosperity would eventually make it "just like us", even as the US under its own leadership was setting America on a path to become just like "them". One reason the timeline for a draft EIS kept being extended was that the Forest Service simply lacked the processing infrastructure to permit a mine that would produce 350,000 ounces gold annually, turning this into a learning how to properly approve a mine on the fly experience. The other reason was that Trump's deregulatory zeal was undermined by strategic incompetence that inflicted an unnecessary government shutdown and which later enabled the Wuhan Virus to become the self-gutting America Virus. But it finally looks like a draft EIS is on track to be accepted in August 2020, which will be followed by a 45 day comment period during which objectors opposed to mining will try to demonstrate that the Forest Service and related agencies are too incompetent or corrupted to have done their job properly. Knowing the quality of the Midas team and the sincerity of the regulators to do the job properly to support a reclamation project bankrolled by a gold mine, these comments should not prove more than fodder for late night comedy, enabling Midas to publish a feasibility study in Q4 of 2020 which incorporates the cost of all the changes generated by the permitting process. A record of decision is expected in late 2021, namely a permit to proceed with construction of the Stibnite Mine whose antimony by-product will bail America out of a serious security of supply problem should the escalating "new cold war" with China disrupt the supply of raw materials in which China dominates. At $1,900 plus gold Stibnite will be very much in the money, even if CapEx expands 30%, and if you dare to dream $3,000 gold, you are looking at a $10-$15 future price target. (Jul 29, 2020)

Disclosure: JK does not own any of the companies mentioned; Azimut and Galway are Fair Spec Value rated Favorites, Midas is a Good Spec Value rated Favorite

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered as Bottom-Fish and Spec Value Hunter picks and will include projects that may be of interest only because they are in the limelight. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. KRO will keep track of projects mentioned through Discovery Watch with HoweStreet.com. Discovery Watch is available via YouTube or Podcast.

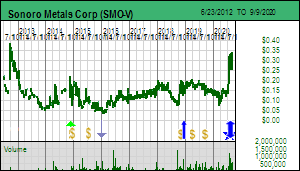

Sonoro Resources Corp was assigned a Bottom-Fish Spec Value rating on December 14, 2018 based on the company's plan to advance the 100% optioned Cerro Caliche gold-silver project in Mexico as an open-pit, heap leach operation that would start at a small scale with the dual purpose of demonstrating the recovery model and generating sufficient cash flow to fund future expansion of a much larger scale operation. Tracker April 11, 2019 describes the recent history of Sonoro, in particular the role of John Darch who emerged in late 2018 after a decade long sabbatical from the resource sector to take on the funding and marketing role at Sonoro after Gary Freeman unexpectedly passed away in early 2018. Sonoro was introduced to Discovery Watch in May 2019 based on management's rather unique plan to attract a Chinese "engineering, procurement and construction" (EPC) entity to fund and build a small open pit heap leach mine focused on a maximum 200,000 ounce resource. If this "pilot" operation was successful, Sonoro and the EPC would negotiate a deal for an expanded operation that tackles ten or so zones which have a tonnage footprint approaching 100 million tonnes, which, if definition drilling confirms the expected 0.4-0.6 g/t gold range with a 3-4 g/t silver kicker, would represent a 1.5-2.0 million ounce gold resource. In May 2019 gold was still below $1,300, so the Cerro Caliche plan clearly was an optionality bet on higher gold prices which hoped to minimize dilultion while demonstrating the mining plan plan with the help of the EPC. Gold began an uptrend in H2 of 2019 that remains intact today, so the original plan to mine 0.5 g/t ore is no longer an optionality story at $1,800 plus gold. But the arrival of Covid-19 in Q1 of 2020 sabotaged the ability of the Chinese EPC staff to travel to complete their due diligence of this project in Mexico's Sonora state. This created an existential crisis for Sonoro which needed to make staged property payments to keep title intact, which was accomplished by selling a royalty in another property and insiders loaning money to the company while allowing payables to accrue, resulting in an ugly balance sheet of a $1.3 million working capital deficit. To make matters worse, while the Chinese remained stranded offshore, Bay Street continued to sneer at a 0.5 g/t open pit heap leaching plan in Mexico. Management, noting that Bay Street was attracted to discovery exploration plays involving the rethink of existing gold systems, undertook a geological review of Cerro Caliche which included alteration studies of the ten or so zones that had been indentified within 200 metres of the surface. These zones consist of veinlets which individually can have high grades but when averaged deliver 0.4-0.6 g/t. The review led by Mel Herdrick concluded that most of the drilling of this low sulphidation epithermal system took place above the boiling zone where the veins tend to coalesce and bonanza gold-silver grades develop. The team also took heart from the Mercedes system 10 km to the southeast which was generated by the same intrusive center, which started as a low grade open pit operation, and which Prmier Gold was now mining underground for much higher grade ore. In late June 2020 Sonoro started marketing the idea of a USD $2 million financing for a 20 hole core program designed to test all the zones at a 150-350 m depth for bonanza grades, clean up the trade payables, and create a reserve for the next round of property payments in Q1 of 2021. Sonoro thus transformed itself from a low grade gold optionality play nobody but the Chinese wanted which would benefit from higher gold prices, into a dual play with bluesky high grade discovery potential that tapped into the dynamic driving the awakening resource junior bull market. Securing that financing will be critical to Sonoro's success potential. (Jul 22, 2020)

