Hello Guest User, You are visiting this website from a computer with an IP address of 172.69.58.68 with the name of '?' since Fri May 10, 2024 at 3:19:26 PM PT for approx. 0 minutes now.

Kaiser Research Online is an information portal featuring all resource companies listed on the ASX, TSX, TSXV and CSE. Membership is available as an Individual Annual KRO Membership at USD $450 and as Multi-User Corporate Annual KRO Membership at USD $1,000. Use your Email to retrieve your login credentials if you have previously registered. See Membership Details for an overview of KRO.

The KRO Summary lists all Trackers and Blogs published during the designated weekly or monthly period so that so readers can easily catch up on what they may have missed. We no longer notify KRO members by email about new material except in special circumstances. When a Tracker is posted at KRO we notify members through the KaiserResearchOnline Slack Workspace. If you are an active KRO member and not registered on Slack, please let us know and we will send the invite. We will email the link to the KRO Summary to all KRO members when it is published. We will also Tweet the link so that Twitter followers can catch up at their leisure. The title links to the Tracker or Blog, the charts in the Discovery Watch Blog link to the YouTube audio segment for that company, and the Tracker charts link to the free Corporate Profile. On occasion we may include commentary on the state of the market. Blog content is unrestricted but Trackers are always restricted to KRO members unless one has been tagged to become unrestricted. Check the General Release Schedule to see which Trackers are already unrestricted or scheduled for general viewing.

A Resource Junior Bull Market Awakens

June proved to be a very turbulent month as the Black Lives Matter protest movement exploded at the same time as states started easing the lockdown response to Covid-19. The result has been an explosion of the daily new infection count into record territory, creating a stark contrast between the United States and Europe where considerably harsher, science based lockdown measures not only flattened the infection curve's trajectory but suppressed it to a substantially lower level than achieved in the United States.

One shudders to think what the American curve would have looked like if Americans had packed their churches on Easter (April 12) as Trump had urged. The effect of the June surge was to stall the V-shaped rebound in the general equity markets which still managed to deliver the best ever quarterly return from the depths of March 31, 2020. Trump's dubious choice of a "law and order" platform for the November 3 US election targeting a shrinking portion of American voters gives legs to the notion that his name may not be on the November ballot. While economic indicators show a recovery in areas such as employment, those are trailing numbers which in four months, when the northern hemisphere flu season is back, will reflect the consequences of a renewed lockdown. The alternative is to give up trying to suppress Covid-19 contagion with lockdown strategies and just let the virus cull the sick and elderly. That can't go over well with Trump supporters, and will prod Republican politicians to rethink their role as Trump's enablers. Meanwhile the rest of world, having sacrificed hard to subdue Covid-19, is embracing the idea of Fortress America by erecting its own wall around the United States.

The stalling of the V-shaped market rebound enabled gold to push higher toward $1,800, the next breakout challenge on the way to the ultimate milestone, the $2,000 level. Since the start of 2020 the World Gold Council sponsored GLD ETF has added nearly 9.6 million ounces gold, for a total of 38.3 million that is close to the December 7, 2012 peak of 43.4 million ounces. The KRO Gold Producer Index, which doubled from its March abyss until early May when it stalled, resumed an uptrend in the second half of June and is now up 28% from the start of the year.

The big surprise, however, is not the growing optimism that the extreme uncertainty unleashed by Covid-19 and America's erratic policies will drive gold into the $2,000-$3,000 range, but rather the awakening experienced by the resource juniors during the second half of June. The first sign in early June was a spate of Bay Street financings, often with Eric Sprott as a lead order, where a financing would be announced in the morning, upsized in the afternoon, and again upsized to double the original amount by the time it closed two weeks later. This was happening to the higher profile juniors with strong management teams and it signaled a pivot by Bay Street away from non-resource stories like cannabis. Bay Street was suddenly in a hurry to secure exposure to the resource juniors which offered considerably better leverage on the upside than gold itself or even the producers. But there was something peculiar about the companies Bay Street was financing. One would have expected the target to be juniors with marginal ounces in the ground that stood to benefit from a higher real gold price, as was the case from 2003-2012. That gold price driven bull cycle raised enormous capital for "feasibility demonstration" raised mainly from institutional investors. The financing focus today, however, are juniors which have a gold system that is inadequate in terms of scale, so that even a higher gold price won't make such deposits worth developing, but which lend themselves to a geological rethink in terms of potential that can only be assessed through exploration drilling. The poster child for this approach is Osisko Mining and its Windfall project in Quebec. While that was an exercise of brute force financing and exploration in 2016-2019 that few other juniors could replicate, today it is a template of what is possible when you throw enough money at exploration drilling.

