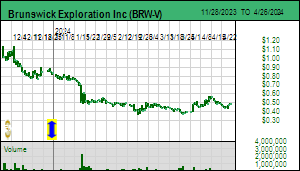

Brunswick Exploration Inc captured the market's imagination during the prior week on news that boots on the ground had identified a 2.7 km trend of outcropping pegmatites up ice from a 1.7 km long by 200 m wide boulder train announced in June which itself has now been extended to 3 km down ice. Key to the excitement is that these outcrops have a similar impressive distribution of spodumene mineralization as the down ice boulders, supporting the conclusion that the source of the boulder train is within the Mirage property. Whether this is a series of short en echelon pegmatites perpendicular to the geological trend as is the case with Allkem's world class Galaxy-Cyr deposit, or a series of parallel elongated pegmatites such as PMET has with the world class CV5 deposit on its Corvette property, is not yet known. Brunswick is mobilizing a scout drilling program to sort out the geometry of these dykes and set the stage for a major discovery delineation program in Q1 of 2024.

On Monday August 28, 2023, however, Brunswick dropped a big cowpie on the market with an update about what its boots on the ground accomplished in other parts of Canada while its access to James Bay was blocked by fire restrictions. A big talking point for CEO Killian Charles has been how the company's prospect generating strategy of researching assessment work archives and matching verbal descriptions of pegmatite occurrences with commercial quality satellite imagery has revealed 800 outcropping pegmatites, none of which have been seriously explored, and any one of which could be the tip of a world class LCT-type pegmatite iceberg. Well, the boots on the ground armed with an XRF gun could not confirm any of these pegmatites as LCT type located in Saskatchewan and Manitoba. In cases where the assessment work archives claimed to have observed spodumene there was no such mineralization present. Those pegmatites which registered beryllium and which might have rare earth or uranium potential are not what Brunswick is looking for. At best they are indications of a setting that spawned pegmatites from a granitoid intrusion, but one has to look farther off-board to find the LCT type that can become a future lithium mine. None of the targets in Saskatchewan or Manitoba delivered any joy, and where Brunswick had optioned claims from juniors like Eagle Plains and Searchlight, the absence of any obvious low hanging fruit has prompted Brunswick to drop those options. Yes these juniors got some pennies up front for what appear to have been worthless lithium properties all along, though closer exploration may reveal high hanging fruit, but Brunswick had a cheap crack at harvesting low hanging fruit and came up empty. The outcome is not a cause for celebration by either side.

The market did not like this news because it underlined the suspicion that historical documentation of a pegmatite, confirmed by satellite imagery, is not likely to be good enough. Yes, when you start with 800 such targets, the process of elimination should leave you with a few world class candidates. But when Brunswick declared that it was giving up on Saskatchewan and Manitoba, suspending its boots on the ground investigation of its Ontario targets, and allocating all its resources to its prospects in Quebec's James Bay region, that was a body blow to the idea that much of Canada has meaningful lithium potential. The market reacted negatively because the next question is, how do we know that your boots won't also crush all your other James Bay pegmatite outcrops?

But maybe Brunswick's exodus from these provinces is not really a thumbs down for mineral potential. The elephant in the room is the threat to critical mineral supply development posed by Canada's First Nations who Prime Minister Justin Trudeau has put on steroids with his embrace of UNDRIP, the United Nations Declaration of the Rights of Indigenous People. Take the time to read the July 13, 2023 CBC article First Nations won't be excluded from critical minerals 'gold rush,' say leaders to understand how Trudeau has sabotaged Canada's mineral supply potential. From past experiences like Alto's Oxford project in Manitoba which Ontario lawyer Kate Kempton torpedoed when she parachuted into town with stories about the need for archeological studies, and Fjordland's futile effort to get a drill permit for a nickel project optioned from Canalaska, I already know that Manitoba's First Nations are a major exploration obstacle for resource juniors. The CBC article tells you that a Saskatchewan pegmatite lithium boom will be still born, though the thrust seems to be more about capturing whatever DLE can extract from oilfield brines.