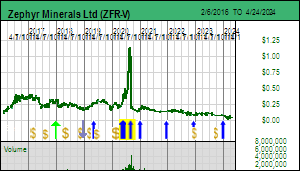

Zephyr Minerals Ltd has been a KRO Bottom-Fish Spec Value rated company since late 2017 based on the Dawson-Green Mountain gold project in Colorado where the junior has a small 111,300 oz resource for which a PEA supporting a small 300 tpd underground mine was published in early 2017. This resource in the Dawson segment has been outlined only to a depth of 275 m because it dips into a mountain and it is not practical to drill deeper. The idea is that if a small scale mine were developed a much bigger resource could be delineated by drilling from underground. The upside for the Dawson segment thus hinges on a gold bull market to bring in the required CapEx. In 2018 Zephyr acquired the Green Mtn segment to the west where it hopes to establish a similar system. Zephyr was introduced to DW in May 2019 on the basis of a Broken Hill type zinc-lead-silver target that emerged in 2018 within the El Plomo segment, a down-dropped block between the Green Mtn and Dawson segments. It features a high grade Zn-Pb-Ag horizon that was tested to a shallow depth decades ago but given up on because although it strikes for 3 km it is narrow. In the Broken Hill model metamorphism will have folded and remobilized such a system to create structural thickening and higher grades. Regional geochemistry suggests such a process could have taken place, so during the summer of 2019 Zephyr conducted an airborne Mag-EM survey over the property to see if there is a magnetic anomaly associated with the El Plomo trend that supports the hypothesis that a much thicker Broken Hill type deposit exists at depth. In September 2019 Zephyr revealed that there is such a magnetic anomaly worth drilling from 4-5 locations along the trend.An analog which fits the target's tonnage footprint is the Cannington deposit in Australia, a smaller but richer version of the original Broken Hill deposit. A KRO Cannington Clone Outcome Visualization indicated such a deposit would be worth more than CAD $7 billion at current metal prices, which, if Zephyr could avoid dilution beyond its current 74 million fully diluted, implied an ultimate price target of $100. Further support for the BHT model emerged when an electronprobe study revealed that silver occurs within a rare mineral uniquely associated with BHT deposit. Testing this target, however, is not simple because El Plomo is bighorn sheep habitat where drilling is restricted to July 1 to Oct 31. Zephyr's plans to drill during the 2020 summer were nearly disrupted when an anti mining NGO appealed the drill permit. The appeal was heasrd on July 22 and unanimously dismissed. Drilling is now expected to begin in the second week of August. Due to the visually obvious massive sulphide nature of a BHT system a new discovery could become evident early in the drill program, launching the stock into S-Curve speculation territory. If a discovery were to demonstrate Cannington scale and similarity, it would have a profound effect on the resource junior bull market awakening after a decade long drought. (Jul 22, 2020)

