| Kaiser Watch July 14, 2023: Short Attack boosts PMET Credibility |

| Jim (0:00:00): What do you think of the short attack launched against Patriot Battery Metals? |

On July 6, 2023 an outfit called Night Market Research that specializes in identifying short selling opportunities published a length report title: Patriot Battery Metals: Aggressive Vancouver Promotion with Multiple MRE Delays and Fake Buyout Rumors Running Headfirst into Wall of Risk (and Warrants). This caused the stock price to decline on July 7 and the ASX requested PMET to provide a response which the company did on Monday July 10 when it also published the final assays for the winter drill program. The ASX will allow a stock to be halted for a number of days while material news is disseminated, but the remaining assays are not material because they are all within the CV5 pegmatite body and do not really change the market's perception of the extent and grade of CV5 for which a resource estimate is anticipated in a "few weeks". The TSXV allowed the stock to trade on Monday while the ASX allowed trading to resume on July 11, enabling the Canadian market for the first time in a long time to set the tone for PMET. The stock recovered into the $15-$16 range as the market shrugged off the Night Market Research report's allegations which fall into two categories.

The first is that in fundamental terms the Corvette project is over-valued and is destined to correct downwards as the project proceeds into the feasibility demonstration stages of the 9 stage exploration-development cycle that starts with grassroots exploration and finishes with commercial production. In terms of my rational speculation model this is true, for the stock is in S-curve territory, the initial valuation surge of what is commonly called the Lassonde Curve, namely the discovery delineation stage where the sky is the limit as to how big the discovery can become until a maiden resource is delivered, after which the market sees the limits and focuses on cost discovery which forms the basis for a discounted cash flow model valuation expressed as a net present value (NPV) accompanied by an internal rate of return (IRR). (Nicholas LePan of the Visual Capitalist has done an excellent job Visualizing the Life Cycle of a Mineral Discovery.) I have observed that the peak valuation frequently matches that of what the project ends up being worth in DCF valuation model terms years later when the project is ready to go into production. The valley in between while the company engages in cost discovery after deposit discovery has been completed is called the "value trough" from the perspective of those who don't already own the stock. Whatever back of the napkin valuations are done during the transition usually shrink as flow-sheets and permitting requirements are sorted out. An additional source of outcome value shrinkage can be the future metal prices, though sometimes they end up higher, the perennial hope for gold projects.

An example of the Lassonde Curve in action is Dia Met Minerals whose Ekati diamond discovery reached a peak $2 billion valuation in 1993, two years after the initial discovery announcement. Three years after Ekati went into production in 1998 BHP acquired Dia Met and its 29% interest for cash at an implied value of $2.3 billion on a 100% basis. Why did Ekati hit a $2 billion value during the discovery stage before we had any numbers for tonnage, grade and carat value? Because this was a brand new diamondiferous kimberlite field outside of Africa where it was legitimate to dream that world class monsters like Jwaneng or Orapa in Botswana might emerge within the Slave Craton of Canada. This did not happen, but the collection of pipes selected for production did end up having a world class value.

Completely missing from the Night Market Research short attack is any discussion of the "district scale" implications of the Corvette property which covers 45 km of the La Grande Shear Structure of which the CV5 resource will represent only a portion. NMR is making the assumption that the CV5 maiden resource estimate will be the culmination of what the Corvette property has to offer, something which the Australian and Canadian brokerage analysts think will be comparable to what Liontown accomplished with Kathleen Valley, which earlier this year attracted a conditional bid from Albemarle that priced the project at about AUD $5 billion (see KW Episode Mar 29, 2023 for background on Liontown's 8 year journey from grassroots lithium exploration in 2015 to the current status of mine construction). Liontown rejected the conditional bid but the stock has since then consistently traded above the proposed Albemarle buyout price. NMR correctly points out that Liontown has pushed Kathleen Valley through 5 years of feasibility demonstration to get the current valuation, as a result of which it has 2.2 billion shares issued, but what it ignores is that Kathleen Valley is now an optimized mining scenario for that project. This project is as good as it is going to get.

