Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.179.50 with the name of '?' since Wed Apr 24, 2024 at 1:15:15 AM PT for approx. 0 minutes now.

100 King Street West #5600, Toronto, ON, M5X 1C9, Canada

Cash Breakup:

$0.00

per sh

Twitter:

Spec Value Rating History

Dec 14, 2018

$0.190

Bottom-Fish Spec Value

New

Dec 21, 2020

$0.140

Bottom-Fish Spec Value

New

Dec 31, 2020

$0.140

Bottom-Fish Spec Value

New

Dec 1, 2021

$0.170

Bottom-Fish Spec Value

New

Dec 31, 2021

$0.180

Bottom-Fish Spec Value

New

Oct 16, 2023

$0.090

Bottom-Fish Spec Value

New

Apr 19, 2024

$0.280

Fair Spec Value

New

Spec Value Rating Overview Updated October 17, 2023

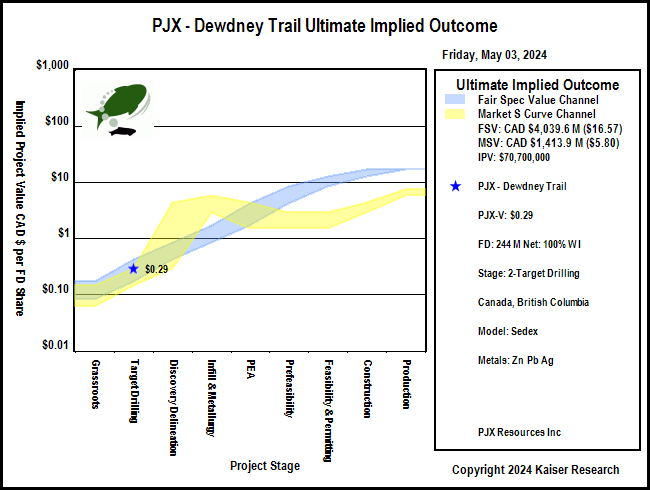

SV Rating: Fair Spec Value - as of April 19, 2024: PJX Resources Inc has been confirmed effective October 16, 2023 with a Bottom-Fish Spec Value rating at $0.09 based on emerging evidence that a Sullivan style zinc-lead-silver exhalative horizon with size potential is present on the 100% owned Dewdney Trail project in southeastern British Columbia. So far PJX has only found mineralized boulders within a talus field on the slope of a mountain, but the exhalative nature of the boulders is very different from the nearby Estella vein deposit, and the physical setting is such that a massive sulphide horizon must outcrop somewhere up the mountain slope underneath the talus debris which consists mostly of younger barren sediments from higher up the mountain. The PJX prospecting crew is racing against winter to establish upslope cutoff for the zinc-lead-silver boulders and possibly find mineralized bedrock. But that may not be necessary. A 2021 geophysical survey has already indicated that this area is underlain by a magnetic high potentially caused by pyrrhotite, the magnetic iron sulphide associated with the Sullivan deposit. This data is being reprocessed by another group to achieve more granularity to allow spotting a drill program even if the exact bedrock source remains hidden under talus. The size of this magnetic anomaly offers substantially greater scale potential than the Kootenay King "puddle" 5 km to the south if it is part of a zinc-lead-silver rich Sullivan style system. Sullivan itself has only a modest surface exposure and its 160 million tonnes were mostly underground mined. PJX has initiated permitting for a drill program in May 2024 when the mountain side will be reasonably clear of snow and ice. It only has to consult with one First Nations group in this area, and this is a group with a history of cooperation with the resource sector, so there is a lower reconciliation risk than usual though given the current Canadian government's hostility towards resource extraction one must keep the NoCanDo risk in mind. The drilling delay until May 2024 gives PJX time to boost its $500,000 working capital with a new financing and also time for bottom-fishers to accumulate positions during bear market conditions. About 28% of the 133.2 million issued are held by insiders, of which management is 3% while the rest are a couple of long time timber baron supporters. In addition Osisko Gold Royalties which acquired a 0.5% NSR on all the properties in 2021 may still own its 6,250,000 shares which are now below the reporting threshold and may remain supportive of PJX. There is an overhang of 29,118,182 warrants between $0.20-$0.30 of which all but 9,350,400 expire in December 2023 unless extended again which boosts fully diluted to 171.8 million shares. PJX does not face any immediate rollback risk, and the two other main property groups are strong enough for the junior to participate in a resource junior bull cycle even if Dewdney Trail fails to materialize into a major Sullivan Two discovery. At 171.8 million FD and $0.09 the market is implying a value of only CAD $15 million for a Sullivan Two outcome at Dewdney Trail.