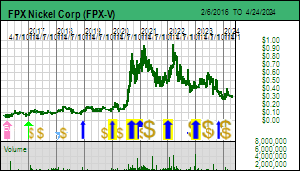

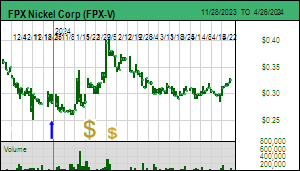

FPX Nickel Corp has had a Bottom-Fish Spec Value rating since 2017 while the junior worked on over-coming the limitations embedded in the PEA Cliffs delivered in March 2013 for a 114,000 tpd open-pit nickel mine at Decar which required a $9/lb plus nickel price to be viable. Most of this work has been completed and 2020 promises to be a relaunch of the Decar nickel story with an updated PEA expected in September 2020. FPX was introduced to Discovery watch in November 2016 as a different type of discovery in the sense that the Decar deposit, recognized in 2009, is unusual in having a very low 0.12% nickel grade as defined by a Davis Tube assay which only measures nickel recoverable through crushing and magnetic separation. This is different from a fire assay which will yield a similar grade for almost every ultramafic body that is economically worthless because it reflects nickel trapped in an olivine lattice. The Decar nickel is different because it occurs as awaruite, a nickel-iron alloy that is in effect natural stainless steel. The result is a very homogenous 1 billion tonne deposit that can be large scale open pit mined for 40 years without any sulphide related acid drainage and which, thanks to the magnesium content that ends in the tailings, could operate as a carbon sink which could bring Decar close to the holy grail of a carbon neutral mine. The key changes achieved by FPX management headed by Peter Bradshaw and Martin Turenne since buying back 100% ownership from Cliffs in 2015 are 1) replacing gravity separation with a flotation stage that generates a concentrate with 65% nickel that can be fed directly into stainless steel mills, delineation of the SE Baptiste zone that allows front-loading the ore schedule with higher grade ore, and preliminary studies that indicate that the concentrate can be converted directly into nickel sulphate, the form required by the EV battery market. FPX is unusual in that it has been funded by insiders and close associates through private placements that did not include warrants, a sign of strong internal belief that Decar is a winner. A key question the PEA will answer is the cost structure of Decar using the new flowsheet, which will make it easier to assess the potential economic value of developing Decar, expected to have a CapEx of $2 billion or more. The wild card is the future price of nickel which during the past decade has suffered from a glut of low grade laterite ore mined in Indonesia and the Phillipines and shipped as whole rock to Chinise blast furnaces where it is converted into nickel-pig-iron, a feedstock for lower quality stainless steel that meets China's standards. Indonesia no longer allows direct shipping of ore, and the Philippines is rapidly depleting the laterite resources suitable for this NPI market. The FPX PEA will show what nickel price is needed to achieve an NPV at least 50% of CapEx. Given that it will take another $40-$50 million to push Decar through feasibility to a permitted production decision, the speculative question is who might pay what percentage of the NPV at what stage for the privilege of investing another $2 billion to develop Decar as a 40 year mine in a secure jurisdiction that threatens little variation during the life of the mine. A decade ago the FPX team scoured the world in search of similar deposits, but concluded that Decar is pretty much unique. (Jul 22, 2020)

Disclosure: JK owns FPX Nickel; FPX Nickel is a Bottom-Fish Spec Value rated Favorite, Zephyr is a Good Spec Value rated Favorite; Sonoro is Bottom-Fish Spec Value rated

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered as Bottom-Fish and Spec Value Hunter picks and will include projects that may be of interest only because they are in the limelight. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. KRO will keep track of projects mentioned through Discovery Watch with HoweStreet.com. Discovery Watch is available via YouTube or Podcast.