During that brief window from 1978-80 when gold surged to $850 before settling back into the $350-$400 range the juniors experienced a major bull market as gold delivered a substantial real price gain that became the basis for two decades of exploration discovery driven bull cycles. Hemlo's 23 million ounce discovery kicked it off in 1981 during the Volcker induced recession. Despite the perpetual gold bug call for $2,000 gold was stuck in a sideways market that became an outright bear as it descended to $265 as the world celebrated America's triumph as the sole super-power. During these two decades the resource juniors would experience market cycles which typically had a couple bull years followed by a couple bear years, with a bull cycle emerging whenever a junior made a substantial new discovery. Prominent world class examples were Eskay Creek, Ekati, Voisey's Bay, Pierina and the Busang hoax while smaller success stories like Casa Berardi periodically helped clusters out of the doldrums.

The idea of a big discovery switching the glass half full and rising ended in 2003 when the China super-cycle kicked in, dragging up the real price of metals, and the gold cycle kicked in as it became apparent that financial engineering was erecting a flawed foundation for the global economy during the first decade of the new century. Yes there were a few major discoveries such as Frutta del Norte in Ecuador, but they did not serve as an inspiration for the broader market. Value creation resided in the combination of rising metal prices and dollars sunk into feasibility demonstration which led to an unprecedented takeover binge as producers absorbed these development ready assets that the juniors had upgraded through what was often just mechanical exploration work. The financial crisis of 2008 proved to be a temporary interruption as China's fiscal stimulus program rebuilt demand for metals, and the quantitative easing strategies of central banks drove gold well beyond its inflation adjusted value of $1,274 toward $2,000. But by 2012 austerity measures had gained the upper hand in the United States and Europe, stalling metal and gold prices, and ushering in what proved to be a decade long bear market for resource juniors. During this period the traded value of juniors listed on the TSXV shifted overwhelmingly to non-resource juniors with stories like blockchain and cannabis. A promising turnaround in 2016 turned out to be tracking an uptrend of gold alone, and stalled when the gold uptrend stalled in late 2016. In 2017 the market was inspired by the possibility that Novo had found Wits 2.0 in Australia's Pilbara, but that gasp of optimism about a global discovery focused exploration boom dissipated in 2018 when it became apparent that Novo could not solve the measurement problem in a timely fashion. But in late June the daily traded value of TSXV resource listings hit the highest level since late 2012.

This value traded peak, achieved on July 2, 2020, is barely noticeable in the short term graphic above, but it is a sign of substantially higher trading value to come. The initial focus of Bay Street's return to funding resource juniors with a discovery exploration focus has its roots in the bear market during which investors tired of being dependent on forces beyond a company's control, such as the metal price. Metal prices did nothing for the juniors during the past decade except briefly when critical metals such as cobalt, lithium and vanadium linked to emerging technologies underwent price spikes. During the past decade there were very few world class discoveries.

