Hello Guest User, You are visiting this website from a computer with an IP address of 172.69.7.46 with the name of '?' since Fri Apr 19, 2024 at 8:17:34 PM PT for approx. 0 minutes now.

Kaiser Media Watch Blog - August 1, 2021 to August 31, 2021

KRO Blog Overview

The KRO Blog is where unrestricted content of a time sensitive nature is posted. It includes the Kaiser Media Watch Blog which features content involving John Kaiser produced by third parties such as the Discovery Watch series by HoweStreet.com, interviews by outfits such as Investing News Network, SDLRC related commentary, the KRO Monthly Summaries, and just about anything else John writes that is not intended exclusively for the fee based KRO Membership.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

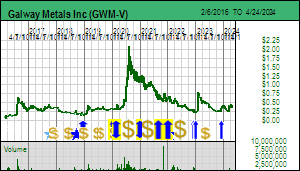

Galway Metals Inc management is the opposite of the "toiling geologist" Eastfield Group whose Cons Woodjam is featured in the second segment of this Discovery Watch episode. In fact they are so good I had to keep the company rated as a Fair Spec Value rated Favorite. In 2020 they raised lots of capital that allowed them to get serious about turning the new series of zones over a 4 km strike southwest of the Freewest discovered resource they purchased in 2016 into a resource estimate. But this resource estimate is still pending. We were supposed to see it in H1 of 2021, but then it was shifted to Q3 of 2021, which has one month left. So the market has become fatigued, and with gold no longer in an uptrend, the price has sagged, allowing me to upgrade Galway to a Good Spec Value rated Favorite. I haven't done an Outcome Visualization because I need to see the geometry of the new Jubilee etc Zone so that I can figure out what sort of mining scenario and operating costs are plausible. The upside resides in the exploration potential to repeat the North-South and Jubilee etc zones many times, feeding a central milling facility. The market wants to see the global resource clear the 1 million oz threshold, and those who know how to squeeze all those assays into a Leapfrog model are hoping for a resource in the 1.5-2.0 million ounce range. I can't wait for them to clear this hurdle because once it is done Galway has plenty of money left to reallocate its 6 rigs to start pounding all these other gold in soil anomalies they have developed near intrusions, for this is an intrusion related gold system which multiple intrusions within a district scale land package controlled by Galway. Although Clarence Stream is part of the Appalachian Gold Trend which includes the Fosterville fantasy playing out in Newfoundland, this is not a Bendigo style gold porn play that needs millions of metres of drilling to delineate a high grade resource. Tracker Aug 23, 2021 explains why I have made Galway a Good Spec Value rated Favorite but for now it is restricted to KRO members.

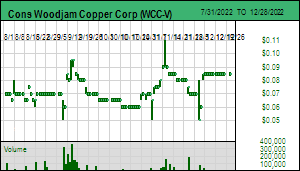

The Eastfield Group behind Cons Woodjam Copper Corp has created value for their backers for decades despite being notoriously obtuse when it comes to stock promotion. They were "toiling geologists" in the nineties when I launched the "bottom-fishing" concept as an independent analyst after leaving the brokerage sector in 1994, and they are still that today. Glory has escaped them because the value they have created through their Eastfield Resources Ltd mothership has been incremental. Glen and Bill are quintessential plodding tortoises who never win a gold medal but make it across the finish line. And you know what the fable says how this is supposed to turn out? WCC finally is a mechanical story in their hands that does not require a discovery to be turned into a mine. But they are addicted to discovery exploration and the current program is geared toward making Deerhorn bigger and proving that Megaton is more than a lower grade extension of the Southeast Zone. The market is pricing failure on the "extra" discovery front, and dismissing $4/lb plus copper as the new long term reality. I've done an Outcome Visualization for the Southeast Zone as it currently stands after Goldfields spent $30 million more than a decade ago and if my cost assumptions for a 30,000 tpd open pit scenario are correct, it deserves to be developed if you accept $4/lb plus as the new long term reality for copper. This doesn't even include blending gold enriched ore from Deerhorn into the SEZ flow-sheet. Now it is not yet for sure that Deerhorn is what it is and Megaton is a bust, but I am betting that this is the best outcome from the drill program currently underway because it would force Bill Morton and Glen Garratt to shift into feasibility demonstration mode. They have always farmed that out to others because that is not their style. So they are terrified about 2022 as the year when they have to shift Woodjam into feasibility demonstration mode, carrying on where Goldfields left off a decade ago. Maybe mother nature will bail them out by allowing the current Derrhorn hole to show there is a lot more size to Deerhorn than figured out by Goldfields, and that Megaton represents an extra 50% for the Southeast Zone. But mother nature seems to have a vendetta against my Favorites, so a pox on her, we don't need her to cooperate, we just need the Eastfield Group to embrace something they have avoided throughout their history.

