Hello Guest User, You are visiting this website from a computer with an IP address of 172.69.6.166 with the name of '?' since Wed Apr 17, 2024 at 6:56:59 PM PT for approx. 0 minutes now.

SV Rating: Fair Spec Value - Favorite - as of December 29, 2023: 92 Resources Corp has a Bottom-Fish Spec Value rating based on the strategic location of its Corvette "lithium" project within the apparent trend of the emerging Mythril copper discovery of Midland Exploration Inc. NTY, which has 87.8 million issued and 104.6 million fully diluted, of which declared insiders own less than 2%, and about $600,000 in flow-thru capital that must be spent in 2019, would not qualify for a Bottom-Fish or higher Spec Value rating if it were not located near ground zero in what appears to be shaping up as a Great Canadian Area Play, a resource junior market phenomenon which we have not seen since 2007-2008 when Noront ignited the McFauld's Lake region with its nickel discovery which failed to achieve world class scale. The James Bay region had a mini area play in 2004-2006 when Virginia Gold discovered the Eleonore gold deposit. This time around Quebec has formalized James Bay as part of Plan Nord, a government initiative to develop the northern two-thirds of the province. The James Bay Plan Nord Area Play does not yet have confirmation of a world class discovery, which could come in early May when Midland reports results from its initial 11 hole program at Mythril, though will more likely unfold during the 2019 summer as Midland gets 3 drill rigs turning and a better understanding emerges for this new copper system which has attracted the attention of BHP, the world's biggest copper producer which is not interested in anything with less than world class scale. The realization that NTY is positioned to become the third hottest junior after Midland and Azimut Exploration Inc during the emerging stage of the James Bay Plan Nord Area Play has lit a fire under a group that has suffered as the resource junior bear market trudges along in its eighth year. NTY listed by IPO in March 2010 with a Sedex play in British Columbia's Ketchika trough as a junior called Rio Grande Mining Corp, split its stock 1:2, acquired a Colombian project in 2011, underwent a management upheaval in 2012, rolled its stock back 7:1 in 2013, optioned the Zim Frac silica project in 2014, and succumbed to another 5:1 rollback and name change on June 10, 2014. 92 Under the new CEO Adrian Lamoureux and CFO Dusan Derka NTY became part of the Zimtu orphanage operated by Dave Hodge and changed its focus in 2016 to the lithium boom spawned by the electric vehicle mania created by Tesla. With the help of Jody Dahrouge, who remains one of the larger shareholders, NTY optioned several projects in the James Bay region of Quebec that either covered known pegmatites, the primary bedrock host for lithium, or were in proximity to advanced projects such as Nemaska and Galaxy's James Bay deposit. By 2018 the lithium boom had run its course as the South American brine operators secured expanded production quotas for their salars, the Australians developed new pegmatite based bedrock mines, the price of lithium carbonate dropped more than 50%, and the ice cream parlor started featuring vanadium as the new flavor of the month. So in 2018 NTY optioned the Silver Sands vanadium play next to the Pine Pass project in BC just in time for the area to come under provincial consideration as a protected area for caribou habitat. But NTY also decided to double down on the Corvette lithium project by doing a deal with Osisko Mining Inc that allows it to earn 75% of the FCI claim, an inlier within the Corvette claim package which covers about 75% of a pegmatite trend. With the vanadium pivot dead on arrival, and the Corvette claim's lithium expansion potential colliding with the end of the lithium boom and fallout from the unfolding Nemaska fiasco, NTY managed to squeak a year end $618,000 flow-thru financing at $0.05 which gives it enough money to work on the Corvette project in 2019. But in what amounts to serendipity, the Mythril copper discovery announced by Midland in October 2018 now appears to be part of a 40-60 km east-west trend that projects westward about 10 km onto Azimut's Pikwa property based on a just disclosed copper lake-sediment anomaly, and 20 km eastwards on Midland ground before Midland's staking collides with the pre-existing Corvette claims, which run for about 10 km before Midland's claims resume for another 15 km farther east. At this point it is not clear what geology is relevant, but it is important that BHP invested $5.85 million in Midland at a 36% premium based in part on its assessment that the Mythril "magmatic-hydrothermal" system does not readily match any deposit style in its catalog. NTY lacks a strong technical team, but does have on its advisory board Darren Smith, a Quebec based geologist who worked on the Eldor rare earth project and is part of Jody Dahrouge's consulting firm which is active in Quebec. Market interest in Quebec's lithium potential is likely down for the count, but these pegmatite systems sit within greenstone belts which have gold potential. NTY has several other such projects in the James Bay area that can benefit from a gold focus. But as of Q2 2019 NTY's Bottom-Fish Spec Value rating hinges entirely on the accidental location of the Corvette project within a trend controlled by Midland. To what extent 92 Resources Corp becomes a major James Play junior will depend on how quickly Midland's discovery gets acknowledged as world class with regional replication implications and how quickly NTY mobilizes its focus on the broader potential of the Corvette project. Unlike Midland and Azimut which have strong shareholder bases and corresponding poor liquidity, NTY has a weak structure screaming for a rollback whose liquidity will become a blessing for the market as the James Bay Plan Nord Area Play gains traction.