PMET's situation at this stage is equivalent to owning the entire 40 km long Carlin Trend in Nevada, and CV5 is the equivalent of finding Goldstrike as the first Carlin-type gold discovery within this trend. And we know a lot more such gold deposits were subsequently found. How many more CV5 deposits might be found within the Corvette property that could be developed as standalone open-pit mines? Perhaps 3-5 more, perhaps none. The point is we don't know yet because the first order lithium discovery boom in the James Bay region is only 2 years old; all the other advanced lithium deposits (Galaxy-Cyr, Wabouchi, Moblan, Rose) were discovered decades ago and are valuable today only because of the climate change crisis and the electric vehicle as a partial solution to achieving the goal of net zero emissions by 2050. How many Kathleen Valley deposits are left for Liontown to find on its property? If there were any more would they not have been found during the past 5 years while the main pegmatite plodded through the feasibility demonstration stages? If the big producers knew that CV5 is all that will ever be found and developed within the Corvette property, there is no way they would consider paying $2-$3 billion to own PMET.

The IEA has projected that the world will need 600% more lithium supply if 2030 EV rollout goals are to be met. That is with existing lithium ion battery technology. Rio Tinto has made even more aggressive predictions. If the EV sales goals are met, the lithium market will be worth $100-$200 billion in 2030-2040 assuming current battery technology remains unchanged. During the past few weeks Toyota, which was in the vanguard with its Prius hybrid model but has been a laggard with full plug-in electric vehicles while it focused on leapfrogging lithium ion battery technology through hydrogen fuel cell technology, made the stunning announcement that it had solved the processing cost problem for a solid state electrolyte which allows lithium metal to substitute for graphite in the anode. Toyota predicts that by 2027 it will be selling a high end model that has a range of 1,200 km and a charge time of 10 minutes. Neither the IEA nor Rio Tinto forecasts allow for this greater usage of lithium in future electric vehicles.

Since you are probably not going to achieve the required lithium supply if the price of lithium crbonate tanks back below $5/lb, what we are facing is a massive scramble to find and harvest the low hanging LCT-pegmatite fruit that is suddenly in the money, and which faces a 5-10 times demand expansion. Australia has already been through this low hanging fruit cycle which I call Lithium Mania 1.0; the second phase targeting stable regions such as Brazil and Canada is Lithium Mania 2.0 for which PMET is the poster child. Rio Tinto has said the world needs 60 Jadar scale lithium mines; the James Bay region has the capacity to deliver a couple dozen Jadar equivalent mines.

The timing of this report just ahead of PMET's plan to publish a maiden resource estimate appears designed to force a stock price retreat if the resource proves lower than the lofty conceptual estimates published by various Australian and Canadian brokerage firms. I have speculated the resource will come out within the range of 50-100 million tonnes grading between 1%-2% Li2O, but Night Market Research has presented a range of estimates from 90-160 million tonnes with grades ranging 1.12%-1.35% Li2O. It offers its own prediction of 73 million tonnes of 1.28%, whose grade is near the upper range of the analyst predictions, though its tonnage is lower than the 90 million tonnes at 1.35% Li2O it attributes to National Bank. NMR claims that PMET CEO Blair Way has been encouraging the market to think in terms of at least 100 million tonnes, which has supposedly set up the market for disappointment. NMR is predicting that the CV5 resource will be similar to the 68.5 million tonnes of 1.34% Li2O proven and probable reserve Liontown is putting into production.

The reality is that we do not know what cutoff grade PMET plans to use. If it uses a higher grade cutoff the tonnage will be lower but the grade higher. Initial development could focus on the higher grade Nova zone within the CV5 deposit. NMR has in fact created a straw man to knock down the market if we see a resource closer to its number. The reason it thinks the analysts are over-estimating the resource is that PMET stopped publishing sections along with its holes last year. However, PMET has an excel spreadsheet with all the drill hole data which includes the azimuth direction and dip angle for each hole, plus all mineralized intervals greater than 2 metres. Combine that with the drill plan and an analyst can construct a 3D model, especially if they have Leapfrog software at their disposal. What the company has not published is the assay interval breakdown which would allow analysts more granularity in defining the geometry of their choice using their own cutoff grades. NMR argues that the implied project value of about CAD $2 billion on a fully diluted basis is excessive if the estimate is more in line with its own prediction, but it does not provide a quantitative basis for this view which requires one to visualize an operating mine and calculate a net present value from the resulting cash flow.