Disclosure: JK owns Cons Woodjam; Galway Metals and Cons Woodjam are Good Spec Value rated Favorites

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

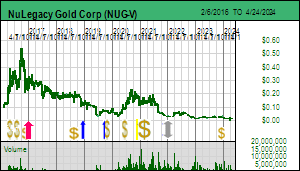

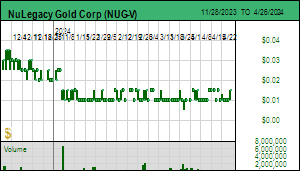

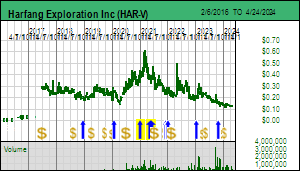

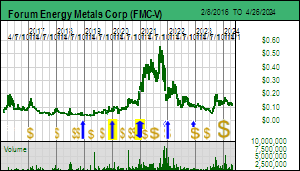

Disclosure: JK owns Nevada Expl Inc; NuLegacy is a Bottom-Fish Spec Value rated Favorite, Harfang is a Good Spec Value rated Favorite, Forum Energy is a Fair Spec Value rated Favorite

Discovery Watch is a weekly 15-30 minute audio show produced by HoweStreet.com where Jim Goddard interviews John Kaiser about resource juniors with projects that have caught John's attention. The projects will not be limited to companies he has covered through the Spec Value Rating System. Jim and John will periodically circle back to review the projects and if necessary close them out as no longer worth watching. Check out the catalog of KRO Free Stuff. KRO offers a USD $450 Annual Individual Membership. This Discovery Watch session is available via YouTube or Podcast.

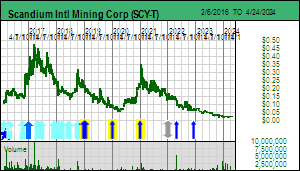

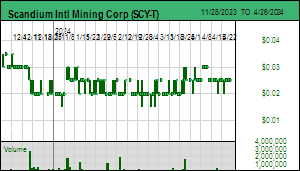

Scandium Intl Mining Corp updated its March 2020 corporate presentation on July 27, 2021, one month after announcing a CMR site hosting deal with Nevada Gold Mines for the Phoenix copper-gold mine in Nevada. The new SCY Presentation is only 13 slides and is chock full of information about the new CMR and HPA strategies that supplement the original goal of building an offtake order book so that funding the CapEx of Nyngan becomes possible. It also indicates that SCY must raise USD $7.5 million to fund the next 15 months, after which it will need to raise $125-$150 million to build the CMR plant, the CMR refinery and the HPA plant. Of these initiatives the HPA plan is completely under SCY management's control, so there are no more excuses left in terms of why SCY is such a market dog. It is do or die time coming up.

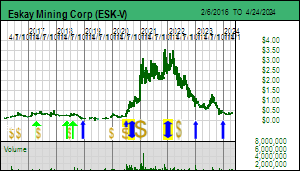

With 4 rigs turning since late June on the SIB project in the Golden Triangle, Eskay Mining Corp should soon be in a position to give us sulphide visuals for other targets beside Jeff and TV highlighted by the Skytem survey. So if you are an ESK shareholder or thinking that ESK might participate in a September rally, I suggest it is time to check out the July 15 Webinar KER's Cory Fleck and Quinton Hennigh did which includes a discussion of the recent Skytem survey for the northern two-thirds of the property. The stock is expensive at a $500 million plus valuation without a 21B Zone clone in sight, and we may not get that hole #109 intersection this year, but for now the story is confirming the district scale for gold-silver rich VMS deposits within this former marine basin layer cake which John DeDecker thinks had at least 3 distinct episodes of seafloor venting that have been made accessible by folding and thrusting that created 3 N-S oriented anticlines of which the Eastern Anticline has a very sexy target at its northern end coinciding with a very high value BLEG anomaly that has never been tested. The Webinar is 52 minutes long but it is a good way to refresh one's understanding of this play which in my view is the most important one unfolding in the Golden Triangle this year.

Towards the end of the webinar Quinton produces a hand drawn cartoon of what he thinks may be going on at the Jeff target where visuals reported July 13 are supportive of the model. If you listen carefully the cartoon will make sense, but to help out I have annotated the cartoon and provided it below.