Corporate Change History

#Old for New

Last Price

Prior Name

Subsequent Name

Details

Dec 1, 2010

Sub-Division

0.5:1

$0.83

Rio Grande Mining Corp (RGV-V)

Rio Grande Mining Corp (RGV-V)

May 13, 2013

Reverse Split

7:1

$0.01

Rio Grande Mining Corp (RGV-V)

Rio Grande Mining Corp (RGV-V)

Jun 10, 2014

Name Change

5:1

$0.02

Rio Grande Mining Corp (RGV-V)

92 Resources Corp (NTY-V)

Oct 17, 2019

Name Change

10:1

$0.02

92 Resources Corp (NTY-V)

Gaia Metals Corp (GMC-V)

May 31, 2021

New Exchange Listing

1:1

$0.09

Gaia Metals Corp (GMC-V)

Gaia Metals Corp (GMC-CSEV)

Jun 10, 2021

Name Change

3:1

$0.09

Gaia Metals Corp (GMC-CSE)

Patriot Battery Metals Corp (PMET-CSE)

Jul 14, 2022

New Exchange Listing

1:1

$2.58

Patriot Battery Metals Corp (PMET-CSE)

Patriot Battery Metals Corp (PMET-V)

Feb 1, 2024

New Exchange Listing

1:1

$6.88

Patriot Battery Metals Corp (PMET-V)

Patriot Battery Metals Corp (PMET-T)

Recommendation History

Edition

Date

Price

Recommendation

Gain

SVF2024

12/29/2023

$9.93

Fair Spec Value Favorite

0%

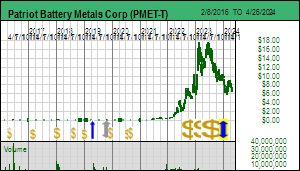

Charts & Financing Activity

Most recent 43-101 resource estimate Prior resource estimate PEA PFS FS/BFS/DFS

Private Placement Key

less than $500,000

$1,000,000 - $2,000,000

$5,000,000 - $10,000,000

$20,000,000 - $50,000,000

$500,000 - $1,000,000

$2,000,000 - $5,000,000

$10,000,000 - $20,000,000

over $50,000,000

Private placement financing dates and value ranges are based on transactions reported by the TSXV Monthly Review.

Past Insiders and Reported Shareholders - Current Ownership Status unknown - positions may be pre-rollback