Some parts of Ontario have First Nations groups eager to participate in the mineral sector on simple commercial terms based on the fact that this is happening in their backyard and they have a strategic advantage. Others such as the First Nations in northern Ontario are split between supporting mineral development and pretending they are still engaged in traditional activities. Check out Stan Sudol's articles from last December describing the Ring of Fire situation: Northern Ontarios Ring of Fire can save provinces auto sector and Ontario has moral obligation to develop Ring of Fire. Brunswick makes no suggestion that the First Nations obstacle course was a factor in its decision to focus on Quebec. And Quebec is no cakewalk as far as First Nations are concerned (moose and goose slaughter seasons are necessary why?), though a difference between the Cree in Quebec and those in Ontario is that the Quebec Cree have figured out how to collaborate with commercial developments in their backyard. That doesn't mean Quebec will not also collapse into a showdown between a DNA defined aristocracy representing 5% of Canada's population and the 95% without indigenous DNA about who gets to shape Canada's supply of minerals critical for the energy transition. It just means that the starting point will be a win-win rather than winner-take-all outcome.

Brunswick has decided to concentrate on the James Bay region of Quebec because PMET's CV5 maiden resource estimate and Allkem's Galaxy-Cyr resource update show that this is a world class lithium pegmatite district, whether the pegmatites occur as an enchelon set of dykes repeating along great distances within dilation zones of a regional structural feature, or as elongated parallel zones within these structural corridors. Currently Brunswick's James Bay strategy has three prongs: 1) optioning large land packages like Plex and Anatacau which cover greenstone belts Andre Gaumond's Virginia companies once explored for precious and base metals deposits, 2) staking claims on top of documented pegmatites corroborated by commercial satellite imagery, and, 3) serendipity deals such as Mirage which emerged because Bob Wares managed to remember that a long time ago Remi Charbonneau pitched him and others on these spodumene boulders in the middle of nowhere north of the Renard diamond discovery at a time when global supply of lithium was worth $200 million and dominated by Australia's Greenbushes pegmatite and Chile's salar brines.

The first strategy is similar to what Q2 Metals and Ophir Gold have undertaken with their Mia and Radis claims covering the 30 km Yasinski greenstone belt. But Q2 and Ophir already have confirmed high grade LCT-type pegmatite outcrop and will both be drilling by Q1 of 2024. Brunswick is only now getting boots on the ground at Plex and the Mythril property north of PMET's Corvette property optioned from Midland. Mirage is more a function of madness than method, though if it is another CV5, no Brunswick shareholder will complain. Again, it is important to keep in mind that Rio Tinto says the world will need 60 Jadars by 2035, and CV5 is only one Jadar.

The wild card for Brunswick is the second category of projects, namely properties it staked 100% using the same method as it applied to properties in Saskatchewan, Manitoba and Ontario. The Monday news included a description of what the Hearst outcrop proved to be all about after a 2,000 m winter drill program. Its small surface expression was the opposite of the tip of an iceberg because it was an upside down iceberg that pinched out at depth and had nothing along strike. Plus the lithium content was marginal and not spodumene. The only part of Ontario that seems to have world class lithium pegmatite potential is the northwestern part where Frontier Lithium has its Pak/Sparks deposit. But this area faces challenges in the form of remoteness and remote First Nations communities who prefer things to remain remote. But the James Bay region is different and the best way to frame this is to contrast the greenstone belts of the Abitibi region with those of James Bay. The deep seated structures within the Abitibi greenstone belt have yielded a 100 million ounce gold bounty. In contrast the greenstone belts of James Bay have yielded Eleonore, Eau Claire, and Azimut's award winning pencil deposit, Patwon, for which Azimut has not dared to provide a resource estimate. Looking for gold in James Bay is like tilting at windmills. Looking for lithium in the Abitibi is almost the same. But today looking for lithium in James Bay is like looking for gold in the Abitibi a century ago. Even though Monday's Brunswick news was greeted as a downer by the market, what Bob Wares in effect declared was, forget everywhere else, if you want lithium, James Bay is the place to be!

