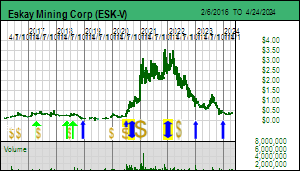

| The KRO 2022 Favorites Index is down 28.1% as of November 3, 2022, up from its October low of being down 39.4%. The only stock that is up is Verde Agritech which is up 163.6% after a good week during which it announced that the full 2.4 million tpa K Forte capacity of Plant 2 is now operational. So far it looks like Jair Bolsonaro will accept his narrow defeat but I think he is just waiting to see what happens with the American mid-terms on November 8. FPX Nickel is the next best performer down 20% at $0.40. It seems that the RBC selling has dried up, but the market remains nervous. All the rest are down 50% or more and probably are close to the bottom if not already off the bottom like FPX Nickel. The one exception that makes me nervous is Eskay Mining Corp which is a Favorite because of its potential to deliver an Eskay Creek clone discovery at its Eskay project in the Golden Triangle. The company announced on October 7, 2022 that it had completed 29,500 m of drilling that started late May in the TV-Jeff area and then moved on to the more exciting Scarlet Ridge target in the northern part of the property not that far from Eskay Creek 1 but within the east anticline of this former marine rift basin. This area has never been properly explored so it held the greatest hope for a discovery in 2022. ESK has reported sulphide visuals which support the VMS model but no assays yet for any of the holes.

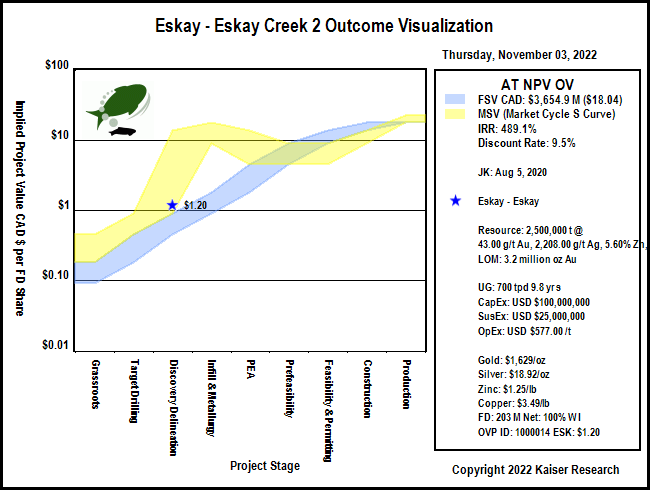

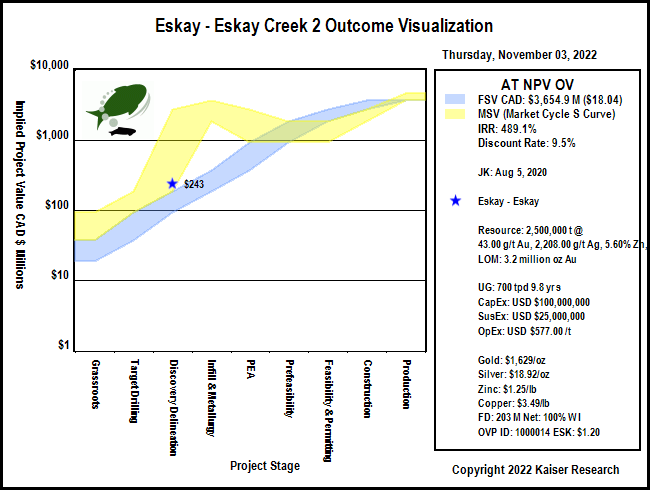

I am not expecting anything significantly new for the TV-Jeff area based on the visual descriptions published, and the market will not care about short isolated high grade silver-gold intervals. It wants to hear that enough of a zone has come into view to allow a resource estimate. If a resource estimate is not in the cards we know it is no longer a real discovery in the sense of something with mine potential. As far as I am concerned everything now hinges on what Scarlet Ridge assays. And therein lies my problem. The two IPV charts below show the fair value and S-Curve channels for an Eskay Creek equivalent outcome which would be worth CAD $3.7 billion at today's metal prices, or $18.04 per share assuming no further dilution. At a $1.20 stock price the project has an IPV of CAD $241 million based on 203 million fully diluted. That pricing represents poor speculative value in terms of the rational speculation model, but it is within the lower end of the S-Curve range for a project at the discovery delineation stage. However, given that TV-Jeff assays are still pending, one has to conclude that this target is no longer at the discovery delineation stage, and should be dropped back to target testing stage where Scarlet Ridge is currently at. Scarlet Ridge needs to replace TV-Jeff as the new discovery focus.

ESK is already down 56% from its $2.77 starting price, but if assays lead the market to conclude that Scarlet Ridge has not yet reached discovery stage, or if it has, with a much more modest outcome than Eskay Creek 1, the stock will be vulernable to another 50%-80% drop. The stock has held up remarkably well, in part because it has developed a cult style shareholder base, but even cultists are not stupid when it comes to financing. At the current price none of the warrants are in the money, including the 1.6 million at $1.30 that expire in early December. And even these won't solve ESK's working capital problem. As of August 31 it had only $5.3 million working capital, much of which will be gone by the time the final assays are paid for. There is a $2.7 million debenture due to Seabridge at the end of the year which Mac Balkam can maybe persuade Rudy Fronk to defer for another year. But if ESK is to follow up next year with a similar scale work program, it will need to finance with flow-through in December or hard dollars in Q1 of 2023. Unless Scarlet Ridge delivers spectacular results that turn it into the new Eskay Creek 2 discovery delineation play, such future financing will happen at much lower prices. Even if the faithful hold steady, the algos will tank the stock. Eskay Mining Corp poses the greatest risk for dragging the KRO 2022 Favorites Index lower. May John Dedecker's enthusiasm prove prophetic. |