| Terry Cain of the Global and Mail, Canada's equivalent of the New York Times, was tasked with finding answers for the following scenario: "For most people, it's a dream scenario. You are given $10,000, perhaps from an inheritance. You already have a decent, well-balanced retirement portfolio, so this money is really frosting on the cake. How should you invest it?" I was one of the people approached in August to provide answers, from which he synthesized the Globe and Mail article. Below is my original submission (the prices were as of August 17, 2016):

A question was posed, if within a properly balanced portfolio there were $10,000 available for high risk high reward investments, namely capital that could suffer a 50%-100% loss while aiming for 100% plus returns over a 1-2 year period, how would Kaiser Research Online allocate that $10,000? Kaiser Research Online specializes in high risk high reward junior public companies focused on the resource sector.

Any attempt to construct a portfolio consisting of companies from this sector during 2011-2015 would have been a disaster whether the companies were exploration/development juniors or producing majors. The important question is whether avoiding the resource sector entirely continues to be the best advice. While the easy money made buying resource juniors at the bottom of the bear market has already been made, those profits required a very risky bet on an unpredictable turnaround. Much more relevant is whether the turnaround in 2016 is a flash in the pan that will soon dissipate into a resumption of a five year bear market that drags on for several more years, or a turnaround with staying power that offers substantial gains from current levels. Kaiser Research Online accepted the challenge to construct a $10,000 portfolio because it is of the view that the resource sector turnaround has at least 1-2 years of running room courtesy of a dynamic that is very different from the metal price indifferent discovery focus of the eighties and nineties, and the metal price tracking boom that kicked in after 2003 when the China super-cycle hit a tipping point.

Overview: The resource sector entered a bear market in early 2011 that tracked the end of the China super-cycle for commodities and gold's retreat from a $1,950 peak when fears of "fiat currency debasement" and "hyper-inflation" failed to become reality. A very robust supply response by the mining industry collided with slower than expected macro-economic demand growth in the wake of the 2008 financial crisis. A political bias against fiscal stimulus in favor of austerity forced central banks to rely on monetary policy to stimulate employment growth. Although "quantitative easing" was expected to generate inflation, insecurity about the future inhibited investment spending and consumer credit expansion, which in turn reinforced consumer caution. As China shifted its focus away from expanding production capacity for an export economy, metal prices sagged. Although prices did not sag to pre-2003 levels, the profitability of mining dropped thanks to cost escalation specific to the mining industry, which in turn cooled general demand from emerging economies that relied on commodity production. India with its better demographics than China has been pegged as the next super-cycle driver, but with its economy at only 2% of global GDP, at India's current growth rate it cannot hit a super-cycle tipping point before 2025. India is a dream not relevant to the current situation.

Secular stagnation and deflation are the new watchwords that haunt the resource sector. With no macro-economic drivers to push up commodity prices, and the traditional reason to expect higher gold prices missing, one might expect the resource bear market to persist for another couple years. However, the five year bear market ended during the last week of January 2016. Fears that the rally in H1 of 2016 would fizzle with the summer doldrums have not been borne out. Gold prices are in an uptrend not because of inflation fears, but because of growing concern that status quo assumptions about a globalized economy "supervised" by the United States are no longer safe. The surprise nomination of Donald Trump as the Republican presidential candidate and the Brexit Leave vote symbolize an under-current of populist anger over perceived marginalization ("left behind") blamed on minorities such as immigrants or economic elites. Growing demand for gold ownership for non-inflation related reasons such as hedging uncertainty promise gold price gains not offset by cost inflation. Insecurity based gold demand growth does not deliver eye-catching gold price gains, but the steadier real price gains it delivers have a leveraged impact on the value of marginal mines or undeveloped deposits. The emerging resource sector bull market has staying power precisely because its gold narrative is no longer dominated by right wing ideology.

Fear rather than righteous indignation is the driving force behind the resource sector turnaround. The imperial ambitions of Russia and China represented by their respective activities in the Ukraine and the South China Sea pose difficult response problems in light of how critical China and Russia are as metal suppliers. The risk of supply disruptions due to geopolitical conflicts that threaten the principle of globalized trade is higher than it has ever been. The prospect for higher metal prices lies not with macro-economic demand growth, but with the potential that destabilizing forces will disrupt supply from certain countries.