Brunswick was made a KRO 2023 Favorite because it had assembled a broad portfolio of projects in Canada representing 800 pegmatites documented by past exploration. This was cool because it is only since 2021 that the world has recognized that the EV revolution is real, and begun to understand the lithium demand implications. Bob Wares and his team jumped onto this concept and parsed the archival universe. Hearing this past week that the pegmatites in Saskatchewan and Manitoba are all dogshit was not so cool. The implication that Brunswick's brute force process of elimination universe has shrunk to its 100% staked James Bay projects, the ex-Virginia Osisko optioned blocks, and the Mirage miracle, while cooling the market's enthusiasm for now, did spark interest in a bottom-fish junior called Dios Exploration Inc. This junior has a horrible web site, no corporate presentation, and issues strange sounding press releases; not even close to qualifying as a KRO Favorite. Nevertheless I have been encouraging paying KRO members to accumulate Dios as a bottom-fish since last September because once I saw this perennial James Bay precious and base metals explorer start acquiring lithium prospects, I took the trouble to contact CEO Marie-Jose Girard whom I have known since around 2000 when Ashton discovered the Renard diamond cluster.

Since being spun out of Sirios in 2002 so that it could focus on diamond exploration, Dios has plodded through the past couple decades as a survivor which has never done a rollback, and still has only 121.3 million shares issued. Fully diluted drops from 135.8 million to 125.7 million if 9,090,000 warrants at $0.20 expire unexercised on September 11. MJG, as we call her on the KRO Slack Forum, works closely with her long time exploration VP Harold Desbiens. During Q2 of 2022 she was focused on the K2 gold prospect next door to Azimut's Patwon gold discovery, the famous pencil deposit beloved by Agnico-Eagle and celebrated by AMEQ in 2022 as the discovery of the year. Like Azimut's Jean-Marc Lulin, she was dismissive of all this Lithium Mania 2.0 blather from the likes of John Kaiser and Bob Wares, and wasted no opportunity to pooh pooh CV5 because it was under a lake and in a remote location.

By September something or somebody had gotten to her (perhaps as she did the drill hole math she saw what was evolving at CV5?), and she began a stealth prospect generating strategy. What intrigued me was how MJG and HD were applying their deep knowledge about James Bay geology, which has nothing to do with kimberlites that come up where they do, and the glacial history which was very relevant to their quest for kimberlite clusters outside the Renard cluster controlled by Ashton. When I listened to how they were combining lake bottom sediment data published by the government with glacial transport history to vector in on geology that was permissive for the formation of LCT type pegmatites, sometimes seeing scant references to outcropping pegmatite in assessment files, and then hearing that they had a regional proprietary till sampling database which managed to capture lithium minerals despite these not qualifying as the sort of "heavy minerals" till sampling for diamond indicator minerals targets, I coined the term "second order" exploration to distinguish the Dios targets from those generated by Brunswick's "first order" exploration.

When you look at a Brunswick map showing the location of its "first order" generated claims, and compare with the slowly emerging locations of the claims Dios has staked, a startling pattern becomes apparent. All of the Dios properties are emerging within a giant hole devoid of Brunswick claims. The Dios market perked this week because some investors began to understand that there is something special going on at Dios. The Brunswick claims are all "first order" targets based on archival references to pegmatite showings confirmed by satellite imagery. These may indeed be low hanging fruit Brunswick could harvest in the remainder of the 2023 prospecting season. Brunswick as the early bird got all these worms, which is why it commands a valuation tenfold that of Dios and why KRO members own more Brunswick than Dios. But Dios as a late bird is going after fruit hanging mid-tree, harder to see and reach, but with no less potential to be world class. During the past week Dios sent boots onto the ground to start checking out these "second order" targets. The sad reality may be that when the field workers from Jody Dahrouge's geological service company hit the ground, nothing that qualifies as LCT-type grading 1%+ Li2O shows up, even where assessment files documented pegmatite. That is why Dios continues to drift as a bottom-fish, with mysterious blobs of stock periodically pounding the bids, a two person show with either no marketing skills or no time to deploy them. All that could change within a couple weeks. |