Related Party

Occupation

Related Since

Insider Ended

Director Ended

Capacity

Ownership

Dusan Berka

Engineer

3/2/2012

6/13/2023

6/13/2023

CFO

631,333

John Bevilacqua

6/5/2012

1/16/2014

1/16/2014

Director

0

Brandon Boddy

Broker

11/2/2010

Placee

100,000

Danny Brody

Broker

11/2/2010

Placee

20,000

Susana Carpena

Broker

11/2/2010

Placee

280,000

Julie Catling

Broker

7/31/2012

Placee

50,000

Bryce A. Clark

Accountant

11/2/2007

4/29/2013

4/29/2013

Director

3,560,000

Edward Dockrell

11/2/2010

Placee

75,000

Teymur Englesby

Broker

11/2/2010

Insider

40,000

Jon Christian Evensen

Analyst

4/13/2022

1/26/2023

1/26/2023

Director

0

Dallas Fahy

Broker

7/31/2012

Placee

100,000

Robert Findlay

6/25/2012

12/16/2019

12/16/2019

Director

100,000

J. Casey Forward

Accountant

9/2/2009

6/25/2012

6/25/2012

Director

0

Sean Gercsak

Broker

11/2/2010

Placee

35,000

David L. Hamilton-Smith

Broker

7/31/2012

Placee

100,000

R. Todd Hanas

Investor Relations

1/14/2020

8/11/2022

8/11/2022

Director

62,500

Dennis Hoesgen

Broker

11/2/2010

Placee

115,000

Eric Hoesgen

Broker

11/2/2010

Placee

115,000

A. Salman Jamal

Businessperson

7/18/2014

Insider

1,000,000

David Kearns

Broker

11/2/2010

Placee

90,000

Adrian Lamoureux

1/16/2014

7/19/2022

7/19/2022

CEO

118,333

Doug March

Broker

11/2/2010

Placee

10,000

Jerry A. Minni

Accountant

5/10/2007

Director

2,640,000

Michael Schuss

Consultant

1/15/2014

5/21/2015

5/21/2015

Director

0

Pamela Starek

Broker

11/2/2010

Placee

25,000

Read Taylor

9/11/2012

12/24/2012

12/24/2012

Director

0

Li Zhu

Broker

7/31/2012

Placee

50,000

Share positions of current insiders based on last AGM circular, ownership % based on current Issued. Share positions of past insiders and shareholders have not been adjusted for rollbacks or splits.

Active Index Memberships

Membership Start Date:

December 29, 2023

Start Price:

$9.93

KRO Favorites 2024: Features companies designated 2024 KRO Favorites, based on closing price December 29, 2023 or when added during 2024..

Membership Start Date:

August 1, 2023

Start Price:

$15.00

KRO James Bay Lithium Index: The KRO James Bay Lithium Index was created to track Lithium Mania 2.0 within the James Bay region of Quebec where several world class lithium pegmatite deposits have been established. Because pegmatites occur within a geological setting prospective for precious and base metals deposits, which have been the historical focus for exploration in the James Bay region while pegmatites were ignored due to the small market for lithium which was worth a mere $200 million in 2005, all companies with property have been included on the premise that any could make an important lithium pegmatite discovery even though not yet looking for such deposits. This also means that some truly horrible juniors are included and consequently index inclusion should not be treated as a judgement about the company. See the Lithium Resource Center a general list of lithium focused companies and lithium related resources.

A Spec Value Hunter table allows speculators to identify which projects offer poor, fair or good speculative value according to the rational speculation model. The speculative value depends on the project stage, the project's implied value as calculated by the company's fully diluted, stock price and net project interest, and the dream target deemed appropriate for the project. A dream target is what a project would be worth in discounted cash flow terms once in production.

Poor Speculative Value -

Fair Speculative Value -

Good Speculative Value -

Note: narrow arrows indicate IPV is outside the fair value channel but within 25% of the fair value limits

Color Key for Target Outcome Achievability Ranges in millions ranked from most to least achievable

below $25

Should be Private: Artisanal, Placer, Mom & Pop Shop

$25-$50

Tiny Scale: underground mine or quarry - not worth the bother

$50-$100

Small Scale: junior needs to self-develop

$100-$250

Buyout Target: by Lower Tier Producers

$250-$500

Buyout Target: by Mid-Tier Producers

$500-$1,000

Ideal Target for Junior: Buckhorn, Sleeper

$1,000-$2,000

Almost World Class: Ekati, Red Chris, Brucejack, Juanicipio, Stibnite

$2,000-$5,000

World Class: Eskay Creek, Hemlo, Hermosa-Taylor, Oyu Tolgoi, LaRonde, McArthur

$5,000-$10,000

Giants: Escondida, Sullivan, Carlin Trend, Kidd Creek, Orapa, Kamoa-Kakula

above $10,000

Off the Scale District: Wits 1.0, Araxa, Sudbury Basin, Bayan Obo

The target outcome range required for the current implied project value to represent fair speculative value is based on the upper and lower certainty limits associated with the project stage. The color coding is based on the target outcome using the mid-point of the certainty range.