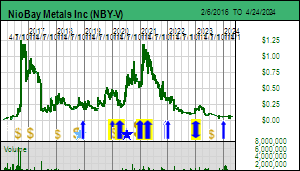

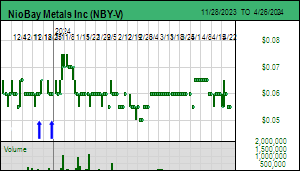

NioBay Metals Inc was introduced to DW in February 2019 after the junior was granted a drill permit for the James Bay niobium deposit in northern Ontario near the First Nations town of Moosonee. This didn't solve the problem that the tribal council chief was opposed to mining in principle and refused to consult with NioBay as required, and, when the Ontario ministry granted the permit anyway, filed for a judicial review of the decision claiming that NioBay never consulted with the Moose Cree FN. That pissed off the other MCFN tribal council members who resigned and forced an election in July 2019 rather than as scheduled in 2020. The anti-mining chief was not re-elected and most of her anti-mining allies on the council were replaced by members prepared to listen NioBay. That process finally led to a "protection agreement" which plugged the MCFN into NioBay's exploration plans and gave them comfort that this was not going to wreck their backyard. It allowed NioBay to conduct a drill program in Q1 of 2020 which it got done before Covid-19 shut down everything. The drilling deepened and extended the footprint of the carbonatite which led to an updated resource estimate in early July 2020 that boosted the indicated+inferred resource 19% to 63.5 million tonnes at a grade of 0.52-0.53% N2O5. That, however, is not so important because the critical milestone is a PEA which describes a plausible mining scenario and what its economic value might be. The niobium market is dominated by supply from Araxa in Brazil which is five times richer and five times bigger than James Bay. Niobium is a $3 billion market controlled 85% by the CBMM family which has set the niobium price at a level which allows 2 other mines to be viable, one in Brazil owned by ChinaMoly and Niobec in Quebec owned by Magris. Niobium demand has being growing at a CAGR of 6.5%, though this will be lower during the pandemic. But James Bay wouldn't be in production until 2025 or beyond. The deposit was discovered during the 1960's and taken to feasibility by Bechtel, but never developed because of its remote location. NioBay's goal is to make it the world's fourth major primary source of niobium and to do that James Bay needs to be viable at the price set by CBMM. NioBay is working on a PEA it hopes to have out before October 2020. It will present an underground only as well as open-pit/underground hybrid scenarios with a 6,000 tpd processing facility. The market has a hard time quantifying the size of a niobium prize, so I have created a SC 6,000 tpd UG scenario OV within the ShareCollective using a resource of 40 million tonnes at 0.53% N2O5 and the spot ferroniobium price. Its after tax NPV outcome is USD $576 million which translates into a potential future stock price of $13.19 if there is no further dilution. That is quite an impressive target even when you assume 100% dilution to drive James Bay through feasibility. The 43-101 PEA will thus be a critical milestone for the market's perception of the upside for NioBay, and it will also become the basis on which the MCFN will have to decide on what terms, if any, they support a major niobium mine in their backyard. (Jul 15, 2020)

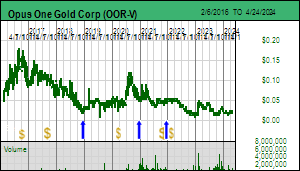

Opus One Resources Inc was introduced to DW in March 2017 as a proxy for a potential area play surrounding Osisko Mining's rethink of the Windfall gold project in the Urban-Barry area of Quebec. Although a greenstone belt this area unlike the Abitibi was not know for robust orogenic gold systems. Windfall was as an erratic gold system which yielded high grades but the zones did not hang together well. The Osisko team felt that Windfall was in fact a mis-understood Timmins style system, and undertook a massive drilling campaign which figured out the plunge of the vein systems, chased them deep, and eventually delivered a 6 million oz plus resource. Osisko started this during a bear market and there was a flurry of activity in adjoining juniors, but that didn't answer the question of whether Osisko had turned Windfall into something new and important on a regional scale rather than a local scale. Osisko had staked land to the east, surrounding the Fecteau project which Opus had optioned because of its apparent VMS potential. Opus itself was created to host a group of properties optioned from Adventure Gold before Probe Metals absorbed Adventure to get at the Val D'Or East project. The lack of visible skin in the game by the board of Opus was because they were custodians for hidden Quebec players. I turned Opus into a canary that served as a local proxy for the Windfall area play and a broader proxy for the Quebec resoruce sector. Opus One went from a tweety bird to near dead canary when Windfall failed to excite beyond Osisko and results of work done at Fecteau failed to excite the hidden shareholders. In early 2019 Opus optioned the Noyell project on the Casa Berardi Break east of the old Vezza Mine where Opus owned the Vezza North and Extension properties. Opus One's geologist Pierre O'Dowd was behind this project; a decade ago he had worked on it for a junior that used it as stepping stone for something "better" in Africa, and pulled the plug on the exploration strategy. Opus resumed that strategy in March 2020 with a 10 hole drill program but only got 2 holes done before Quebec pulled the plug on exploration due to Covid-19. This was a big disappointment because the Noyell target can only be drilled in winter when the swamp is frozen. When the holes were reported in early July and showed that the iron formation system was robust at depth and continued to the east if the IP survey is to be trusted, this near dead canary dragged itself off the cage bottom. Fecteau will only get some till sampling this summer, and even if it gets a couple holes to spend the flow-thru money, it would be very lucky to tag into a VMS zone right away. So this stock's market action will be about the resumption of drilling in January 2021 at Noyell, and thus it is now serving as a proxy for the awakening of a resource junior bull market. (Jul 15, 2020)