Once we have a 43-101 resource estimate the market will be in a position to create an outcome visualization in the form of a DCF model which depletes the resource within 15 years. For example, NMR's resource would be mined at about 13,000 tpd to be depleted within 15 years. The economic value of that scenario will depend on CapEx and OpEx as well as the long term price of lithium carbonate. Suppose the DCF model does generate a future target outcome of CAD $5 billion. Under my rational speculation model fair speculative value should be 2.5%-5.0% for a project that has delivered a resource estimate but not yet done cost discovery in the form of a PEA. So we are talking a fair value range of $2.50-$5.00, well below the current valuation. However, if the project moves to PFS stage the FSV should be 50%-75% of the target outcome, which would be $25-$38 per share. What NMR is arguing is that the current valuation is an S-Curve peak which will follow the Lassonde Curve downwards once the project enters feasibility demonstration stage and follows into the value trough.

This can be expected to happen if PMET stays in charge of moving the project through the feasibility demonstration stages, but a likelier outcome is that a major producer will buy out PMET and do it properly. The most obvious candidate is Rio Tinto which has been optioning nearby properties from Azimut and Midland in what amounts to an effort to tie up as much of a new district as possible. NMR seems to be trying to talk down the price of PMET in order to help a third party get a better deal. But this may not work because we are talking about an emerging world class lithium district serving a market that by 2030 will be worth $100-$200 billion, more if Rio Tinto's own predictions are to be believed, and even bigger if Toyota is not bullshitting us. CV5 represents only a fraction of an LCT-pegmatite mineralized trend. There may be multiple CV5 deposits present, each of which could be developed as a standalone mine. It is conceivable that Rio Tinto, Albemarle or Pilbara Minerals would be willing to pay an S-curve valuation based on the strategic district value. Far from making a case that PMET's stock price will be a lot lower once the maiden resource estimate is published, Nigh Market Research has in fact boosted the credibility of PMET's discovery.

NMR's other angle of attack is to slag the history of Patriot Battery Metals, such as the sordid 18 month marketing deal PMET did at USD $500,000 per 6 month term with some obscure entity based in an ordinary Vancouver residential neighborhood. This deal was made just before the company announced an RTO of a private rare earth company that was canceled a couple months later when Blair Way became CEO and steered PMET back to the Corvette lithium project. I abhor these awful and expensive marketing deals Canadian juniors do to pump their stock, and sometimes I wonder if these deals are just ways for hidden insiders to steal their private placement money back into their pockets. In the ASX requested response to the short attack Blair Way stated the marketing deal was terminated after 6 months when PMET had a market capitalization of only $20 million, a hundredth of what it is today. Regardless how sleazy the marketing deals a junior may have done, none of that matters if the company has delivered a fundamental success. One thing I keep repeating is that the nature of Lithium Mania 2.0 is such that even juniors with horrible management practices can achieve a huge fundamental success, provided they spend money on competent exploration. Whatever questionable marketing deals PMET management has done, it did let Darren Smith's competent exploration team do their stuff.

NMR also tries to scare PMET shareholders by pointing out that Ken Brinsden, who played a key role in the success of Pilbara Minerals during Lithium Mania 1.0, was previously involved with an iron company that failed. Who cares? That is like arguing that Robert Friedland's Mongolian Turquoise Hills copper-gold discovery in Ivanhoe One, after he delivered a $4 billion buyout for the Voisey's Bay nickel-copper discovery by Diamond Fields, is doomed to fail because Friedland's earlier company, Galactic, crashed and burned. Not every Friedland effort is a winner (Kaizen and Cordoba come to mind), but Ivanhoe Two's Kamoa-Kakula grassroots copper discovery in the DRC is a monumental fundamental success. This complaint is the most feeble one NMR makes.

NMR does make a valid point when it frets that PMET has a large overhang of unexercised warrants that are very much in the money. Many of the holders will already have dumped the long positions from those private placements done in 2021 and are sitting on huge paper profits. Frankly I do not understand why so many cheap warrants remain unexercised. I pointed out this problem in KW Episode March 17, 2023 and it is still a problem. NMR's main strategy is to prime the market for a sell-off after the maiden resource estimate is released by predicting it will be lower than analysts are projecting. During the past year there have been several rumors about possible takeover bids for PMET, none of which are credible because no producer is going to pay a "strategic" premium without at least a resource estimate in view to explain its reasoning. The market risk is that even if the resource estimate come in within the analyst predicted range, there may not be a quick follow through. The attitude of the warrant holders is that they will exercise when they have to, such as in the event of a takeover bid. But if that does not promptly happen because Pilbara, Mineral Resources, Albemarle and Rio Tinto are all disciplined and reluctant to start a bidding war, the stock could stall. At Friday's $15.70 closing price the 24,330,190 warrants that expire between December 21, 2023 to March 21, 2025 have an implicit profit of $365 million, which to collect would require $382 million worth of buying at $15.70. Psychologically this type of warrant based paper profit is more unstable than if the holders exercised them a long time ago without selling any. NMR is in effect reminding all the warrant holders of their prisoner's dilemma situation and setting up a selling cascade after the resource estimate is released. The potential bidders for PMET are right now chortling with glee at the predicament of the warrant holders.