Recommendation History

Edition

Date

Price

Recommendation

Gain

SVF2019

12/31/2018

$0.22

Bottom-Fish Spec Value Favorite

0%

SVF2019

12/31/2019

$0.16

Bottom-Fish Spec Value Favorite

-26%

SVF2020

12/31/2019

$0.16

Bottom-Fish Spec Value Favorite

0%

SVF2020

12/31/2020

$0.14

Bottom-Fish Spec Value Favorite

-13%

SVF2021

12/31/2020

$0.14

Bottom-Fish Spec Value Favorite

0%

SVF2021

12/31/2021

$0.17

SV Technical Closeout 100%

18%

SVF2024

4/19/2024

$0.28

Fair Spec Value Favorite

0%

Charts & Financing Activity

Most recent 43-101 resource estimate Prior resource estimate PEA PFS FS/BFS/DFS

Private Placement Key

less than $500,000

$1,000,000 - $2,000,000

$5,000,000 - $10,000,000

$20,000,000 - $50,000,000

$500,000 - $1,000,000

$2,000,000 - $5,000,000

$10,000,000 - $20,000,000

over $50,000,000

Private placement financing dates and value ranges are based on transactions reported by the TSXV Monthly Review.

Past Insiders and Reported Shareholders - Current Ownership Status unknown - positions may be pre-rollback

Related Party

Occupation

Related Since

Insider Ended

Director Ended

Capacity

Ownership

Susan McDonald

6/29/2011

Insider

2,018,250

Osisko Gold Royalties Ltd

Public Company

2/9/2021

6/20/2023

Insider

6,250,000

Somerset Parker

Deceased

3/7/2011

7/26/2018

7/26/2018

Director

0

Kent Pearson

Geologist

3/7/2011

6/20/2023

6/20/2023

Director

49,000

Share positions of current insiders based on last AGM circular, ownership % based on current Issued. Share positions of past insiders and shareholders have not been adjusted for rollbacks or splits.

A Spec Value Hunter table allows speculators to identify which projects offer poor, fair or good speculative value according to the rational speculation model. The speculative value depends on the project stage, the project's implied value as calculated by the company's fully diluted, stock price and net project interest, and the dream target deemed appropriate for the project. A dream target is what a project would be worth in discounted cash flow terms once in production.

Poor Speculative Value -

Fair Speculative Value -

Good Speculative Value -

Note: narrow arrows indicate IPV is outside the fair value channel but within 25% of the fair value limits

Color Key for Target Outcome Achievability Ranges in millions ranked from most to least achievable

below $25

Should be Private: Artisanal, Placer, Mom & Pop Shop

$25-$50

Tiny Scale: underground mine or quarry - not worth the bother

$50-$100

Small Scale: junior needs to self-develop

$100-$250

Buyout Target: by Lower Tier Producers

$250-$500

Buyout Target: by Mid-Tier Producers

$500-$1,000

Ideal Target for Junior: Buckhorn, Sleeper

$1,000-$2,000

Almost World Class: Ekati, Red Chris, Brucejack, Juanicipio, Stibnite

$2,000-$5,000

World Class: Eskay Creek, Hemlo, Hermosa-Taylor, Oyu Tolgoi, LaRonde, McArthur

$5,000-$10,000

Giants: Escondida, Sullivan, Carlin Trend, Kidd Creek, Orapa, Kamoa-Kakula

above $10,000

Off the Scale District: Wits 1.0, Araxa, Sudbury Basin, Bayan Obo

The target outcome range required for the current implied project value to represent fair speculative value is based on the upper and lower certainty limits associated with the project stage. The color coding is based on the target outcome using the mid-point of the certainty range.

