Hello Guest User, You are visiting this website from a computer with an IP address of 172.70.131.199 with the name of '?' since Tue Apr 23, 2024 at 8:06:59 AM PT for approx. 0 minutes now.

Albert Matter, the CEO of NuLegacy Gold Corp, is a colorful character who is working very hard to turn NuLegacy into an exploration success after the first $20 million failed to deliver much more than a gold geochemical anomaly at Red Hill just southeast of Barrick's Goldrush deposit which probably needs $2,000 plus gold to be worth developing as a modest oxide open pit heap leach operation. But he persisted. Instead of rolling back the stock brutally and starting over like the vampire squids of this industry insisted, he brought on board a new team of former Barrick people to rethink the Red Hill project, out of which emerged the Rift Anticline hypothesis for a potential Goldrush Two clone. Now he is trying to get a plan of operations approved by September so that he can launch a major drill program to see if he indeed does have another 10 million plus oz high grade Carlin type deposit or even better under those barren younger cover rocks just to the west of where he spent all the money. He raised $7.5 million through 100 million units at $0.075 last October and now he is going after another $5 million through 75 million units at $0.075 to make sure that he can keep drilling when flu season resumes in Q4 of 2020 and the main market tanks while gold soars. As the photo above of Albert and the Big Stick shows, he is determined not to miss out on what could be an awful lot of fun once the plan of operations is approved. I've had NuLegacy as a Bottom-Fish spec value rated junior during most of Albert's Red Hill adventure, and finally feel that he has very good story. I wrote up the Rift Anticline story in Tracker February 26, 2020 which I've made unrestricted to the public because KRO members had plenty of time to buy the stock when it tanked into the $0.03-$0.05 range during the March Covid-19 meltdown. What I have now created for KRO members is an Outcome Visualization for Red Hill as a Goldrush Two clone which allows us to see what the valuation impact should be in the context of my "rational speculation model" if drilling starts to deliver results supportive of a Goldrush scale and calibre discovery. The rational speculation model is very conservative, but it also provides the analytical framework for understanding market S-Curve action when a project moves from target testing to discovery delineation. This OV updates every night based on stock price, gold price, CAD:USD exchange rate, fully diluted (I'm assuming Albert gets the latest PP done), and any changes I may make about the underlying assumptions. I believe I have created a new paradigm for how resource junior speculators should think about discovery or optionality plays, though "create" is a stretch because this is what all the majors do behind the scenes and what any competent junior management team which grasps "economic geology" also does behind the scenes. They just can't talk to the public about it until they have published a 43-101 resource estimate followed by an economic study at PEA or higher standard. This knowledge gap between market and management is the big missing piece. To help general audiences understand this concept, in particular Post Boomers who have never dabbled in resource juniors, I have made available the NuLegacy OV below "frozen" as it was on May 21, 2020. For those of you who want to access member only stuff and track OV's I have done for juniors like NioBay Metals, Eagle Plains, Zephyr Minerals and Eskay Mining, we are now accepting new individual KRO memberships as well as renewals for lapsed members through Subscriptions.