NMR also worries about the permitting regime in Quebec which is fairly detailed and could benefit from streamlining. It also mentions a lake sturgeon that supposedly lives in the lake which would be disrupted by open-pit mining CV5. The Canadian and Quebec governments are going to have to do a cost-benefit analysis. Billions are being shoveled at downstream fabricators serving the EV market to encourage them to set up their operations in Canada. One reason to do so is they can all see the potential lithium supply coming from Canadian pegmatites. But if the government is going to take a purist stance that there must never be a local loser, at the expense of net zero emission goals, there is a surprise coming. This year is shaping up to deliver a new round of extreme weather records, as Quebec's forest fire debacle has already shown. It is time to become pragmatic about all aspects of the various climate change mitigation solutions, in particular the discovery and mining of critical minerals.

NMR also invokes Goldman Sachs which has been predicting that Chinese and Latin American lithium supply will meet all demand growth, and mentions a GS prediction of $34,000/tonne for lithium carbonate in 2024. That is equivalent to $15.42/lb. If lithium carbonate is at that level rather than $10/lb as I assume, what is there to worry about? In fact $10/lb will be hugely profitable for pegmatites grading 1% Li2O or better. Demand will probably grew faster than supply, which NMR dwells on but treats it as a negative for PMET along the lines of "your project will take a lot longer to permit than anybody else's project, so by the time you are producing the market will be in oversupply and the lithium carbonate price will be a lot lower". Understanding the discovery exploration game is not something Goldman Sachs has much experience with because it is such a small space; its revenue generating strategy will involve helping downstream raw material consumers secure their supply. So of course GS is trying to talk down the prices of the lithium developers. And Night Market Research appears to have volunteered itself as foot soldier in this process. But in fact it has helped fulfill the requirement that no major new discovery is real until it has attracted a major short attack. |

Patriot Battery Metals Corp (PMET-V)

Unrated Spec Value |

|

|

| Corvette |

Canada - Quebec |

3-Discovery Delineation |

Li |

Where NMR thinks PMET sits in the Lassonde Curve, its own resource estimate prediction, and the Warrant Time Bomb |

Dia Met's Ekati as an illustration of the Lassonde Curve |

Liontown's Kathleen Valley reserve and price chart |

Lithium Carbonate Price Chart and Price-Grade Rock Value Matrix |

| Jim (0:16:52): What do you think of the farmout deal Azimut did with Rio Tinto? |

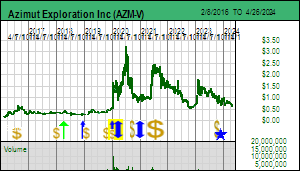

Azimut Exploration Inc announced a farmout deal on July 10, 2023 that has very positive implications for the James Bay region, though perhaps less for Azimut despite it being a stronger deal than the one Rio Tinto did with Midland Exploration Inc in mid June. Rio Tinto can earn up to 70% in the Corvet and Kaanaayaa properties by spending $114 million split between the properties over 9 years. The first stage requires Rio Tinto to spend $7 million on each property over 4 years to earn 50%, of which the first year is a firm commitment of $1.5 million for each property which Azimut gets to operate. In addition Rio Tinto must pay $850,000 per property, of which $250,000 is up front and $150,000 on each anniversary of the initial term. On this basis alone the farmout deal is much stronger than the one Midland secured from Rio Tinto on June 13, 2023.