Active Company Projects

Project

Location

Net Interest

Stage

IPV $ MM

Fair Spec Value Required Target Outcome Range

$100

UPV $500

$2000

Target Metals

Deposit Style

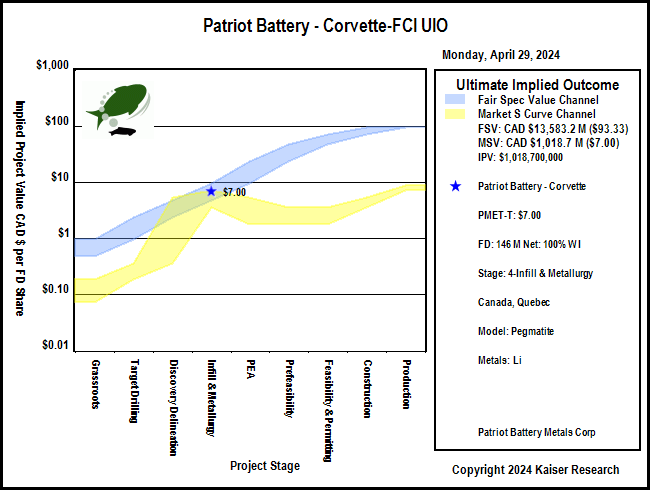

Corvette

Canada - Quebec - James Bay

100% WI

4-Infill & Metallurgy

$1,071

$10,711 - $21,423

Lithium

Pegmatite

Hidden Lake

Canada - Northwest Territories

10% TC

2-Target Drilling

$10,711

$428,454 - $1,071,134

Lithium

Pegmatite

Pontax River

Canada - Quebec - James Bay

100% WI

2-Target Drilling

$1,071

$42,845 - $107,113

Lithium

Pegmatite

Eastmain

Canada - Quebec - James Bay

100% WI

1-Grassroots

$1,071

$107,113 - $214,227

Lithium

Pegmatite

Golden Silica

Canada - British Columbia - Southeast BC

100% WI

4-Infill & Metallurgy

$1,071

$10,711 - $21,423

Silica Sand

Mineral Sands

Lac du Beryl

Canada - Quebec - James Bay

100% WI

1-Grassroots

$1,071

$107,113 - $214,227

Lithium

Pegmatite

Silver Sands

Canada - British Columbia - Northern BC

100% WI

1-Grassroots

$1,071

$107,113 - $214,227

Vanadium

Sediment Hosted

Project Stage

Flagship

Secondary

Active

Grassroots (1) & Target Testing (2)

Discovery Delineation (3)

Infill Drilling & Metallurgy (4)

PEA (5) or PFS (6)

Feasibility & Permitting (7)

Construction (8) or Production (9)

Clicking on the project icon will display a popup identifying the company project, its stage and target metals, basic facts, a chart, a link to that project within that company's KRO Profile, a link to the most recent news release, and a link to the most recent KRO comment if one exists.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 0.00%

Ownership Terms: Corvette claims 100% owned. Adjacent claims (FCI) optioned on Aug 27, 2018 75% from Osisko Mining Inc for 2 million shares and $2.2 million exploration over 3 years to earn 50%, and spending another $2 million to earn 75%. On Apr 24, 2019 the FCI agreement was amended to include the FCI West block (4,253 ha) in the agreement without any additional changes. This project consists of the 100% owned Corvette block and the 75% earn-in West and East FCI blocks.

Net Interest: 10% TC Vested: Yes Uncapped NSR/GOR: 1.00%

Ownership Terms: Acquired 100% on Feb 16, 2016 from DG Resource Management Ltd (50%), Zimtu Capital Corp (25%) and Michael V. Sklavenitis (25%) for $85,000, 4,000,000 shares and $500,000 by May 31, 2018 (done). DG retains 2% NSR of which 1% can be bought for CAD $2 million. On Jan 22, 2018 92 optioned out to Far Resources Ltd whhich can earn 60% by paying $50,000, issuing $500,000 worth of stock (555,555 @ $0.90), and spending $500,000 by Feb 28, 2019 (done). Far can increase to 70% by issuing $250,000 worth stock and spending $500,000 by Feb 28, 2020, 80% by issuing $300,000 worth stock and spending $600,000 by Feb 28, 2021 and 90% by issuing $400,000 worth stock and spending $700,000 by Feb 28, 2022.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 0.00%

Ownership Terms: Agreement July 25, 2016 to acquire 100% from DG Resources Management Ltd and Michael Sklavenitis for 3,000,000 shares and $50,000 cash by May 31, 2018 (done). DG retains 3% NSR of which 1.5% can be bought for $2 million.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 1.00%

Ownership Terms: January 2014 agreement to acquire 100% (ZimFrac) from Zimtu Capital Corp. and Cannon Bridge Capital Corp., two arm's-length vendors, in consideration for the issuance of one million common shares to each, for a total of two million common shares, and subject to a 2-per-cent net smelter returns royalty. Agreement Mar 3, 2017 to acquire Golden Frac claims ffrom Dahrouge Geological Consulting Ltd and DG Resource Management Ltd for $40,000. Subject to 2% GORR in favour of DG of which 1% can be bought for $2 million.