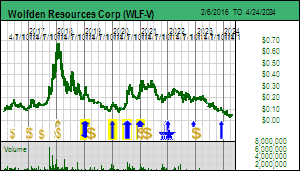

Wolfden Resources Corp was introduced to DW in August 2018 based on the intriguing story of Maine reforming its mining code and re-opening itsef to exploration after more than a decade of no trespassing signs. Wolfden was a first mover to do a deal on the Pickett Mtn VMS system which Getty found and explored during the 1980's. Since then we have been watching to see if Wolfden can expand the existing resource. This was accomplished with the January 2019 resource estimate for the West-East lenses after drilling pushed the West Lens deeper. 2019 was supposed to be the year Wolfden discovered new lenses in the Footwall Zone and in fold limbs parallel to the West-East lens limb. But technical drilling problems turned the campaign into a bust except for a teaser stringer zone in which the last hole was lost. But during 2019 Wolfden flew geophysical surveys, not just on the property, but also on a 30 km by 10 km grid covering geology similar to that which hosts the Bathurst Camp in New Brunswick and Buchans in Newfoundland. To avoid equity dilution Wolfden raised USD $3.5 million January 2020 by selling timber rights. It also filed for land use rezoning from logging to industrial for a 500 acre parcel that would be the site for mining infrastructure. This rezoning is necesaary for a mining permit application and they hope to get it by Q1 of 2021. In early Q3 2020 Wolfden will publish a PEA for a 1,000 tpd UG mine which was the basis for the rezoning application. I created a SC 1,000 tpd scenario OV in the ShareCollective which yields a USD $135 million after-tax NPV that implies a future CAD $1.24 stock price, but that is a worst case scenario. Much more interesting is the exploration potential to boost the existing resource to 10 million tonnes at the same grade so as to support a 2,000 tpd scenario with a 10 year mine life. The SC 2,000 tpd scenario is much more interesting at USD $464 million NPV with a corresponding CAD $4.26 stock price. Wolfden began a 5,000 m drill program in July 2020 designed to test multiple new targets at Pickett Mtn whose EM conductors represent potential tonnage footprints of 15-20 million tonnes. The DW hope is that Wolfen turns one or more of these targets into satellite massive sulphide zones that boost the resource towards 10 million tonnes. Failing that, Wolfden is negotiating with landowners for deals on some of the sourrounding area it flew in 2019. If successful, the play turns into a regional quest for Buchans scale VMS clusters. (Jul 15, 2020)

Disclosure: JK owns NioBay, Opus One, Wolfden; NioBay and Wolfden are Good Spec Value rated Favorites; Opus is Bottom-Fish Spec Value rated

Effective January 1, 2019 we have new Membership Fees and an expanded Spec Value Rating System. Check out the catalog of Free Stuff at KRO. Currently we have a USD $275 special membership option which gives full access to KRO to end of 2020.

This Week in Money is a weekly show hosted by Jim Goddard and sponsored by HoweStreet.com which features a wide range of commentators. The July 11, 2020 show is available via Podcast or YouTube. It starts at 11:31 and runs about 40 minutes.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered as Bottom-Fish and Spec Value Hunter picks and will include projects that may be of interest only because they are in the limelight. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. KRO will keep track of projects mentioned through Discovery Watch with HoweStreet.com. Discovery Watch is available via YouTube or Podcast.

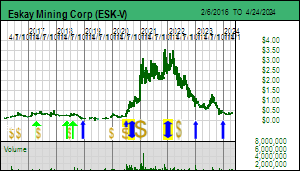

Disclosure: JK owns none of the companies; Azimut and Galway are Fair Spec Value rated Favorites, Eskay Mining is a Bottom-Fish Spec Value rated Favorite