Under Midland's deal Rio Tinto can earn up to 70% in 10 James Bay properties by spending $64.5 million over 10 years, with $14.5 million over the first 5 years to earn 50%. Unlike the Azimut deal where the amounts are split between the 2 properties, allowing Rio Tinto to spend only half the total if it drops one of the properties, the Midland deal appears to allow Rio Tinto to vest in all the properties regardless on which one it spends the money. Midland gets $500,000 up front and $100,000 on each anniversary of the five year 50% vesting term. The first 18 month expenditure is a firm $2 million but Rio Tinto is the operator and as such has complete control over where the money gets spent. In this deal Midland CEO Gino Roger handed off the lithium potential of its James Bay properties to Rio Tinto to figure out so it can concentrate on its other Quebec prospects.

Although similar in terms of spending requirements and vesting timelines, there is a dramatic difference that makes the Azimut deal superior and which undermines Rio Tinto CEO Jacob Stausholm's bluster that valuations of major LCT pegmatites (ie Patriot Battery Metals) are too expensive. Azimut's CEO Jean-Marc Lulin was able to secure an option where once Rio Tinto has vested for 70% in either property Azimut, instead of becoming a 30% joint venture partner at the mercy of Rio Tinto's cash calls, can elect to reduce to a 25% interest carried through production in the form of a loan from Rio Tinto that is repayable from 50% of Azimut's 25% share of cash flow. If Rio Tinto makes a major discovery on either Corvet or Kaanaayaa and quickly blows through $57 million on either property, Azimut can avoid the risk of death by cash call funding dilution. This is a part of the value trough within the Lassonde Curve that is deadly to juniors who must fund all or part of the boring feasibility demonstration stages. Midland did not get this option, perhaps because CEO Gino Roger did not ask for it. No doubt Lulin studied the Midland deal and the market's less than enthusiastic reaction to it, which allowed him to push for a stronger deal. What is surprising is that Rio Tinto capitulated to this demand.

However, neither deal is truly strong and both are strategic blunders created by an obsession with the prospect-generator-farmout model and what appears to be a dismissive attitude about Lithium Mania 2.0. Rio Tinto is doing its best to lock up title to claims near PMET's Corvette project for which we should get a maiden resource estimate by the end of July. Midland already blundered on November 10, 2022 when it optioned 85% of the "critical mineral (lithium)" rights to the Mythril property adjoining to the north of Corvette to Bob Wares' Brunswick Exploration Inc for $700,000 and $3.5 million exploration over 5 years. If there is any lithium pegmatite potential on Mythril, Brunswick will find out within 2 years and reap all of the speculative upside because the market does not care about the residual 15% contributing interest Midland will end up with.

Neither of Azimut's farmed out properties directly adjoins Corvette, so they represent potential for a parallel trend to the south, similar to the Champion Electric trend to the north owned 100% by Champion Electric Metals Inc. One hopes that by now Champion's CEO John Buick sees the wisdom of rebuffing similar farm-in overtures by Rio Tinto. So far Rio Tinto does not have any exposure to the La Grande Shear Structure trend which PMET's Corvette property straddles for 45 km, which continues another 15 km westward through the Pikwa property owned 50:50 by Azimut and Soquem, and another 30 km through the Cancet property of Winsome Resources Ltd, and then bends northwest into Brunswick's 90% optioned Plex property which straddles another 40 km of the prospective trend.

Why is Rio Tinto doing these apparently strong deals with Azimut and Midland? In the case of Midland only one property, Mythril East is near the Corvette trend; the rest are scattered throughout the James Bay region, with Galinee near Winsome's Adina discovery and the Komo property west of Allkem's Galaxy-Cyr project the most interesting in terms of standalone discovery potential. Rio Tinto was unable to secure the Galinee project of Azimut because it is already a 50:50 JV with Soquem. While it looks like Azimut got the better deal out of Rio Tinto than Midland, the opposite is actually the case. It will not take much exploration work to kill the low hanging fruit LCT pegmatite potential of Azimut's Corvet and Kaanaayaa blocks. Within two years after spending $3 million Rio Tinto can drop these properties knowing that they are not part of emerging world class lithium district. Its willingness to meet Jean-Marc Lulin's demands is really just a shoulder shrug for Rio Tinto, whose real target is PMET despite its professed aversion to high early stage valuations.