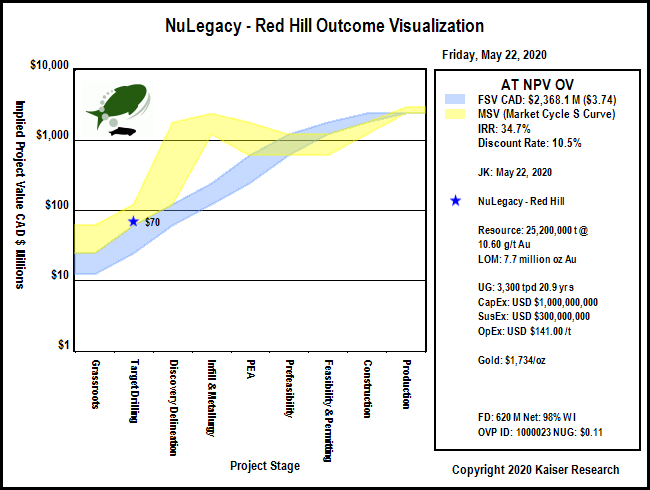

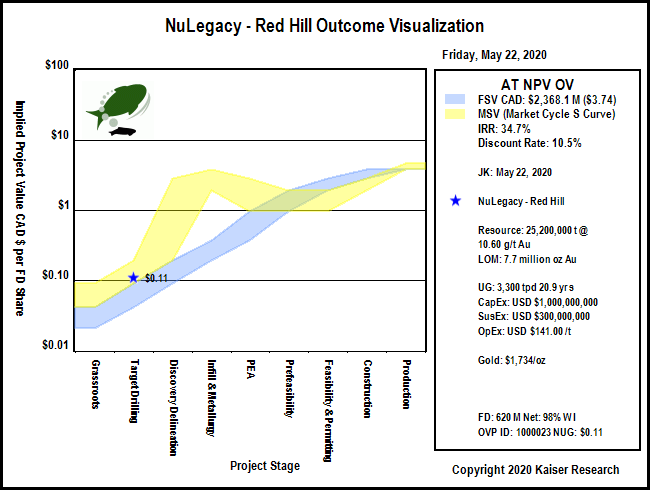

Outcome Visualization Project as of May 21, 2020: NuLegacy: Red Hill - 3,300 tpd UG Goldrush Two

Key People: Albert J. Matter (CEO), Danny Lee (CFO)

Diluted 620,408,769

Insiders 17.2%

As of 12/31/2019

Visualized Outcome: NuLegacy: Red Hill - 3,300 tpd UG Goldrush Two

NuLegacy spent over $20 million from 2012 onwards trying to find high grade Carlin type zones in addition to the low grade oxide Iceberg zone. In late 2017 NUG brought former Barrick exploration people including Ed Cope, Mark Bradley and Charles Weakly on board in an effort to salvage the play. Their work developed the Rift Anticline hypothesis to the west of all the drilling activity, an area covered by younger basalts which has never been drilled because it was assumed the Lower Plate rocks prospective for Carlin type mineralization. The ex Barrick team which worked on Goldrush relogged all the core to the west and developed a stratigraphic model they were able to map CSAMT geophysical data. A CSAMT survey over the barren rocks to the west developed a structural model very similar in scale and nature to the Goldrush deposit to the northwest that Barrick is developing as an underground mine expected to produce 450,000 oz per year at an AISC of $665 per oz. Barrick completed a PFS for Goldrush but has never disclosed cost details. However, from the technical reports it has filed for the Cortz JV operation which includes UG mining refractory sulphides similar to those that define the Goldrush deposit (25.2 million tonnes of 10.6 g/y gold), which are trucked to the Goldstrike roaster for processing, it is possible to come up with likely costs. This OV imagines a clone of Goldrush One, what it would cost to develop and operate, and what it would be worth at the current gold price.

Visualized Outcome Summary: NuLegacy: Red Hill - 3,300 tpd UG Goldrush Two

Economic Outcome (USD): Revenue Model at OV designated Metal Prices

Annual Average

Life of Mine (LOM)

LOM Stats

Recoverable Revenue:

$647,567,314

$13,548,108,191

$538/t ore Recoverable Value:

Smelter/Transport Costs:

($6,475,673)

($135,481,082)

1.0% of Recoverable Revenue

Gross Payable Revenue:

$641,091,641

$13,412,627,109

99.0% of Recoverable Revenue

Royalties:

($19,232,749)

($402,378,813)

3.0% of Gross Payable Revenue

Net Payable Revenue:

$621,858,892

$13,010,248,296

96.0% of Recoverable Revenue

Mining Cost:

($104,791,500)

($2,192,400,000)

57% of OpEx - $87.00/t ore

Processing Cost:

($57,816,000)

($1,209,600,000)

31% of OpEx - $48.00/t ore

Other Cost:

($7,227,000)

($151,200,000)

4% of OpEx - $6.00/t ore

Sustaining Cost:

($14,285,714)

($300,000,000)

8% of OpEx - $11.90/t ore

Total Operating Cost:

($184,120,214)

($3,853,200,000)

30% of Net Payable Revenue - OpEx - $152.90/t ore

Pre-Tax Cash Flow:

$437,738,677

$9,157,048,296

70% of Net Payable Revenue - $363.37/t ore

Taxes:

($96,740,800)

($2,035,183,550)

22% of Pre-Tax Cash Flow - $80.76/t ore

After-Tax Cash Flow:

$340,997,877

$7,121,864,746

55% of Net Payable Revenue - $282.61/t ore

Note: Concentrate transport costs, smelter treatment costs and retention are subtracted from recoverable revenue to get gross payable revenue to which the uncapped royalty rate for the project is applied. The annual average of LOM sustaining cost is expensed as an annual operating cost. Annual average figures reflect full production years.