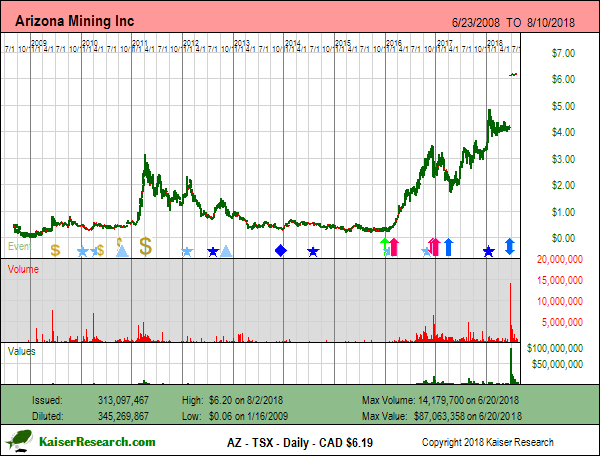

The notable exception was my recommendation at $0.35, Arizona Mining Inc, whose Hermosa-Taylor discovery South32 bought for CAD $2.1 billion in 2018. Technically, Hermosa-Taylor wasn't a brand new discovery, but rather a rethink of an existing system on whose open-pittable resource $40 million had been spent. It was only when Don Taylor started drilling the deeper sulphide zone that a world class, underground mineable discovery emerged. Arizona Mining's Richard Warke stopped relying on better future metal prices to make Hermosa-Taylor valuable. Instead he used his own money to fund deeper drilling that amounted to a major rethink of the existing system's potential. Like Osisko Mining, Arizona Mining took control of its destiny with spectacular results. At the time this junior's success failed to switch the glass half full for the broader market, but it is now happening.

The graphic above is a monthly time series which presents what percentage of TSX and TSXV resource listings are in each of the price ranges. The most important statistic is the percentage of listings trading below $0.10. Such cheap juniors used to be the anomaly, representing only companies soon to be rolled back (not the case with ASX listings where rollbacks are discouraged and issued shares can exceed 1 billion). The 2008 crash pushed stocks trading below a dime to 53% from which there was a remarkable recovery to less than 15% in Q1 of 2011 when the bear market began. It peaked at 66.1% in late 2015 before a rally lowered the percentage to 33.4% in late 2017, but since then the percentage of juniors below a dime has been rising, peaking at 53.7% in March during the Covid-19 sell-off. The recent sharp decline to just below 40% took place mostly in June and the first week of July. During this short time 203 resource listings have clawed their way above $0.10. This is a widespread awakening and it is not the zombie companies, but rather those juniors which had gone into hibernation during the bear market, juniors with decent management teams and projects that stalled because there was no exploration capital available except on hideous dilution terms. Bottom-fishers are now swarming resource juniors, buying the better ones below a dime and driving them into the $0.10-$0.19 range where the challenge will be to attract financing in order for these juniors to take charge of their value creation destiny.

The situation today is different from 2016 when a similar awakening appeared be ending the 5 year bear market that afflicted the resource juniors longer than any prior bear market during the 1980's and 1990's. There is a new triad at work in this awakening bull market which is entirely about controlling a resource junior's destiny. The focus on rethinking existing systems, with an initial emphasis on gold, is the first leg and it depends on geological creativity coupled with powerful computational manipulation and the collection of relatively low cost new datasets with technologies that allow the junior to see deeper or through cover. Is what we see from historic work all that there is ever to see? Or is all that past work a stepping stone to see the potential for something much bigger and better?

The second leg of this triad comes from investors who are putting up risk capital to enable the junior to make the rethought vision about the bigger and better potential of the existing system a reality by drilling to discover something beyond what is already known about the mineral system. Here is money to make it so, we understand that we may need to give you more, and will do so provided you deliver geological support for your vision. This money is initially coming from high net worth investors and family offices, with institutions, who prefer the math facilitated by feasibility demonstration stories as their excuse for gambling other people's money on resource juniors, a still relatively minor presence. All it takes is cash...wasn't that the song of the cannabis bubble?

The third leg is an entirely new one for the junior resource sector, namely the emergence of the retail investor as an influencer within the various social media platforms. It started in the late nineties with stock forums, first with Silicon Investor, then Stockhouse, and now in Australia, Hot Copper. But now there are platforms like Facebook and Twitter on a big scale and CEO.ca on a smaller scale which allow individuals to develop a following that is based on their postings about any topic, rather than being confined to a specific topic like the Novo stock channel at Stockhouse. Retail investors who are Post-Boomers discovered the stock market through the cannabis bubble, which is now finished. Most of their gambling has been guided by momentum based trend following, which is all that broader markets, given the extreme uncertainty created by the Covid-19 lockdown response for future revenues and earnings, can offer for the foreseeable future. In contrast, the value of a resource junior is defined by metal price, which in the case of gold is in a long term uptrend unless peace and harmony and prosperity miraculously invade the world, deposit parameters like grade and tonnage, and the costs of developing and operating such a deposit as a mine, all of which is captured by the discounted cash flow model that generates a net present value that becomes the basis for assigning a value to a junior tied to its stage in the exploration cycle. In the case of projects undergoing a "rethink", these are all in the S-curve territory associated with the earlier target testing and discovery delineation stages. This is a public space where non-millionaire influencers can shape the narrative. These retail investors, who the regulators have prohibited from helping shape a junior's destiny by giving it money directly through a private placement, will become a powerful force shaping a resource junior's perceived destiny. They will become the engine of a Cambrian Explosion of sorts that reverses the decade long creep of the junior resource sector ecosystem towards an extinction threshold. All this is possible because gold is emerging as the equivalent of the Federal Reserve's guarantee that it will not allow the general stock market to collapse to its intrinsic value. I might say better, because when the Fed's levee breaks gold will this time soar and the resource juniors, in control of their own destinies, need not experience the crash they suffered when Wall Street's house of cards came apart in late 2008.