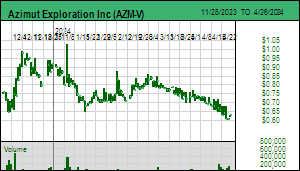

Whereas Rio Tinto is letting Azimut do the first pass lithium exploration, it is doing its own work on the Midland properties because some may have real but not obvious potential for major LCT-pegmatites. I am frustrated that Midland chose not to spend its own money on first pass boots on the ground exploration, but the company is busy with its many other Quebec projects and does not appear to believe Lithium Mania 2.0 is real. I don't think Azimut believes Lithium Mania 2.0 is real either; the James Bay map JML included with the news release is speckled with red dots representing claims targeting nickel which is where JML thinks the James Bay future lies, and perhaps the Patwon pencil deposit at Elmer into which Azimut has sunk $25 million without yet delivering a maiden resource estimate. In fact at the Metals Investor Forum in Vancouver in January 2023 JML spent 30 seconds on his lithium slide and at least 60 seconds on his nickel slide. It will be interesting to see how much the Azimut-Soquem JV gets done on Pikwa and Galinee this summer, the two most promising LCT-pegmatite properties accidentally in Azimut's James Bay portfolio. The real importance of the Midland and Azimut deals by Rio Tinto is that if PMET becomes the target for a hostile takeover bid, and the army of timid Canadian investors sitting on the sidelines swarms into the market as FOMO takes hold of the James Bay Great Canadian Area Play, they will be targeting those juniors who retain 100% of their holdings and have meaningful exploration strategies underway. |

Azimut Exploration Inc (AZM-V)

Fair Spec Value |

|

|

| Corvet |

Canada - Quebec |

1-Grassroots |

Li |

Midland Exploration Inc (MD-V)

Bottom-Fish Spec Value |

|

|

| Komo |

Canada - Quebec |

2-Target Drilling |

Li |

Regional Map of James Bay showing Azimut's Nickel and Lithium Postage Stamps |

Map showing location of Midland's James Bay Properties |

Azimut spending $3 million on peripheral plays but how much on Pikwa, the one that counts? |

Pikwa is where Azimut's boots should be pounding the ground in 2023! |

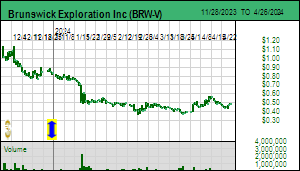

| Jim (0:25:56): What did the market like about Brunswick's latest news? |

Brunswick Exploration Inc announced on July 13, 2023 that it had identified multiple spodumene bearing dykes on its 90% optioned Anatacau Main project east of Allkem's Galaxy-Cyr project where Brunswick's Anatacau West property hosts the eastern extension of the Galaxy-Cyr system at least 300 metres onto Brunswick's property. The northern part of the Anatacau property hosts the continuation of the Galaxy-Cyr structure 22 km to the east, and Brunswick managed to have boots on the ground for 5 days in late May before sending the team off to the Mirage property where it spent a day outlining a spodumene enriched pegmatite boulder field about 200 m wide and with a 1,700 m strike perpendicular to the ice direction. Brunswick would have spent more time at Mirage to track down the bedrock source but on June 6 the Quebec government issued a forest access ban due to the fires in southern Quebec whose threat to infrastructure and communities forced the requisitioning of all helicopters to support firefighters.

The James Bay region is still subject to forest access bans, but these are expected to be lifted soon as heavy rains make their way across Quebec. Southern Quebec has in fact shifted to flood warnings as severe thunderstorms pummeled the Montreal-Ottawa areas and spawned tornadoes. The government has been letting fires in the James Bay region burn because they are not near infrastructure and the setting of height-challenged spruce tree stands separated by lakes and swamps makes wildfire spread in this region a much smaller threat than in the incendiary south. Resource juniors are lacing up their boots in anticipation of a green light next week.

The market reacted strongly to the news, bidding the stock as high as $0.82 on just over 1 million shares of trading after touching $0.68 on July 12 when the Red Cloud unit financing done at $0.85 in March came free trading. The stock had stalled as the market waited for a surge of clip and flip selling from Canadians no longer gripped by fear of missing out on Lithium Mania 2.0. But it was not obvious what the market was so excited about. The news was that prospecting had identified a cluster of parallel pegmatite dykes within which the largest was one that outcropped for 100 metres and at surface was 15 metres wide. Brunswick took 19 grab samples which assayed 1.2%-3.8% Li2O, generally above 2%. The Main dyke has light grey spodumene crystals up to 20 cm long and so these values are not representative but do confirm this is an LCT-pegmatite. The company did not disclose this outcrop earlier because it is small, similar to the Decoy outcrop at the Hearst property in Ontario where the absence of an update from a 1,000 m drilling program that began April 24 hints at disappointment. Brunswick wanted assay confirmation for the Anais showing before announcing it.