Economic Outcome (USD): Royalty Model for 1% NSR at OV designated Metal Prices

Mine Life:

21 years

Startup

NPV 5%

NPV 10%

NPV 15%

Annual Avg NSR:

$6,218,589

Now

$75,766,053

$48,833,406

$34,111,900

LOM NSR:

$130,102,483

2028

$51,281,447

$22,781,144

$11,151,241

Economic Outcome - Discount Rate: 10.5% - CAD AT NPV: $2.4 billion - Poor Speculative Value

Gross Rock Value (USD/t):

$591

Recoverable Rock Value:

$538

Payable Rock Value:

$532

LOM Net Payable Revenue (USD):

$13,010,248,296

LOM PT Cash Flow (USD):

$9,157,048,296

LOM AT Cash Flow (USD):

$7,121,864,746

USD Pre-Tax NPV:

$2,400,369,746

Pre-Tax IRR:

43.8%

Pre-Tax Payback:

2.3

USD After-Tax NPV:

$1,689,718,300

After-Tax IRR:

34.7%

After-Tax Payback:

2.9

CAD Fair Spec Value Low:

$23,681,402

CAD Fair Spec Value High:

$59,203,505

CAD Implied Project Value:

$69,637,719

Price Target if Visualized Outcome delivered by Expl-Dev Cycle without dilution: CAD $3.74

Fair Speculative Value Stock Price Range: CAD $0.04 - $0.09

MSV (Market Cycle S Curve): Market Speculative Value represents the typical market pricing pattern of a new discovery as it moves through its exploration-development cycle. The irrational pricing behavior of the yellow channel contrasts with the fair speculative value of the blue channel as defined by the rational speculation model because during the pre-economic study stages there is great uncertainty about how big the discovery will turn out.

Fair Speculative Value Ladder

USD OV NPV

CAD OV NPV

Exch Rate

Diluted

Net Interest

$1,689,718,300

$2,368,140,197

1.4015

620,408,769

98.00%

Project Stage

Uncertainty Range

CAD FSV Range

CAD FSV per Share Range

CAD MSV per Share Range

Grassroots

0.5% - 1.0%

$11,840,701 - $23,681,402

$0.02 - $0.04

$0.04 - $0.09

Target Drilling

1.0% - 2.5%

$23,681,402 - $59,203,505

$0.04 - $0.09

$0.09 - $0.19

Discovery Delineation

2.5% - 5.0%

$59,203,505 - $118,407,010

$0.09 - $0.19

$0.19 - $2.81

Infill & Metallurgy

5% - 10%

$118,407,010 - $236,814,020

$0.19 - $0.37

$1.87 - $3.74

PEA

10% - 25%

$236,814,020 - $592,035,049

$0.37 - $0.94

$0.94 - $2.81

Prefeasibility

25% - 50%

$592,035,049 - $1,184,070,099

$0.94 - $1.87

$0.94 - $1.87

Permitting & Feasibility

50% - 75%

$1,184,070,099 - $1,776,105,148

$1.87 - $2.81

$0.94 - $1.87

Construction

75% - 100%

$1,776,105,148 - $2,368,140,197

$2.81 - $3.74

$1.87 - $2.81

Production

100%

$2,368,140,197

$3.74

$3.74 - $4.68

Market Speculative Value Stock Price Range: CAD $0.09 - $0.19

Warning: while the market spec value (S-Curve) and fair spec value channels presented in project value terms track the evolving expected ultimate outcome value, when presented in stock price terms the expected stock prices are subject to dilution through future equity financings or project interest farmouts.