With regard to the resource juniors, the appropriate stance is to focus on so-called optionality plays, namely projects with an existing resource that requires a higher metal price to be developed, but which also have untested exploration potential for a bigger and better grade resource. This applies equally to gold and other metal projects. The speculative attitude should be that higher metal prices would be welcome, but the expected payoff for the junior stock is the discovery of a deposit that is economic at prevailing prices. With regard to projects that do not qualify as an "optionality" play because they are earlier stage, emphasis should be given to juniors who are bringing something new to the table such as a target generation method or a creative rethinking of the project's geology. The recent turnaround for the resource juniors is emerging from a deeply depressed state; with the glass now switched to half full, the new junior bull market has 1-2 years of running room during which the better optionality plays will get absorbed by producers as metal prices creep higher, and new discoveries get bought out through competitive auctions.

The following portfolio of 6 companies assumes an equal amount purchased. It gives exposure to a gold optionality play (Midas), a zinc optionality play with discovery potential (InZinc), a gold-copper optionality play with discovery potential (Serengeti), innovation based gold exploration (Nevada Expl Inc), innovation based uranium exploration (Uravan), and primary supply commercialization for scandium, the ideal alloying partner for aluminum (Scandium Intl).

|  |

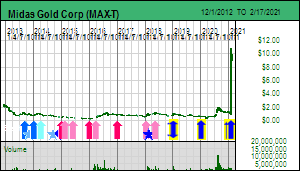

Midas Gold Corp (MAX-T: $1.11): Midas is fully funded to complete a feasibility study and obtain a mine development permit over the next 3 years for its 100% owned Stibnite project in Idaho. The December 2014 PFS envisioned a 20,000 tpd open-pit mine that would produce over 300,000 ounces gold annually for 12 years. The project has future resource expansion potential. Stibnite is an optionality play because its $1 billion CapEx requires a $1,500 or better gold price to justify development. With over $120 million already invested on feasibility demonstration, this project will be ready to go if gold develops a substantial uptrend not linked to collapse of the USD or high inflation. Midas is a takeover target at $2 plus when gold breaks through $1,500. The stock has suffered because of the perception that Idaho is a difficult permitting jurisdiction. The project is in fact a reclamation project funded by a gold mine to clean up the mess created during World War II when antimony and tungsten were mined. The proposed Stibnite Mine has an important antimony by-product credit which would become critical to the American economy if either China's dominant antimony supply subsides or supply is disrupted for geopolitical reasons.

|  |

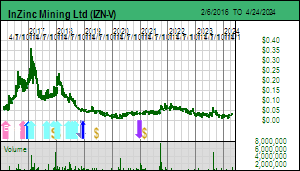

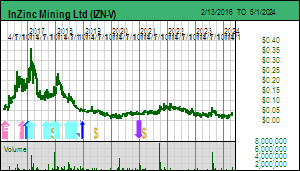

InZinc Mining Ltd (IZN-V: $0.20): InZinc owns 100% of the West Desert project located in Utah, a state friendly to mine development. A 2014 PEA proposed a 6,500 tpd underground mine that would produce 1.6 billion lbs of zinc as well as copper, indium, silver and gold credits over a 15 year mine life. CapEx was estimated at $247 million, but the project needs a zinc price above $1/lb to justify development. An alternative to waiting for a zinc bull market would be to explore for additional high grade tonnage for which the project has plenty of unexplored room. Of the base metals zinc has the most positive outlook because of western mine depletion with little replacement production in the development pipeline. The downside has been concern that China, the dominant zinc producer, would snuff out higher zinc prices by ramping up output as it has consistently done since 1980. However, China is undergoing an environmental awakening which includes a new water quality monitoring program that will put pressure on sources of heavy metal contamination such as small scale zinc mines. There is a shortage of juniors with advanced zinc projects. West Desert offers optionality on a stronger zinc price and additional exploration discovery potential.