Active Company Projects

Project

Location

Net Interest

Stage

IPV $ MM

Fair Spec Value Required Target Outcome Range

$100

UPV $500

$2000

Target Metals

Deposit Style

Dewdney Trail

Canada - British Columbia - Southeast BC

100% WI

2-Target Drilling

$76

$3,023 - $7,557

Zinc Lead Silver

Sedex

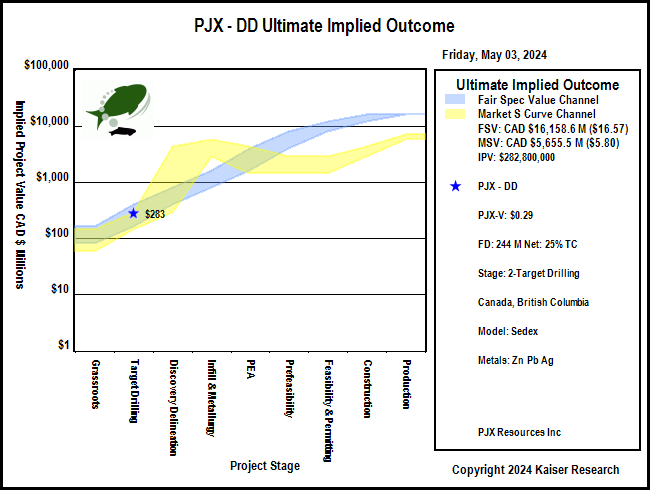

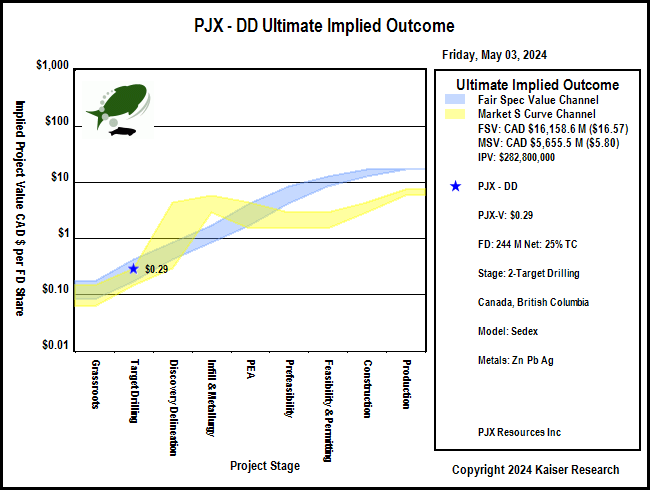

DD

Canada - British Columbia

25% TC

2-Target Drilling

$302

$12,091 - $30,228

Zinc Lead Silver

Sedex

Eddy - Gold Shear

Canada - British Columbia - Southeast BC

100% WI

2-Target Drilling

$76

$3,023 - $7,557

Gold

Orogenic Vein

Vine

Canada - British Columbia - Southeast BC

100% WI

2-Target Drilling

$76

$3,023 - $7,557

Zinc Lead Silver

Sedex

Parker Copper

Canada - British Columbia - Southeast BC

100% WI

1-Grassroots

$76

$7,557 - $15,114

Copper

Sediment Hosted

West Basin

Canada - British Columbia - Southeast BC

100% WI

1-Grassroots

$76

$7,557 - $15,114

Zinc Lead Silver

Sedex

Zinger

Canada - British Columbia - Southeast BC

100% WI

2-Target Drilling

$76

$3,023 - $7,557

Gold

Orogenic Vein

Project Stage

Flagship

Secondary

Active

Grassroots (1) & Target Testing (2)

Discovery Delineation (3)

Infill Drilling & Metallurgy (4)

PEA (5) or PFS (6)

Feasibility & Permitting (7)

Construction (8) or Production (9)

Clicking on the project icon will display a popup identifying the company project, its stage and target metals, basic facts, a chart, a link to that project within that company's KRO Profile, a link to the most recent news release, and a link to the most recent KRO comment if one exists.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 0.50%

Ownership Terms: PJX Resources has an option to earn up to an 80-per-cent interest from SG Spirit Gold Inc. In July 2013 the terms were revised so that PJX can earn up to 100%. The initial option agreement with SG, dated Sept. 14, 2010, allowed PJX to earn up to an 80-per-cent interest in the properties by spending $2.5-million in exploration work and paying $215,000 in cash payments over four years. Under the agreement, PJX will have full ownership with no net smelter return royalties or other retained interest by SG, and PJX will not have to complete approximately $750,000 in remaining work commitments. The agreement requires PJX to make the remaining cash payments of $125,000 that would have had to be made under the option agreement and issue 500,000 PJX shares to SG that were not in the option agreement. On Feb 9, 2021 PJX sold a 0.5% NSR on the Gold Shear, Eddy, Zinger and Dewdney Trail claim blocks to Osisko Gold Royalties Ltd for $1 million. On July 29, 2021 PJX optioned the 14 Estella crown grants from Imperial Metals for $250,000 over 5 years. Imperial retains a 2% NSR of which can be bought for $2 million.

Net Interest: 25% TC Vested: Yes Uncapped NSR/GOR: 0.00%

Ownership Terms: Option dated July 2015 to acquire 100% from Doug Anderson and David Pighin for 250,000 shares over 5 years, subject to 2% NSR which can be bought for $2 million. Teck optioned 75% on May 16, 2016 whereby it can earn 51% by spending $4 million by Jan 31, 2021, and 75% by spending an additional $4 million by Jan 31, 2024.Teck dropped option in late 2019. Agreement June 22, 2020 where MG Capital Corp can earn up to 75% by paying $250,000 and spending $4 million over 4 years to earn 50%, at which pioint it can elect to earn 75% by delivering a bankable feasibility study within 8 years of the agreement. On Aug 20, 2020 DLP optioned 100% of the NZOU (NaZoo) property for $115,000 and 400,000 shares in stages by Dec 31, 2025. 453999 BC Ltd retains 2% NSR of which 1% can be bought for $1 million. Moby Dick appears to have been acquired by staking. The area of interest clause for DD includes Moby Dick and NZOU though PJX must contribute 50% of the acquisition costs. The 75% stepup applies to all 3 claim blocks which would carry PJX through a BFS.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 0.50%