Alternative Metal Price Scenarios

Metal 1

Metal 2

Metal 3

Metal 4

Gold

Spot:

$1,734 /oz

OV Assigned:

$1,734 /oz

Pessimistic:

$1,000 /oz

Optimistic:

$1,600 /oz

Fantasy:

$2,500 /oz

Note: for Metal 1 pessimistic, optimistic and fantasy price scenarios, OV assigned prices are used for Metals 2-4

Economic Outcomes with Alternative Metal Price Scenarios

USD PT NPV

USD PT IRR

USD AT NPV

USD AT IRR

AT Payback yrs

Spot:

$2,400,369,746

43.8%

$1,689,718,300

34.7%

2.9

OV Assigned:

$2,400,369,746

43.8%

$1,689,718,300

34.7%

2.9

Pessimistic:

$413,342,950

16.8%

$198,454,690

13.7%

6.7

Optimistic:

$2,038,611,954

38.9%

$1,418,219,077

31.0%

3.2

Fantasy:

$4,476,515,459

71.3%

$3,247,865,657

55.5%

1.8

Fair Speculative Value for Alternative Metal Price Scenarios

Stage: Target Drilling - 1.0% - 2.5%

CAD AT NPV

CAD Target Price

CAD FSV Range

CAD FSV per Share Range

CAD MSV per Share Range

Spot:

$2,368,140,197

$3.74

$23,681,402 - $59,203,505

$0.04 - $0.09

$0.09 - $0.19

OV Assigned:

$2,368,140,197

$3.74

$23,681,402 - $59,203,505

$0.04 - $0.09

$0.09 - $0.19

Pessimistic:

$278,134,248

$0.44

$2,781,342 - $6,953,356

$0.00 - $0.01

$0.01 - $0.02

Optimistic:

$1,987,634,036

$3.14

$19,876,340 - $49,690,851

$0.03 - $0.08

$0.08 - $0.16

Fantasy:

$4,551,883,719

$7.19

$45,518,837 - $113,797,093

$0.07 - $0.18

$0.18 - $0.36

Detailed Visualized Outcome (KRO Members Only)

VU = Very Unsure

SU = Somewhat Unsure

SS = Somewhat Sure

VS = Very Sure

The confidence indicator is intended to convey the visualizer's degree of uncertainty with regard to a particular assumption.

Deposit Scenario

Metal 1

Metal 2

Metal 3

Metal 4

Gold Au

Grade:

10.6 g/t

VS

Recovery:

91.0%

SS

Payable:

99.0%

VS

Concentrate Grade:

0.0%

VS

Price:

$1,733.55 /oz

VS

Price Type:

Spot

Annual Payable:

369,814 oz

LOM Payable:

7,737,087 oz

Metal 1 Note: Gold ore is refractory and needs to be roasted. The recovery is what Barrick achieved for underground refractory sulphide ore mined at Cortez and trucked to the Goldstrike roaster. The recovery is what Barrick gets for roasted ore mined UG at Cortez.

Mining Scenario

Tonnage:

25,200,000

VS

Strip Rate:

0.0

VS

Operating Rate (tpd):

3,300

SS

Mining Type:

Underground

VS

Mine Life (years):

20.9

Startup:

2028

VU

Tax Treatment:

DDBM - double declining balance

SS

Tax Rate:

25.0%

SS

Tonnage Note: The resource is that published by Barrick for its Goldrush deposit: 25,200,000 tonnes at 10.6 g/t gold which is the final stages a feasibility study and permitting cycle with completion expected in 2020, though this is somewhat uncertain given the Covid-19 situaton. It is important to understand that the Rift Anticline target of NuLegacy is completely blind and a conceptual extrapolation of peripheral exploration data mapped to CSAMT geophysical data for the Rift Anticline area.

Operating Rate Note: Based on Barrick's UG mining rate of Cortez Hills breccia.

Mining Type Note: Barrick decided against open-pit mining to reduce the permitting cycle.

Tax Treatment Note: This depreciation method boosts after tax cash flow during the early years.