|  |

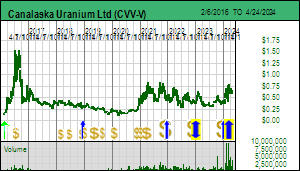

Uravan Minerals Inc (UVN-V: $0.38): Uravan has developed a geochemical exploration tool for identifying blind uranium deposits in the Athabasca Basin of Saskatchewan that are too deep for their alteration envelopes to be visible at surface. The theory is that microbes living within the rock at the unconformity and in the basement nourish themselves on sulphide bodies such as the high grade uranium deposits typical of the Athabasca Basin. Their methane exhalations function as transport vehicles for atoms from the deposit, of which radiogenic lead isotopes, the decay daughters of uranium, are the most diagnostic for the presence of a uranium deposit. The gases work their way through the basin sandstone, with their metal payload attaching themselves to clay particles at the surface. Uravan conducts grid surveys over large areas in search of certain isotope ratios as well as other marker elements. It has conducted case studies over the Centennial and Cigar Lake deposits which show a spatial correlation of geochemical anomalies at surface with deposit location at depths exceeding 1,000 m. A "Footprint" study sponsored by CMIC and Cameco being done on the McArthur River deposit using Uravan's method has apparently yielded a similar geochemical anomaly. Uravan owns 100% of the Outer Ring property in the Cable Bay corridor where a large geophysical anomaly coincides with a geochemical anomaly. A $2.4 million financing in August will enable Uravan to conduct a drill program to test the Outer Ring target. The story is similar to the hydrogeochemistry approach of Nevada Expl Inc except that in Nevada nobody generally owns gravel covered basin areas, whereas in the Athabasca Basin the prospective areas are already owned. Should Uravan deliver "proof of concept" through a discovery at Outer Ring, it would be in a strong position to option properties which lack good untested geophysical targets. Uranium prices remain at very bearish levels, but that is irrelevant because Uravan's goal is to discover a high grade deposit that is worth developing even at $26/lb U3O8. Furthermore, in the 5-10 years it takes to permit and build a mine in the Athabasca Basin the current over-supply caused by utility destocking in the wake of Fukushima will be over, and Chinese nuclear reactors coming on stream will have absorbed the recent supply surge from Kazakhstan.

|  |

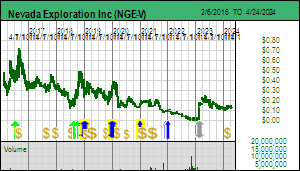

Nevada Exploration Inc (NGE-V: $0.57): NGE has developed an exploration method involving hydrogeochemistry that enables it to detect geochemical gold anomalies in gravel covered settings such as Nevada's basins. The science is well-established, though the application including gold is fairly recent because gold dissolved in water occurs in parts per trillion which was below the detection limits of labs until 15 years ago. NGE has established protocols for measuring gold and has collected nearly 6,000 samples over the shallower parts of Nevada's basins. This regional sampling has identified a couple dozen anomalous hotspots that require further sampling. Currently NGE owns claims on four such targets, of which the most important ones are Grass Valley, Grassy Valley South and Kelly Basin covering areas that have seen little past exploration due to the lack of outcrop. What makes northern Nevada especially interesting for gold exploration is that over 300 million ounces have already been found by testing outcrop or projecting under the gravel from outcrop. But there has been no way to "see" through the basin gravels where there is no outcrop to point the way. This is important because Nevada's basin and range topography formed after the rich Carlin type deposits formed. The geometry of the basin and range is independent of the structures and traps that helped these deposits form. So half of northern Nevada's gold endowment has been "artificially" hidden beneath basin gravels. NGE's strategy is to generate targets through groundwater sampling that are otherwise invisible to exploration methods. In 2015 NGE undertook a reorganization that brought former Uranerz chairman Dennis Higgs on board to tackle the financing challenge for this sort of conceptual play. Finding another world class Cortez Hills, Twin Creeks or Pipeline equivalent deposit would have a very high price impact on the stock. Unlike a more traditional exploration junior, NGE's deployment of a fairly unique exploration strategy would enable it to replicate success over and over again with properties whose potential is invisible to competing exploration juniors.