Ownership Terms: Initially part of a package optioned 80% from SG Spirit Gold Inc in 2010 which PJX acquired 100% in Oct 2013 after spending $1,750,000 of its $2.5 million obligation in exchange for $125,000 and 500,000 shares. On Jan 17, 2018 PJX optioned 100% of the Gold Shear property from Louis Davis for $45,000 and 200,000 shares over 2 years. The vendor retains a 2% NSR of which can be bought for $2 million. On Feb 9, 2021 PJX sold a 0.5% NSR on the Gold Shear, Eddy, Zinger and Dewdney Trail claim blocks to Osisko Gold Royalties Ltd for $1 million.

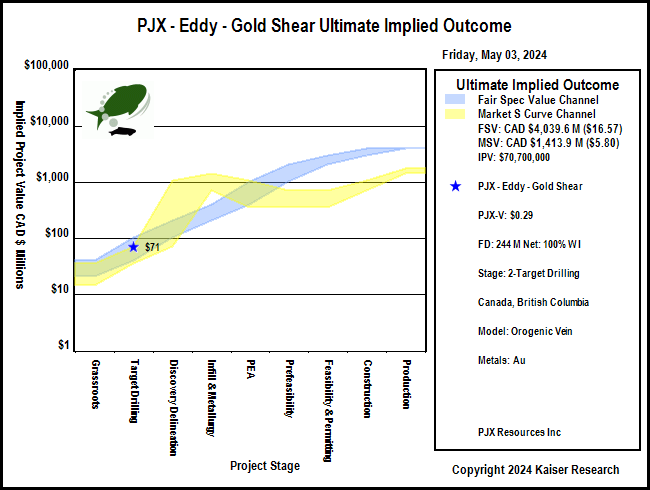

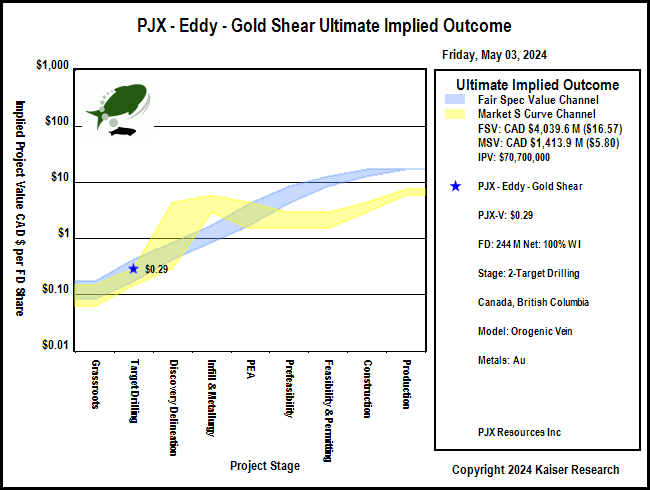

Target Metals: Gold

Model: Orogenic Vein

Stage: 2-Target Drilling

Notes on Eddy - Gold Shear Project

Prospecting and geological mapping by SG Spirit Gold Inc identified a succession of gold-mineralized quartz veins which occur along shear zones within the fold hinge of a regional anticline that is at least 9.5 km long on the property. A total of 64 grab samples of bedrock have returned values ranging from 1 to 57 g/t Au and demonstrate the potential for high-grade gold concentrations along the shear zones.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 0.00%

Ownership Terms: Initially part of a package optioned 80% from SG Spirit Gold Inc in 2010 which PJX acquired 100% in Oct 2013 after spending $1,750,000 of its $2.5 million obligation in exchange for $125,000 and 500,000 shares. In Feb 2014 PJX acquired the Vine Extension claims from Klondike Gold Corp for 700,000 shares. The property was subject to a 50% farm-in by PJX on Apr 26, 2012. Klondike Gold retains a 1% NSR on the Vine Extension claims.

Net Interest: 100% WI Vested: Yes Uncapped NSR/GOR: 0.50%

Ownership Terms: Initially part of a package optioned 80% from SG Spirit Gold Inc in 2010 which PJX acquired 100% in Oct 2013 after spending $1,750,000 of its $2.5 million obligation in exchange for $125,000 and 500,000 shares. On Feb 9, 2021 PJX sold a 0.5% NSR on the Gold Shear, Eddy, Zinger and Dewdney Trail claim blocks to Osisko Gold Royalties Ltd for $1 million.