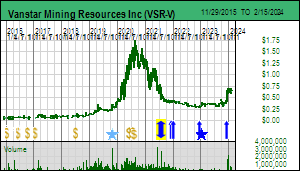

Vanstar Mining Resources Inc was introduced as a 2021 KRO Favorite via Tracker July 20, 2021 which will become unrestricted on August 6, 2021 to the general public in order to help illustrate the concept of outcome visualization to the Discovery Watch audience. The stock has been a market orphan since it went public in 2010 and stayed that way while the Nelligan discovery unfolded in 2015-2019 after IAMGOLD optioned up to 80% of the project. Part of the problem, and to some degree remains so, was that IMG had its hands full with its Cote open pit project in Ontario and suffered during the decade long gold bear market. But the stock was cheap after IMG published a maiden inferred resource of 96,960,000 tonnes of 1.02 g/t gold (3.2 million ounces) in October 2019 which was named the Discovery of the Year by AMEQ, Quebec's annual resource sector conference. The story caught the attention of Peter Grandich in March 2020 who with the help of his followers drove the stock to a peak of $1.75 on August 31, 2020 just after the gold rally peaked. In early 2021 Grandich began to sour on the Vanstar story because it was not clear what the 20% stake was worth, what the timeline for an exist strategy might be, and stalled gold rally as Bitcoin fever poached away traditional gold bug audiences. His capitulation occurred in July 2021, taking the stock back to a level where the fundamental value is very interesting, especially with IMG finally starting a serious drill program to infill the existing resource and test the western extension. The market fallout created by Grandich's exit offered an opportunity to undertake an Outcome Visualization where I imagined what Nelligan might be worth if turned into a 30,000 tpd open pit mine similar to what First Mining Gold had presented through its Springpole PFS in January 2021.

An OV is a discounted cash flow model valuation expressed in after-tax net present value terms using life-of-mine averages which is updated daily to reflect the latest exchange rates, metal prices and company fundamentals such as fully diluted and stock price that is available in a Members Only OV Report which includes all the assumption details, and as an Unrestricted OV Report which includes all the outcome values but not the detailed assumptions needed to run a cash flow model. Both, however, apply the rational speculation model to the outcome so that the future value implied by the DCF model can be discounted to the current stage of the project with the exploration-development cycle. And therein lies the problem for Vanstar because the project seems stuck at the infill drilling stage where the economic value has not been indicated by a 43-101 PEA level economic study. So even at $0.50 Vanstar offers slightly poor speculative value, though if a PEA were in hand the current stock price would represent fair speculative value.

Fair speculative value shows you what gains to expect as the assumptions in an OV are derisked as a project moves through the development stages, assuming they do not change (in reality they always change somewhat, usually for the worse as more conservative standards are brought to bear). When you see good speculative value implied by the current stock price, it usually is because the market is more pessimistic than you about the assumptions that generate your future outcome value. Then it becomes a question as to who will be right, you or the market? When you see poor speculative value it means the market is more optimistic than you, usually because it expects project fundamentals to improve beyond the assumptions you have embedded in your OV. In a case like Nelligan, the two variables that can change the most are the future price of gold and the size of the deposit where ounces are not boosted by simply lowering the cutoff grade. So I made Vanstar a Favorite even though the spec value is slightly above the fair value channel because I see room for a 50% resource expansion and I am bullish gold will trend above $2,000 without profitability undermining inflation caused by "fiat currency debasement". In addition to these two bets, I am also placing a bet on IMG's timeline for advancing Nelligan toward completion of a feasibility study, which is partly linked to higher gold price expectations which will make IMG less unloved by the market and more willing to accelerate work on projects such as Nelligan and use its higher priced stock as currency to acquire assets. Although IMG has the right to buy Vanstar's 20% stake at fair market value after it completes a feasibility study, which it would have to pay in cash, it might be interested to pursue an earlier negotiated buyout because the formal acquisition leaves Vanstar with a 1.5% NSR whose NPV would be worth more than the current market cap of Vanstar if you use a 5% discount rate to price it under the OV scenario. The key with this bet is that Vanstar is carried through production at Nelligan, so it cannot be forced onto a dilution treadmill by cash calls from a major which manages the data flow so as to minimize its marketability value for its junior Nelligan partner. In addition there is a management bet that as the market begins to understand the future fundamental value of Nelligan, the junior will once again end up with a stock price ahead of the results, except this time around, unlike when Grandich ran the stock to $1.75, there is a new management team on board with investment banking skills, some of whom, ironically, ended up there as a result of Peter's behind the scenes jawboning efforts last year. If the new CEO JC St-Amour starts making strategic acquisitions involving distressed assets, IMG might make a move to acquire Vanstar sooner than later. But for now management must wait for the market to recognize the fundamental value potential of Vanstar's 20% Nelligan stake.

Disclosure: JK owns Scandium Intl; Scandium Intl is a Bottom-Fish Spec Value rated Favorite, Vanstar is a Fair Spec Value rated Favorite, Eskay Mining is a Fair Spec Value rated former Favorite