|  |

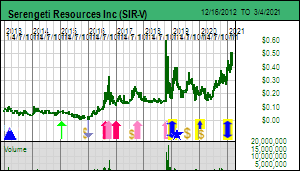

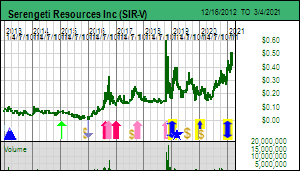

Serengeti Resources Inc (SIR-V: $0.20): Serengeti owns 100% of the Kwanika project in British Columbia where it made a significant gold-copper discovery in 2007 on which it has spent over $20 million. A 2013 PEA proposed a 15,000 tpd combined open pit and underground mining operation with a CapEx of $364 million to produce 555 million lbs copper and 489,000 oz gold over a 14 year mine life. However, the project is not viable at current metal prices. In 2016 a Korean company called Daewoo agreed to earn up to 35% by spending $8.2 million over 3 years. The deal includes several other properties owned by Serengeti in the vicinity. Daewoo's vision is to establish a central milling facility at Kwanika for which the Central deposit can achieve payback and which will be fed by future discoveries on the remaining properties. A 3 hole drill program in 2016 will help Serengeti assess if the grade of the underground portion of the Central Zone can be improved. One of the holes will also test an IP geophysical anomaly at a depth of 500 metres that extends for 1,000 metres in a northerly direction where shallower prior drilling failed to intersect mineralization. If the anomaly is a sulphide body enriched with copper and gold, Serengeti and Daewoo would have on their hands a new discovery that could support a standalone mine development at Kwanika. Serengeti's Kwanika project offers optionality on better copper and gold prices and exploration potential for a discovery substantially bigger than resources already established.

|  |

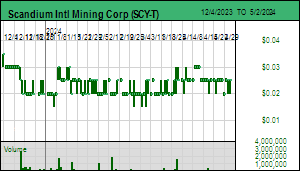

Scandium International Mining Corp (SCY-T: $0.15): Scandium Intl has published a DFS for a 240 tpd mine in New South Wales of Australia that proposes to produce 36-42 tonnes of scandium oxide annually. At a price of $2,000/kg Sc2O3 the DFS indicates an after-tax NPV of US $177 million (10%) and a 33.1% IRR, which is robust enough to justify spending the $87.1 million CapEx to build a mine. Not included in the valuation is the potential to expand capacity 3-4 times using feedstock from Nyngan itself and the nearby similar Honeybugle deposit. The market is not factoring such expansion potential because its primary concern is whether or not SCY would be able to find buyers for 36-42 tonnes of scandium oxide of which currently the world is supplied by only 10-15 tonnes from various by-product sources such as the Bayan Obo rare earth mine, Russian in situ leach uranium mines, and titanium doxide waste stream stripping operations. The speculative question is whether the market size is a function of demand, or a function of the non-scalable by-product supply. And is it like rhenium or beryllium limited to high temperature aerospace and military applications, or is like niobium whose unlimited availability from the Araxa mine has created a US $2.4 billion annual market as an alloying agent for steel? Given the existing literature and patents about what scandium does to aluminum as an alloying agent, namely strengthening it, making it corrosion resistant, and weldable without weld joint strength loss, there is enormous demand potential from the transportation sector where weight reduction is key to lower fuel consumption and meeting carbon dioxide emission targets. The aircraft and automotive industries are obvious offtake candidates, though they cannot afford to use Al-Sc based components until the first primary, scalable scandium mines have demonstrated an ability to produce and sell scandium oxide at a stable price that still leaves the operations profitable. Less critical end uses involve sports equipment such as bicycles, smartphone cases, and even beverage containers for which Al-Sc alloy can be quickly deployed, and where the failure of Nyngan to deliver is not a planning disaster for the end-user. Nyngan is the most advanced of several scandium enriched laterite deposits found in the past decade which represent game-changers for the evolution of scandium consumption, not just as an aluminum enhancing alloying agent, but also in a variety of innovation areas such the role scandium plays in making Bloom Energy's solid oxide fuel cell viable. Once it has been demonstrated that primary, scalable scandium supply at a stable offtake price is a new reality, the scandium offtake market has the potential to grow to 1,000 tpa over the next decade, a market worth $2 billion that will be shared by several producers, of which SCY will have the first mover advantage. Key upcoming milestones are additional offtake agreements, a mining permit, and construction financing by Q1 of 2017. Assuming the equity portion of project financing gets done in the $0.40-$0.60 range, the 3-4 year price target will be in the $2 plus range. SCY differs from the other juniors in that its upside does not hinge on higher metal prices or new discoveries.

Disclosures: John Kaiser owns shares in InZinc, Uravan, Nevada Expl Inc and Scandium Intl. |