Tax Rate Note: The federal corporate tax rate is 21%. Nevada has no state corporate tax but does have a 5% minerals tax on net profits. Since a minerals tax is deductible before application of the federal tax rate, the effective tax rate is 24.95%: ((1-0.05) x 0.21) + .05

Cost Scenario

Currency

USD Cost

Exchange Rate

CapEx:

$1,000,000,000

SS

USD

$1,000,000,000

1.000

Sustaining Capital:

$300,000,000

SU

USD

$300,000,000

1.000

Mining Cost ($/t rock):

$87.00

SS

USD

$87.00

1.000

Mining Cost ($/t ore):

$87.00

USD

$87.00

1.000

Processing Cost ($/t):

$48.00

SS

USD

$48.00

1.000

Other Cost ($/t):

$6.00

SS

USD

$6.00

1.000

Total OpEx ($/t):

$141.00

USD

$141.00

1.000

CapEx Note: Barrick in a press release stated that CapEx would be $1 billion.

Sustaining Capital Note: The sustaining cost for the Cortez UG roaster ore is $11.10/ST or $12.23/MT which works out to $308 million for the deposit resource and has been rounded down to $300 million.

Processing Cost Note: Processing cost for roasted sulphides is $29.01/ST converted to $31.97/MT plus $14.42/ST transportation to Goldstrike converted to $15.89/MT for a total of $47.86/MT rounded up to $48/t.

Other Cost Note: G&A is $5.02/ST for roasted ore converted to $5.53/MT rounded up to $6/t.

Risk Factors - Risk-Adjusted Discount Rate: 10.5%

Risk Level

Risk Weight

Confidence

Note

Environmental Permitting:

Low

1.0

SU

Established nearby Pipeline-Cortez mining complex and Goldrush UG mine at permitting stage.

Social License:

Very Low

0.5

VS

Uninhabited area with no grazing, close to Pipeline-Cortez mining operations.

Title:

Low

1.0

SS

Tax:

High

1.5

SU

Nevada tax has no state corporate tax nor any royalty, just a 5% minerals tax. This is about as good as it gets, so it can only get worse depending on the federal government and the economic hardship Nevada ends up facing.

GeoPolitical:

Very Low

1.0

VS

Half of America thinks Donald Trump is the best president ever. What could go wrong?

Infrastructure:

Very Low

0.5

SS

Next door to existing world class mining infrastructure.

Technical:

Low

2.5

SS

Assumes mineralization will be refractory and that ore will bee trucked to Goldstrike roaster.

Management:

Low

1.5

SS

Management includes top-notch former high level Barrick people work worked on nearby Pipeline-Cortez-Goldrush system.

Financing:

Low

1.0

SS

Although NuLegacy already has 403 million shares issued, CEO Albert Matter has a fund-raising track record, and has already raised over $20 million for Red Hill. Plus he now carries a Big Stick.

Risk Factor Weight Table

Very Low

Low

High

Very High

Environmental Permitting:

0.5

1.0

1.5

2.0

Social License:

0.5

1.0

1.5

2.0

Title:

0.5

1.0

1.5

2.0

Tax:

0.5

1.0

1.5

2.0

GeoPolitical:

0.5

1.0

1.5

2.0

Infrastructure:

0.5

1.5

2.5

4.0

Technical:

1.0

2.5

4.0

5.5

Management:

0.5

1.5

3.0

4.0

Financing:

0.5

1.0

1.5

2.0

The risk adjusted discount rate is the sum of the weight of the risk level assigned to each risk factor.

Disclaimer: A visualized outcome is one of many possible outcomes for an exploration project as it moves through the 9 stages of the exploration-development cycle from grassroots to a producing mine with failure as an outcome at any point along the way. The range of possible outcomes for the physical nature of a deposit shrinks after delivery of an initial 43-101 resource estimate. While the nature of the deposit constrains the range of mining scenarios, the cost assumptions will vary as the project moves through the feasibility demonstration stages of the cycle, which affects the economic value of the final outcome. This economic value will also vary according to the prices of the metals targeted for extraction which may change during the years it takes for a project to become a mine. An outcome visualization is thus a compilation of best guess assumptions for the key variables that drive the discounted cash flow model, the basis for assigning an economic value to a mine. An OV is not intended as a prediction, but rather as a framework that allows the incorporation of new information generated by the exploration-development cycle for the project into a valuation model on an ongoing, dynamic basis.