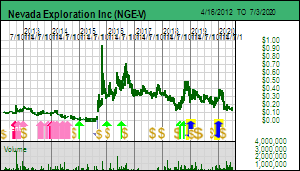

Nevada Exploration Inc released final results on May 27, 2020 for the recent drilling at South Grass Valley which confirmed expectations that a discovery hole was still missing, and on June 1, 2020 announced a farmout deal on the Kelly Creek project which gives the beleaguered junior some breathing room. The latest SGV results confirm what I projected in Tracker May 5, 2020 based on NGE's April update, the upshot of which is that drilling has finally shown that the fluid flow was from the east, ...

Dios Explorations Inc was assigned a Bottom-Fish Spec Value rating on January 23, 2020 in the wake of drill results reported by Azimut Exploration Inc for the Patwon prospect on the adjacent Elmer project in the James Bay region of Quebec. Dios listed on January 31, 2002 after being spun out from Sirios Resources Inc on a 0.08 Dios for 1 Sirios share to hold the diamond assets in central Quebec where Ashton and Rio Tinto had made the Renard diamond discovery in the Otish Mountain area. Headed by...

Zephyr Minerals Ltd announced on June 17, 2020 that an appeal has been filed against its Notice of Intent (NOI) to drill the El Plomo zinc-lead-silver target in Colorado. Zephyr's NOI application was formally accepted on June 5 by the Colorado Division of Reclamation, Mining and Safety (DRMS) which sets the amount of the reclamation bond Zephyr must post, with approval then granted by the Colorado Mined Land Reclamation Board (MLRB). This was supposed to be a quick approval because Zephyr has al...

PJX Resources Inc announced on June 22, 2020 that it has optioned up to 75% of the DD project to MG Capital Corp to continue the Sullivan 2 Hunt in the Panda Basin of southeastern British Columbia. MG Capital completed its qualifying transaction as a capital pool on November 20, 2019 by issuing 32 million shares to acquire privately held DLP Resources Inc, named after David Leo Pighin, who spent much of his career with Cominco (Teck) during which he became one of the top experts on Sullivan and ...

Golden Goliath Resources Ltd moved up sharply in response to an update on June 22, 2020 about the Kwai project in the Red Lake region. The move comes as a surprise because the exploration update requires some geological sophistication to appreciate that the latest work improves the potential for the Pakwash fault that passes through Kwai to host gold mineralization. I assigned a Bottom-Fish Spec Value rating in Tracker January 28, 2020 based largely on the unexplored, blind nature of the Pakwash...

MG Capital Corp was assigned a Bottom-Fish Spec Value rating on June 23, 2020 based on its emergence as the exploration vehicle for Sullivan expert David Pighin which plans to drill 3 separate Sullivan 2 targets in southeastern British Columbia during the summer of 2020. MG Capital was a capital pool which completed its qualifying transaction on November 20, 2019 by issuing 32 million shares to acquire DLP Resources Ltd named after "David Leo Pighin" whose initials also became the new company tr...

Eskay Mining Corp is set to launch an entire rethink of its SIB-Corey land package in the Golden Triangle of British Columbia. The perennially terrible balance sheet has been cleaned up with a $362,122 debt settlement at $0.17 and a $2,440,000 private placement unit financing done at $0.17 and $0.255 for hard and flow-thru dollars. I adopted Eskay Mining as a bottom-fish recommendation in 2017 after SSR Mining Inc optioned The SIB-Lulu portion that SSR optioned required it to spend $14.6 million...