As Brunswick makes clear, its exploration strategy is one of search and destroy; if a property survives the first pass boots on the ground, it is followed by drill to kill, a massive process of elimination strategy. With properties in Saskatchewan, Manitoba, Ontario, Quebec and Atlantic Canada the junior's hope is that a discovery will emerge sooner than later. The forest fire ban has sabotaged this goal as far as its James Bay properties are concerned, for these have the highest potential to deliver a discovery comparable to PMET's CV5 pegmatite on its Corvette property.

It wasn't until I talked to Brunswick CEO Killian Charles that I discovered why they were so excited about the Anais showing at Anatacau Main. Unlike at Galaxy-Cyr and Anatacau West 22 km to the west where pegmatite occurs as an en echelon series of short northeast oriented dykes within an east-west shear structure, the Anais cluster of pegmatite dykes is oriented in the same direction as the structural zone they call a "deformation corridor". Whereas the Galaxy-Cyr pegmatite system outcrops so extensively it is visible using Google Earth, this is not the case to the east which consequently has seen little exploration for LCT-pegmatites. The Galaxy-Cyr dykes are filling Ridel dilation zones within the deformation corridor because the wandering pegmatite bodies exploited these openings. The risk with this type of system is that the dykes, while high grade, can be narrow and separated by wide spaces of country rock. Since this has to be open pit mined the grade of the resource will be the average of mineralized dyke and barren intervening rock. This is the problem with the Pontax lithium dyke system on which Cyngnus and Stria are working.

If, as seems to be the case at Anatacau Main, the pegmatite bodies exploited the weakness of a corridor in the direction of its strike, as has clearly happened with PMET's CV5 pegmatite for which brokerage analysts are estimating a resource exceeding 100 million tonnes of 1% Li2O or better, there is greater potential for significant pegmatite strike length to develop. The next step once the James Bay forest access bans have been lifted will be to channel sample the outcropping dykes to get a representative grade across the width and to step beyond the projected strike of the outcrop to see if it does indeed project under overburden. Brunswick has, apparently, already decided to permit a small drill program for the Anais showing because that is the most efficient way to establish the strike of a pegmatite body of which only a portion outcrops. The permitting cycle is about 45 days and is unaffected by forest access bans. It is Brunswick's goal to have a drill start roving from target to target in September.

The immediate priority will be to get back to Mirage and track down the source of the boulder field for which Brunswick should soon have grab sample assays. The prospecting team never made it to the Plex or Mythril targets in late May before the fires shut everything down, but these will become a priority in August, assuming a hot dry spell does not reappear. Killian also mentioned that Brunswick now has boots on the ground in the Hanson Lake area of Saskatchewan where there is a lot of outcropping pegmatite that could turn into low hanging fruit if prospecting confirms they are decently enriched LCT-type pegmatites. It remains to be seen how big the Anatacau Main pegmatites turn out to be. The company was able to option 90% from the Osisko group based on analysis of satellite imagery which revealed subtle signs of pegmatite. That, of course, is not sufficient to make the pegmatite LCT-type, so when the boots on the ground confirmed they were LCT-type with decent lithium grades, that was a boost for second order targets in the southern half of the James Bay region, and bodes well for juniors like Dios Exploration Inc which have developed similar second order targets in the southern half of James Bay using additional proprietary data sets that include lithium in till values. For me the key immediate milestone is finding the bedrock source of the Miraga spodumene boulder and confirming that its 1,700 m length corresponds with a similar length pegmatite body. |

Brunswick Exploration Inc (BRW-V)

Favorite

Fair Spec Value |

|

|

| Anatacau |

Canada - Quebec |

2-Target Drilling |

Li |

Remaining Forest Access Bans in Quebec & Closeup of Fire Activity iin James Bay area |

Anatacau Main Property and Anais LCT-Pegmatite Showing |

James Bay Map showing location of Brunsswick properties |

| Disclosure: JK owns shares of Brunswick; Brunswick is a Fair Spec Value rated Favorite; Midland is Bottom-Fosh Spec Value rated |